Kolawole Bekes is a Database Administrator, Database Reliability Engineer, and DevOps Engineer with over a decade of experience spanning multiple industries. He holds a Bachelor’s degree in Mathematics from the University of Abuja. Following his relocation to the United States in 2015 and subsequently to Canada in 2017, he has built a career working with organisations such as Microsoft, AppDirect, WorkJam, Sunwing Airlines, Agio, and Big Fish Games.Â

He is also

Kolawole Bekes is a Database Administrator, Database Reliability Engineer, and DevOps Engineer with over a decade of experience spanning multiple industries. He holds a Bachelor’s degree in Mathematics from the University of Abuja. Following his relocation to the United States in 2015 and subsequently to Canada in 2017, he has built a career working with organisations such as Microsoft, AppDirect, WorkJam, Sunwing Airlines, Agio, and Big Fish Games.Â

He is also the founder and chief executive officer of WakaMi, an on-demand errand service platform focused on delivering reliable and efficient errand solutions to Nigerians both locally and in the diaspora.

Explain what you do to a 5-year-old.

Once upon a time, there was a big fruit garden where fruits kept falling everywhere—apples here, bananas there, and oranges rolling all over the ground. Nobody could find what they wanted.

So I became the helper of the garden. I picked up all the fruits and put them into the right baskets; apples in one basket, bananas in another, and oranges in their own place.

I also made sure the fruits stayed fresh and safe. Whenever someone came looking for a fruit, I could quickly say, “I know exactly where it is,†and give it to them right away.

My job is to keep everything neat, safe, and easy to find, just like the fruit baskets in the garden.

How did you become a Database Administrator?

I became a Database Administrator as part of a deliberate effort to improve my earning potential and build a more reliable career path. I joined a community of IT professionals in North America, where I was exposed to new ideas and opportunities.Â

Through that network, I discovered and enrolled in a bootcamp, completed several training sessions, and gained hands-on experience. I then applied to multiple roles, and eventually secured an opportunity that marked the beginning of my career as a Database Administrator.

What is the easiest and most difficult part about your job?

The easiest part of my job is when systems are well-structured and everything is running smoothly. Tasks like monitoring, backups, and routine maintenance become very straightforward.

The most difficult part is handling unexpected issues, like performance bottlenecks or outages, especially under time pressure. But that’s also the most rewarding part, because it challenges me to think critically, troubleshoot quickly, and ensure systems are restored with minimal impact.

If your job had a warning label, what would it say?

Warning: Unexpected issues may occur at any time. Requires patience, quick thinking, and a strong relationship with coffee.

What’s one real-world incident where your database decisions directly saved (or cost) a company big time?

Early in my career, I was involved in a deployment where a change was made directly in production without a proper rollback plan. Unfortunately, it caused a temporary disruption to a critical service.

Although we resolved it quickly, it highlighted the importance of change management. From that point on, I enforced stricter deployment processes introducing staging validation, rollback strategies, and better communication.

It significantly reduced risk for us in future deployments, critical because it now shapes how I approach database changes today.

As a first-time founder living abroad, what is the hardest part about building a startup for a market where you’re not physically present? How do you deal with this?

One of the hardest parts of building a startup remotely while living in Canada and operating in Nigeria is maintaining strong team alignment and accountability when you are not physically present day to day.

Early on, I experienced challenges with staff management, particularly around consistency, ownership, and productivity. Some team members struggled with structure, and it became clear that the issue was not just about effort. It was about clarity, expectations, and systems.

To address this, I shifted my approach in a few ways. First, I implemented clear performance metrics and deliverables so everyone understands exactly what success looks like. Second, I introduced regular check-ins and reporting structures to improve visibility. Third, I focused more on hiring for accountability and cultural fit, not just technical skills.

I also make it a point to spend time in Nigeria periodically, which helps reinforce relationships, build trust, and reset expectations with the team.

Overall, the experience taught me that managing a remote team, especially across different environments, requires intentional structure, strong communication, and the right people in place. Once those are aligned, performance improves significantly.

What’s the vision behind WakaMi and why do you think a marketplace for managed services can scale in Nigeria?

The vision behind WakaMi came from a personal experience. While living in Canada, I needed someone to handle an errand for me in Nigeria. I tried finding help online, but unfortunately, I had a bad experience where I lost money.

That led me to dig deeper, and I realised this was not just my problem. Many people, especially those in the diaspora, face the same challenge. There is no reliable, structured way to get trusted services done remotely in Nigeria.

WakaMi was built to solve that. It is an on-demand managed services marketplace that connects people who need errands or services done with verified service providers. It also provides oversight by tracking progress and only releasing payment once the task is completed and confirmed.

I believe it can scale in Nigeria because it addresses a real and growing problem. As more Nigerians live and work abroad, and as urban life becomes busier locally, the demand for trusted on-demand services will continue to increase.

What makes it scalable is the combination of trust, structure, and technology, bringing accountability into an otherwise informal market. Once you solve trust at scale in a service marketplace, growth becomes a natural outcome.

Put a finger down if you experienced poor service with Nigerian telecom operators between November 2025 and January 2026.

The Nigerian Communications Commission (NCC), the country’s telecoms regulator, has said that subscribers will receive airtime refunds as compensation for poor service experienced within the said time.

In other news, Nigeria’s elections have a retention problem. A new Zikoko Citizen report predicts what participation in the 2027 election might look like, drawing on trends from previous cycles, and explores what could bring about a massive turnaround.

Kolawole Bekes is a Database Administrator, Database Reliability Engineer, and DevOps Engineer with over a decade of experience spanning multiple industries. He holds a Bachelor’s degree in Mathematics from the University of Abuja. Following his relocation to the United States in 2015 and subsequently to Canada in 2017, he has built a career working with organisations such as Microsoft, AppDirect, WorkJam, Sunwing Airlines, Agio, and Big Fish Games.Â

He is also the founder and chief executive officer of WakaMi, an on-demand errand service platform focused on delivering reliable and efficient errand solutions to Nigerians both locally and in the diaspora.

Explain what you do to a 5-year-old.

Once upon a time, there was a big fruit garden where fruits kept falling everywhere—apples here, bananas there, and oranges rolling all over the ground. Nobody could find what they wanted.

So I became the helper of the garden. I picked up all the fruits and put them into the right baskets; apples in one basket, bananas in another, and oranges in their own place. My job is to keep everything neat, safe, and easy to find, just like the fruit baskets in the garden.

How did you become a Database Administrator?

I became a Database Administrator as part of a deliberate effort to improve my earning potential and build a more reliable career path. I joined a community of IT professionals in North America, where I was exposed to new ideas and opportunities.Â

Through that network, I discovered and enrolled in a bootcamp, completed several training sessions, and gained hands-on experience. I then applied to multiple roles, and eventually secured an opportunity that marked the beginning of my career as a Database Administrator.

If your job had a warning label, what would it say?

Warning: Unexpected issues may occur at any time. Requires patience, quick thinking, and a strong relationship with coffee.

What’s the vision behind WakaMi and why do you think a marketplace for managed services can scale in Nigeria?

The vision behind WakaMi came from a personal experience. While living in Canada, I needed someone to handle an errand for me in Nigeria. I tried finding help online, but unfortunately, I had a bad experience where I lost money.

That led me to dig deeper, and I realised this was not just my problem. Many people, especially those in the diaspora, face the same challenge. There is no reliable, structured way to get trusted services done remotely in Nigeria.

I believe it can scale in Nigeria because it addresses a real and growing problem. As more Nigerians live and work abroad, and as urban life becomes busier locally, the demand for trusted on-demand services will continue to increase.

20+ Markets. One API.

Fincra connects your business to Africa’s payment rails without building market by market. For collection, payout, FX, and settlement through a single integration. See what this means for your business.

BANKING

Ethiopia’s second-largest commercial bank has listed on the country’s stock market

Image Source: Tenor

Awash Bank, Ethiopia’s second-largest commercial bank by assets—and largest privately-owned lender—has listed on the Ethiopian Stock Exchange (ESX), the country’s stock exchange. Launched in 2025, the ESX brought the total number of stock exchanges in Africa to 30 at the time. Awash’s listing is only the third since that launch.

State of play: Awash Bank listed 37.9 million shares by introduction, out of the 54 million which it previously registered with the Ethiopian Capital Market Authority (ECMA), the country’s capital markets regulator, in March.

The listing allows Awash to provide liquidity for its existing shareholders, while diversifying its shareholder base. The listing by introduction method is typically used by companies that have listed on other stock exchanges or have recently raised capital.

In Awash’s case, the bank previously raised its paid-up capital in 2022 to ETB 55 billion (about $1 billion), a few months after Ethiopia opened up its banking sector to foreign investors.

Why this matters: Awash Bank serves over 15 million customers, runs nearly 1,000 branches, and reported a record profit of ETB 25.67 billion ($163.9 million) last year. When a company of that size goes public, investors now have a heavyweight stock to trade. It also signals confidence. If a market leader is willing to show up, others are more likely to follow.

What happens next: Awash is only the third listing on the ESX, but it likely won’t be alone for long. Other major banks are already lining up to join, with more listings expected before mid-2026.Â

Apply to Africa’s Business Heroes

Africa’s Business Heroes is calling Africa’s boldest entrepreneurs, shaping the future today. If you’re building a high-impact business, this is your moment. Apply for a chance to win a share of the $1.5M prize pool, plus mentorship and access to a powerful pan-African network. Applications close April 28. Start your journey now.

GOVERNMENT

South Africa plans a 3-year reset for its troubled State IT Agency

Image source: TechCentral

South Africa’s Department of Communications & Digital Technologies, the government agency that regulates broadcasting and communications services, has put down a three-year plan to fix the State Information Technology Agency (SITA), the state-owned IT company responsible for managing IT resources for the government.Â

Why does it need a reset? If SITA were graded for its performance, it was doing very badly. In the 2024/2025 fiscal year, in its audit, the communications regulator found that the IT agency failed to deliver R12. 1 billion ($729 million) worth of projects. The operator was struggling to function properly; a lack of staff and leadership gaps stalled multiple projects.

Now, the regulator wants to make sure SITA has no excuses in the coming fiscal year.

Rebuilding it brick by brick: The restructuring will happen in three phases. First, SITA mustdefine the problem, then diagnose what happened before designing a new framework for its operation. The third phase is a consultation with stakeholders, and then a final draft of the new business model will be presented.

Planning is the easy part: This is not the first attempt to rejig the agency. Those plans were among the institutional reform priorities for the year ended 2025. So this plan is less about what needs to be done (they already know that) and more about whether it can actually be done this time.

TECHCABAL 4.0

In March 2013, TechCabal published its first article. Thousands of stories later, the work continues, and today, it goes deeper.

TechCabal has always been free. That’s not changing.

We’ve opened a new layer. Reporting that goes further, built on sources you won’t find anywhere else, and told in ways we haven’t tried before. You’re among the first to see it.

Getting in takes less than 15 seconds.

You’re one step away from the other side.

Click the button below to see what TechCabal 4.0 looks like and what it means for you.

AI Diagnostics, a South African healthtech startup, raised 5.2 million in a funding round led by The Steele Foundation for Hope, with participation from the iFSP Group, Global Innovation Fund, and angel investors. (Apr 17)

Here are the other deals for the week:

BFree, a Nigerian fintech startup, raised $3.1 million in debt funding from undisclosed investors. (Apr 21)

Sinai.ai, an Egyptian edtech startup, raised $1.5 million in a pre-seed funding round led by KAUST Innovation Ventures and DisrupTech Ventures, with participation from Maza Ventures, YOUXEL Ventures, and several angel investors. (Apr 21)

INVIA, an Egyptian fintech startup, raised $1.2 million in seed funding from angel investors and strategic backers. (Apr 21)

Swoop, an Eswatini food delivery startup, raised $7.3 million in seed funding from Silicon Valley investors including Long Journey, Variant, Version One, Dune Ventures, Soma Capital, and Zero Knowledge Ventures. (Apr 23)

P:S If you’re often missing TC Daily in your inbox, check your Promotions folder and move any edition of TC Daily from “Promotions†to your “Main†or “Primary†folder and TC Daily will always come to you.

Swoop, an Eswatini food delivery startup, has raised $7.3 million in seed funding to support its expansion into Nigeria as it pursues its super-app model outside its home country for the first time.Â

The round, backed by Silicon Valley investors including Long Journey, Variant, Version One, Dune Ventures, Soma Capital, and Zero Knowledge Ventures, will fund the buildout of a consumer platform starting with food delivery. Walter Kortschak and Base Capital also participated.Â

Swoop, an Eswatini food delivery startup, has raised $7.3 million in seed funding to support its expansion into Nigeria as it pursues its super-app model outside its home country for the first time.Â

The round, backed by Silicon Valley investors including Long Journey, Variant, Version One, Dune Ventures, Soma Capital, and Zero Knowledge Ventures, will fund the buildout of a consumer platform starting with food delivery. Walter Kortschak and Base Capital also participated.Â

Swoop’s seed raise is one of the largest seed rounds disclosed by an African consumer startup, and nearly as large as the $9 million Series A that Chowdeck closed in August 2025 after four years of operations and expansion into 11 cities.Â

“It’s super hard to build a super app, and our investors recognise that. They recognise that you need a bit of runway and foundation to be able to do the things that you need to do operationally,†said Demola Adesina, Swoop’s Nigerian country manager.Â

Swoop believes Nigeria’s food delivery market—valued at $1.1 billion in 2025—has more room to grow than its competitors suggest. According to Nigerian payments processor Paystack, which processes payments for Swoop and all the major food delivery companies in Nigeria, the sector grew by 187% between 2021 and 2024.Â

Nigeria’s ratio of food ordered for delivery to food consumed outside the home is far lower in the country than in peer markets in Africa or Southeast Asia, and the real opportunity lies in converting non-consumers rather than poaching existing users, Adesina said.Â

“We think that the food delivery space in Nigeria is still significantly under-penetrated. Our target is not existing consumption but the users that are not consuming,†he said. “We are not getting into a war with other platforms. We are trying to grow the pie.â€

Swoop, formerly known as Thumo, launched in Eswatini in August 2025 and acquired 6,000 users in its first month, according to co-founder Aubrey Niederhoffer. Edwin Ruiz, another co-founder, told local press in Eswatini that the goal was to build a pan-African super app combining food, groceries, and rides.Â

The startup is starting with food delivery in Yaba, a neighbourhood in Lagos Mainland, already served by Chowdeck, Glovo, and FoodCourt, its competitors in Nigeria’s growing food delivery sector.Â

“There is more confidence regarding regulatory risk, and international investors committing capital to us proves that,†Adesina said. “Beyond that, I am passionate about Nigerians. There is better market education and more interest in positively changing consumer habits. We think this is the perfect time to build on that.â€

Swoop says it uses a network of independent riders rather than an employed fleet, generating revenue through commissions on restaurant sales and customer handling fees. While riders retain 100% of delivery fees, the startup applies a 7% service charge to fund operations.

Adesina declined to disclose the startup’s fee structure or unit economics, saying current fees are low because the priority is user acquisition. He added that the company is not interested in a price war.Â

“Our approach is to find the reason why some people are not consuming [through food delivery] and to make them consumers. We are not just slashing prices and getting into a price war,†he said.Â

Picking food delivery as the first vertical in a multi-product approach allows Swoop to acquire daily customers that create a habit with the app, a proven but costly growth engine for its super-app ambitions. OPay, one of Nigeria’s largest fintechs, initially bundled food delivery and ride-hailing with its payments wallet to drive daily usage for its wallet before shutting down the non-fintech products.

“Food delivery is a metric for how developed the ecosystem is. If you get food delivery right, you can essentially be the node of the ecosystem,†Adesina said.Â

“We believe that if we have a group of customers around that node, we are able to translate that into other areas and verticals,†he shared, adding that Swoop will let its users determine the next vertical to launch.Â

Nigeria’s ‘difficult’ food delivery market

Food delivery in Nigeria is a tightly contested sector that has claimed many startups and local divisions of well-funded international companies like HelloFood, Jumia Food, Bolt Food, and OFood, as the unit economics rarely work at scale. According to Jumia’s 2022 financial report, its food delivery arm lost $1.80 for every $10 it made.Â

The logistics and marketing costs exceeded the revenue made from the order, which meant Jumia was essentially paying customers and restaurants to use the service. These unit economics are a primary reason why Jumia eventually shuttered its food delivery business in late 2023.

Despite Jumia Food’s shutdown, Chowdeck, the largest food delivery platform in Nigeria, serves two million registered users with over 20,000 riders operating across 14 cities in Nigeria and Ghana while maintaining profitability, a rare feat for young food delivery startups.Â

Swoop’s strategy will require acquiring high-volume, lower-income customers on the outskirts of Lagos and in smaller cities, where local restaurants and quick-service outlets dominate, if it is to create a new set of food delivery consumers.

Whether Swoop becomes a success depends on three things: what it builds after food delivery and in what order, a monetisation strategy that ensures it is profitable, and whether it can scale beyond Yaba and Lagos before it runs out of cash.Â

Nigeria’s telecom subscribers will receive airtime refunds as compensation for poor service experienced between November 2025 and January 2026. The refunds will begin on Friday, April 24, according to the Nigerian Communications Commission (NCC).

The NCC said operators failed to meet required performance benchmarks in several parts of the country following a March 29, 2026, directive.

While this is not the first time the regulator has ordered compensation for service fai

Nigeria’s telecom subscribers will receive airtime refunds as compensation for poor service experienced between November 2025 and January 2026. The refunds will begin on Friday, April 24, according to the Nigerian Communications Commission (NCC).

The NCC said operators failed to meet required performance benchmarks in several parts of the country following a March 29, 2026, directive.

While this is not the first time the regulator has ordered compensation for service failures—MTN and Celtel (now Airtel) were fined in 2008—the latest directive signals a more assertive approach to holding telecom operators accountable.Â

The NCC said it has also directed tower companies responsible for many of the outages to channel their compensation obligations into upgrading tower infrastructure. These investments, separate from their annual capital plans, will be monitored by independent auditors to ensure compliance.

“It’s actually compensation for the quality of service experience you may have had,†NCC’s Executive Vice Chairman and chief executive officer, Aminu Maida, said at a press briefing on Thursday in Lagos, adding that subscribers will begin receiving alerts via SMS detailing the credits applied to their lines.

Unlike previous enforcement approaches, which assessed service quality at the state level, the NCC said it has shifted to a more granular system. Performance is now measured at the local government level, allowing the regulator to better capture variations in network experience across the country.

“What we have now adopted is to carry out the assessment at local government levels,†Maida said. “This ensures that whatever we measure is as close as possible to what subscribers actually experience.â€

Under this framework, operators are evaluated across multiple network layers—2G, 3G, and 4G—against key performance indicators set out in the commission’s quality of service regulations. Where operators fall short, penalties are imposed, part of which is now being redirected as compensation to affected users.

Maida acknowledged the gap between demand and current network capacity but pointed to ongoing investments by operators as a sign of progress. In 2025, the industry invested over $1 billion upgrading networks, importing equipment, and building new towers. According to Maida, one operator has already invested $1 billion in infrastructure this year.Â

“Things actually improve, but we need to be patient,†he said, noting that infrastructure expansion remains the primary driver of better service quality.

According to him, operators deployed just under 300 new sites last year. In contrast, they have committed to rolling out about 12,000 sites in 2026. So far, around 2,800 have been completed, including new builds, spectrum additions, and upgrades such as converting 3G sites to 4G and deploying 5G in select locations.

“You can see we’re already moving way ahead of what we did last year,†he said.

Operators say they are complying with the directive while continuing to invest in network improvements. MTN Nigeria said in a statement on Thursday that all affected customers will receive airtime compensation in line with the NCC framework, describing the directive as one that “places customers at the centre of regulatory decision-making.â€

While many African countries race to deploy artificial intelligence, Mauritius has made governance and ethics the starting point of its AI strategy, rather than a problem to solve after the technology is in use.

Central to the strategy is the FAIR framework, a set of guidelines that governs how AI systems are designed, deployed, and managed. It sets clear expectations across sectors and applies to the entire AI lifecycle, from design and development to deployment, monitoring, and eventual de

While many African countries race to deploy artificial intelligence, Mauritius has made governance and ethics the starting point of its AI strategy, rather than a problem to solve after the technology is in use.

Central to the strategy is the FAIR framework, a set of guidelines that governs how AI systems are designed, deployed, and managed. It sets clear expectations across sectors and applies to the entire AI lifecycle, from design and development to deployment, monitoring, and eventual decommissioning.

Mauritius’s approach reflects a broader shift in how African countries may position themselves in the AI landscape. While larger markets such as Nigeria and Kenya emphasise scale and ecosystem growth, and South Africa focuses on institutional regulation, Mauritius is advancing a governance-led model centred on enforceable standards.Â

The Mauritius National AI Strategy 2025–2029, alongside the FAIR Guidelines introduced in April 2026, is designed to be vendor-neutral and border-agnostic. Any AI system operating within the country, regardless of origin, must comply with a unified set of ethical and operational standards.

Imported AI tools are subject to the same level of scrutiny as domestic systems. The framework requires compliance with principles of fairness, accountability, inclusiveness, integrity, and responsibility. In high-risk sectors such as fintech and gaming, systems must undergo bias audits to mitigate discriminatory outcomes. Accountability provisions also require foreign providers to designate locally based representatives who can be held responsible for system outcomes.

Any AI system that affects individuals, organisations, or public interests in Mauritius falls within the framework’s scope, reflecting a recognition that AI risks are not bound by geography and that governance should be determined by impact rather than origin.

Although the FAIR Guidelines are currently non-binding, there are no immediate legal penalties or fines for non-compliance—at least not yet; they are designed with a clear legal and policy trajectory. They are expected to shape government policy, inform sector-specific regulations, influence procurement standards, and eventually underpin future legislation.Â

The Mauritius approach allows the country to remain flexible while still establishing a stable reference point for accountability. Policymakers, regulators, businesses, and even courts can rely on these principles as AI adoption expands.

The framework has four pillars: fairness, accountability, inclusiveness, and integrity. Each addresses a specific risk that has emerged in global AI deployment and is tied to concrete expectations.

Fairness focuses on preventing bias. AI systems must not discriminate based on income, gender, ethnicity, or geography, the policy stated. This is particularly important in a small and diverse society, where flawed systems could quickly exclude entire groups from access to services or opportunities. To address this, the guidelines emphasise the use of representative local datasets and require bias testing, especially in high-impact sectors such as finance and public services.

Accountability tackles one of AI’s most persistent challenges: the “black box†problem. Under the FAIR framework, there must always be a clearly identifiable party responsible for an AI system’s decisions. This includes defining liability, maintaining audit trails, and establishing mechanisms for redress when harm occurs. AI decisions are not meant to be opaque or unchallengeable.

Inclusiveness ensures that the benefits of AI are widely distributed. Rather than concentrating advantages among large firms or urban populations, the strategy promotes AI literacy through initiatives like “AI for All,†supports small and medium-sized enterprises, and expands access to digital infrastructure. The goal is to prevent a new form of inequality—what the policy’s authors describe as a potential “digital divide 2.0.â€

The final pillar, integrity and responsibility, addresses the technical and ethical robustness of AI systems. It covers data governance, privacy, cybersecurity, and safeguards against misuse, including fraud and manipulation. For a government that plans to integrate AI into public service delivery, trust in system reliability is essential.

What sets Mauritius apart is not just the inclusion of these principles, but how they are embedded into the broader economic strategy. The FAIR framework is tied directly to procurement decisions, system design, and policy development. It is positioned as a baseline requirement, not optional guidance.

It is not that South Africa and Nigeria are ignoring trust. The difference lies in priorities and timing. Mauritius is using its smaller size to position itself as a focused, “boutique†AI regulator, while South Africa and Nigeria must balance building trust with driving the scale of growth their larger economies demand.

In doing so, it hopes to attract investment, build partnerships, and integrate into global AI value chains.

The country’s economic ambitions reinforce this direction. AI is seen as a new growth pillar, alongside traditional sectors like manufacturing, whose contribution to GDP has steadily declined—from over 20% in the late 1990s to about 10.7% in 2020, and only a modest recovery to roughly 12.8% in 2024.Â

According to the policy, the country now sees AI as a way to revitalise these sectors, improve efficiency, and create new opportunities in areas such as fintech, logistics, and the ocean economy.

To drive this transformation, Mauritius is building institutional capacity in the form of an AI Council. The council would be supported by public and private sector stakeholders, and international experts, who will oversee implementation, coordinate projects, and measure socio-economic impact. Incentives such as tax credits, grants, and regulatory support are also being deployed to encourage adoption.

Mauritius, by comparison, is betting that trust can be a competitive advantage.

There are risks to this strategy. Overemphasis on governance could slow down innovation if not carefully managed. And as the guidelines transition into binding rules, questions will arise about enforcement capacity and regulatory burden. But for now, the country appears to be striking a balance, setting clear expectations without stifling experimentation.

BuuPass, a Kenyan mobility startup, is expanding beyond its consumer roots with the launch of a corporate travel platform, Gavanpass, as it looks to capture a largely undigitised segment of Africa’s enterprise economy.

The Nairobi-based company told TechCabal on Thursday that more than 20 enterprises across Kenya—including banks, fintechs, insurers, and manufacturers—are already using the platform to manage business travel.

BuuPass, a Kenyan mobility startup, is expanding beyond its consumer roots with the launch of a corporate travel platform, Gavanpass, as it looks to capture a largely undigitised segment of Africa’s enterprise economy.

The Nairobi-based company told TechCabal on Thursday that more than 20 enterprises across Kenya—including banks, fintechs, insurers, and manufacturers—are already using the platform to manage business travel.

The move marks a strategic expansion for BuuPass, which has spent the past eight years building a consumer-facing marketplace for bus, rail, and flight bookings.Â

Since its founding in 2017, the company says it has sold more than 30 million tickets and processed over $100 million in travel transactions in the past year alone, primarily across Kenya, Uganda, and South Africa.

With Gavanpass, BuuPass targets finance and procurement teams that oversee corporate travel budgets, as well as operations staff who coordinate trips. The platform integrates bookings for flights, hotels, buses, ground transfers, and group travel into a single system, while embedding approval workflows, policy controls, and real-time spend tracking.

“Finance leaders have been telling us their problem is bigger than consumer travel,†BuuPass co-founder and co-CEO Sonia Kabra told TechCabal. “They need one platform that handles everything, but also gives them the controls they actually need.â€

Corporate travel accounts for an estimated 3–5% of enterprise revenue globally, but in many African markets, the category remains heavily manual. Bookings are mostly handled via phone calls or messaging apps, while approvals are dispersed across email chains, and reconciliation can stretch weeks, particularly for companies operating in multiple currencies.

The company argues that existing global corporate travel tools are poorly adapted to African operating environments, where currency volatility, supplier fragmentation, and cross-border travel present unique challenges.

“Most enterprise software is built elsewhere and then localised,†said Wycliffe Omondi, BuuPass co-founder and co-CEO. “We built this from the ground up with African finance and procurement teams.â€

The launch comes as African startups look to enterprise software as a path to more predictable revenues, amid tougher funding conditions and rising pressure to demonstrate profitability.Â

FrontEnd Ventures, an early investor in BuuPass, said the new product reflects the founders’ track record of building products that respond to user needs.Â

“Gavanpass applies the same instinct to the enterprise market,†said Njeri Muhia, a general partner at the firm.

BuuPass plans to roll out Gavanpass across sub-Saharan Africa in the coming months, betting that regional companies—especially those with operations in multiple countries—will adopt a unified system to manage travel spend and compliance.

In the world of Kenyan elites, wristwatches are becoming the new real estate. Yes, instead of land plots, some of the crème de la crème are now putting money into pre-owned luxury watches, because apparently, you can wear your investment and flip it later for profit. What makes this wild is how much it makes sense. Unlike property, a watch doesn’t need permits or months to sell. It can be liquidated in days and carried across borders on your wrist.

If you were to invest in something unconventional, what would it be?

In other news, Nigeria’s elections have a retention problem. A new Zikoko Citizen report predicts what participation in the 2027 election might look like, drawing on trends from previous cycles, and explores what could bring about a massive turnaround.

Nigeria’s consumer protection watchdog approves five airtime lenders

Image source: The Punch

After Nigeria’s largest telecom operators MTN and Airtel temporarily suspended airtime lending last week, new players have swooped in to take their place—at least temporarily.

On Wednesday, the Federal Competition and Consumer Protection Commission (FCCPC), Nigeria’s consumer protection watchdog, approved five companies to operate airtime and data lending services: Total TIM Nigeria Limited, Rane Interactive Medien CLS Limited, Mode NG Applications Nigeria Limited, Cloud Interactive Associate Limited, and Coverage Broadband Limited.

The move comes as Globacom and T2, which round up the four telcos operating in Nigeria, have also quietly paused their own lending services, according to our checks.

Will telcos resume airtime lending? Airtime lending has not been scrapped; it is being reorganised. Under the FCCPC’s 2025 regulations, services like MTN’s Xtratime are now classified as consumer credit, requiring proper licencing, disclosure of fees, and clearer accountability.

For users, the immediate question is what happens to existing debt. Telecom operators haven’t addressed this yet.

There is another wrinkle. The newly approved lenders, it is worth noting, do not yet have listed consumer-facing apps in the FCCPC’s disclosure, making it unclear how Nigerians can actually access these services for now.

Between the lines: This is opening the door to new competition. Telcos have long dominated airtime credit, but once they secure approval and return, they may find themselves sharing that space with licenced third-party lenders operating under stricter rules.

What is really happening? Airtime credit is being pulled into the formal lending system, where the business is clearer, and the players are easier to hold accountable.

20+ Markets. One API.

Fincra connects your business to Africa’s payment rails without building market by market. For collection, payout, FX, and settlement through a single integration. See what this means for your business.

companies

M-Tiba is shutting down its health savings wallet

Image Source: M-Tiba

A curious little back story: In 2025, a cyberattack hit M-Tiba, a Kenyan healthtech platform, and went undetected for ten days. That attack exposed the personal and medical information of nearly five million Kenyans, including insurance claims, patient information, and clinical records.

What’s the news here? The same platform is now shutting down its My Health Funds (MHF) wallet, the feature that allowed people to set aside money strictly for healthcare. M-Tiba users have begun receiving refunds of the amount in the wallet into their M-PESA accounts without requesting withdrawals.

There is no confirmed link between the breach and the decision to shut down the wallet, but the timing raises eyebrows. Plus, the explanation that CarePay Limited, M-Tiba’s operator, gave is… thin. The official line is that it is evolving and will now shift its focus to “improving health insurance management.â€Â

Beyond that, there is very little detail on why the wallet is being retired, how many users were affected, no clarity on how affected users transition, and no real sense of what this new focus will look like. Will this mean deeper partnerships with insurers? A new insurance-led product? Or a full pivot away from individual users entirely? For now, it seems like a product shutdown wrapped in a vague strategy shift.Â

While one can make guesses about what might be happening behind the scenes, this is one of those moments where CarePay needs to spill a bit more tea.

TECHCABAL 4.0

In March 2013, TechCabal published its first article. Thousands of stories later, the work continues, and today, it goes deeper.

TechCabal has always been free. That’s not changing.

We’ve opened a new layer. Reporting that goes further, built on sources you won’t find anywhere else, and told in ways we haven’t tried before. You’re among the first to see it.

Getting in takes less than 15 seconds.

You’re one step away from the other side.

Click the button below to see what TechCabal 4.0 looks like and what it means for you.

Absa Kenya is spending $23.2 million on digital banking

Absa Kenya headquarters in Nairobi. Image source: Absa

Across Africa, walking into a bank branch is becoming a backup plan, as digital payments deepen. Absa Kenya, the country’s seventh-largest bank by assets, is leaning fully into that shift. The lender says it plans to spend up to KES 3 billion ($23.2 million) annually on technology as it pushes more customers toward mobile and self-service banking.

The investment is not new, but it is becoming routine. Absa spent KES 2.16 billion ($16.7 million) on technology in 2025, and now treats digital spend as a recurring cost of staying competitive. The payoff is already visible: 94% of all transactions now happen outside branches, a sharp jump from roughly 40–50% a decade ago.

This is less about innovation and more about survival. Kenya’s banking sector has long been shaped by mobile money, and customer expectations now revolve around speed, convenience, and always-on access. Traditional banks are adjusting or risking irrelevance.

What is really happening? Absa is rebuilding its retail strategy around digital channels, and leadership changes reflect that shift. The appointment of former M-Pesa Africa chief executive Sitoyo Lopokoiyit to lead personal and private banking signals where future growth is expected to come from.

The efficiency gains are starting to show. The bank’s cost-to-income ratio improved to 36.5% in 2025 from 46% a year earlier, while operating expenses dropped 21% to KES 7.35 billion ($56.9 million). At the same time, net profit rose 10% to KES 22.9 billion ($177.3 million), suggesting the digital push is not just about convenience, but also margins.

Zoom out: Kenyan banks are no longer just competing with each other. They are competing with the habits shaped by mobile money, where transactions are instant and physical branches are optional. Absa’s spending signals that keeping up now comes with a permanent technology bill.

All the technical ways to describe a cool car: The Chery Q comes with a 42.7kWh battery, up to 400km range, a peak power output of 90kW, a rear-mounted motor, and a cabin that leans heavily into screens and software, including a 15.6-inch infotainment display and a 360-degree panoramic camera.

The EV market is getting busy: South Africa’s new energy vehicles (NEV) growth was valued at R244 million ($14.3 million) in 2024, with about 3,800 units sold, as reported by Forbes Africa.

Competition in this sector is already there from Chinese automakers like BYD and Geely— which recently made its local debut at a starting price of R339,900 ($20,600). Though Chery claims some of the features of the Q car trumps those of the competitor (peak power output), its edge is that it has already built its reputation locally with its non-EV models.Â

A familiar name with a heavy past: If the Chery Q sounds familiar, it should. This is a modern reboot of the QQ3, one of the cheapest cars South Africa had seen when it first arrived in 2008. It was cheap, only going for R59,900 ($3,600) at the time.Â

However, these cars received a zero-star safety rating in a South African car safety campaign conducted by the Global New Car Assessment Programme (NCAP). While this new version has history, the Chery Q is now getting a second chance to meet a higher safety and car quality expectation.

CRYPTO TRACKER

The World Wide Web3

Source:

Coin Name

Current Value

Day

Month

Bitcoin

$77,800

– 0.62%

+ 10.90%

Ether

$2,343

– 2.30%

+ 10.01%

XRP

$1.41

– 2.92%

+ 0.35%

Solana

$85.84

– 2.65%

– 4.73%

* Data as of 06.34 AM WAT, April 23, 2026.

Events

The voices shaping Africa’s digital future are taking the stage. From AI and IoT to cloud, connectivity and smart infrastructure, IOT West Africa | Data Centre & Cloud Expo Africa 2026 brings together the leaders building the continent’s next digital chapter. This is where the ecosystem meets, and we’ll see you there. The event kicks off on April 28–30 at the Landmark Centre, Victoria Island, Lagos. Register here to attend.

All roads lead to Nairobi on May 7, 2026. Gathered at the Sarit Expo Centre, senior leaders from across Africa’s fintech and payments ecosystem will gather for a day of meaningful connections, market insights, and cross-border collaboration. The focus of the Africa Fintech Live event is on driving real engagement, bringing together industry leaders and emerging innovators to spark strategic conversations that will shape the future of finance on the continent. Secure your early bird ticket now at 50% off

On May 6–8, 2026, policy, capital, and innovation in Africa will take centre stage at the 3i Africa Summit. Happening at the Destiny Arena, Accra, Ghana, it will pack operators, investors, and policymakers in one room to answer questions about the continent’s integrated fintech future, and what it’s still missing. Register here to attend.

The Africa Tech Summit London 2026 is back for its 10th edition. Held at the London Stock Exchange building in London on May 29, it will feature 350 attendees from over 200 companies, the event will be a small, high-impact gathering of founders, investors, and global partners driving the future of tech in Africa. Use the code TC10 to get 10% off tickets. Apply to attend.

P:S If you’re often missing TC Daily in your inbox, check your Promotions folder and move any edition of TC Daily from “Promotions†to your “Main†or “Primary†folder and TC Daily will always come to you.

Absa Bank Kenya will spend up to KES 3 billion ($23.2 million) a year on technology to deepen its digital strategy, according to a Business Daily report, as the lender seeks to move more customer activity to mobile and other self-service channels.

The bank said the recurring investment will make transactions easier and support its push into digital banking, even as competition intensifies and customer expectations shift away from branches.

The change reflects a broader migration across Ke

Absa Bank Kenya will spend up to KES 3 billion ($23.2 million) a year on technology to deepen its digital strategy, according to a Business Daily report, as the lender seeks to move more customer activity to mobile and other self-service channels.

The bank said the recurring investment will make transactions easier and support its push into digital banking, even as competition intensifies and customer expectations shift away from branches.

The change reflects a broader migration across Kenya’s banking sector towards mobile and self-service channels, a trend accelerated by the country’s entrenched mobile money ecosystem and rising expectations for instant, always-on financial services.

“Typically, we now do KES 2 billion ($15.4 million) to KES 3 billion ($23.2 million) of investments per year [in technology], and 2025 was no different in ensuring we are migrating transactions to digital platforms. We are making it easier for our customers to transact with us,†Absa Kenya chief executive Abdi Mohamed told Business Daily.

The bank spent KES 2.16 billion ($16.7 million) on technology in 2025, underscoring how quickly digital investment has become a fixed cost in its operations. About 94% of all transactions in 2025 took place outside branches, compared with roughly 40–50% a decade ago, according to the lender.

The technology push comes as Absa continues to reshape parts of its consumer banking leadership around digital banking. In February, the bank appointed former M-Pesa Africa chief executive Sitoyo Lopokoiyit to head its personal and private banking division, a move widely read as a signal of where it expects retail growth to come from.

Lopokoiyit, who built his reputation overseeing the expansion of M-Pesa, is expected to bring mobile banking experience to retail and affluent banking at a time when the boundaries between banks and fintechs are becoming blurred.

Efficiency gains

The efficiency gains are already visible in the bank’s cost base. Other operating expenses fell 21% to KES 7.35 billion ($56.9 million) in the year to December 2025, with management attributing much of the decline to digitisation and automation. The impact of the technology push has also been reflected in performance metrics.

Absa’s cost-to-income ratio—a measure of banking efficiency—improved to 36.5% in 2025 from 46% a year earlier, helped by lower costs and improved revenue generation.

Net profit rose 10% to KES 22.9 billion ($177.3 million) over the period, suggesting that efficiency gains from digitisation are beginning to support bottom-line growth, even as investment spending remains elevated.

M-TIBA, a mobile health platform run by Kenya-based healthtech startup CarePay, is shutting down its My Health Funds (MHF) wallet that lets customers set aside money specifically for healthcare.

On April 8, users began receiving refunds directly into their M-PESA wallets without initiating withdrawals, indicating payouts are already underway. Five M-TIBA users confirmed to TechCabal that they had received the funds.

The decision marks a shift in M-TIBA’s model, from a co

M-TIBA, a mobile health platform run by Kenya-based healthtech startup CarePay, is shutting down its My Health Funds (MHF) wallet that lets customers set aside money specifically for healthcare.

On April 8, users began receiving refunds directly into their M-PESA wallets without initiating withdrawals, indicating payouts are already underway. Five M-TIBA users confirmed to TechCabal that they had received the funds.

The decision marks a shift in M-TIBA’s model, from a consumer health savings wallet to an insurance management platform. The move, however, leaves users who depended on the service to set aside small amounts for care without a clear alternative for planning or paying for treatment.

CarePay declined to comment for this story.

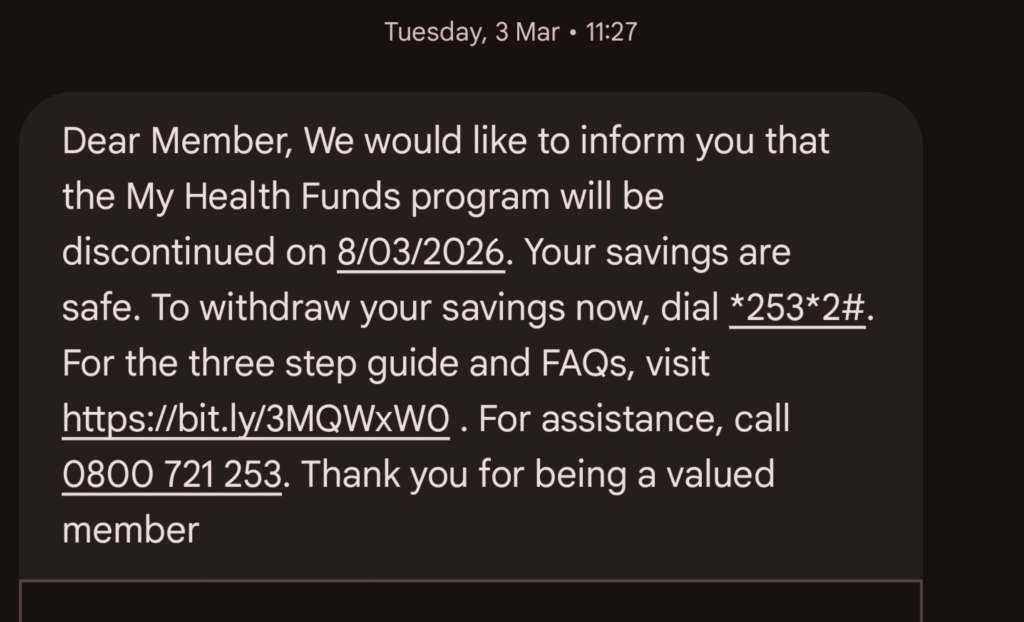

M-TIBA first informed users on March 3 via SMS and its website that the MHF wallet would be discontinued, stating that access to insurance benefits on the platform would remain unchanged.

An SMS from M-TIBA notifying users about the discontinuation of the MHF wallet. Source: Screenshot from an M-TIBA user

Users were asked via SMS to withdraw their balances via USSD or receive M-PESA refunds by March 8, 2026. M-TIBA also said it would process refunds using verified details, with any unresolved balances sent to the Unclaimed Financial Assets Authority, the government agency that holds unclaimed funds until owners come forward.

Refunds began on April 8, and users who had not withdrawn their balances by the March 8 deadline received their wallet savings automatically.

On its website, CarePay said withdrawals would be free, and funds would remain safe, but did not fully explain why the savings product is being retired.

“M-TIBA has some exciting updates on how we’re evolving to better serve you and millions of others,†the company said on its website, without providing further detail.

Launched in 2015, M-TIBA built its early momentum on the idea of ringfencing healthcare funds so they cannot be spent elsewhere. The MHF wallet allowed individuals, employers, and donors to allocate money strictly for medical use across a network of providers. It provided an option for users who could not afford insurance but wanted a structured way to save for care.

CarePay said on its website it will focus on “improving health insurance management,†pointing to a model where insurers and partners drive usage rather than individual savings.

“Since we launched the M-TIBA wallet, we’ve helped many people save and access healthcare, and thanks to your trust, we’re growing into something even bigger and better,†CarePay said on its website. “That’s why we aim to focus on improving health insurance management to ensure more people get access to more affordable healthcare and a better experience.â€

CarePay has not disclosed how many users are affected, the total value of refunds, or how many accounts may be transferred to the Unclaimed Financial Assets Authority due to failed verification. It has not outlined clear alternatives for users who cannot transition to insurance products. The shutdown follows scrutiny in 2025 after a cyber attack exposed user data, as reported by TechCabal. M-TIBA said it will delete personal data once MHF accounts are closed, in line with its privacy policy. It has yet to disclose whether the decision is linked to security, compliance, or cost pressures.

Introducing… WhatsApp Premium (because money must be made).

You read that right. WhatsApp is testing paid subscriptions that unlock features like more pinned chats, custom app icons, themed interfaces, and exclusive ringtones and stickers. Fun, but we’ll see how that plays out.

South Africa’s communication regulator, the Independent Communications Authority of South Africa (ICASA), is also side-eyeing the platform and other over-the-top (OTT) services like Netflix. The focus is to open a market inquiry into whether these services are eating into the space that traditional broadcasters once dominated, and what that means for competition and regulation. Findings are expected after the 2026/2027 financial year.

Fingers crossed for whatever ICASA finds.

In other news, Nigeria’s elections have a retention problem. A new Zikoko Citizen report predicts what participation in the 2027 election might look like, drawing on trends from previous cycles, and explores what could bring about a massive turnaround.

Nigeria’s Central Bank and telecoms regulator team up to give banks real-time access to telecom data

Aminu Maida, the EVC of Nigerian Communications Commission (Middle) and Cardoso Olayemi, the Governor the Central Bank (Right) of Nigeria during the signing of the MoU. Image source: NCC

Financial fraud in Nigeria has gone beyond stealing passwords or tricking people into sending over sensitive financial information. SIM cards are now identity anchors used in financial services; recycled or swapped phone numbers have become a sort of back door for fraudsters to intercept one-time passwords (OTPs) and move money before anyone notices. The impact is ₦52.26 billion ($37.86 million) in losses in 2024.

Now, the Central Bank of Nigeria (CBN) and the Nigerian Communications Commission (NCC), the country’s telecoms regulator, have signed a new agreement that would allow banks to check mobile number activity before a transaction goes through.

How would it work? At the centre of this partnership is something called the Telecom Identity Risk Management System (TIRMS), a centralised platform designed to track and verify the risk status of mobile numbers. With this new setup, banks can see what’s going on behind a phone number in real-time: whether it has been recently altered, reassigned, flagged for suspicious activity, or is inactive. It’s like sharing intelligence.

What does peeking into this data do? With real-time verification, banks can flag risky transactions before they happen. It will increase scrutiny on phone numbers that show signs of compromise in the system. This could mean that banks can pause authentication steps or transactions tied to those phone numbers before money is transferred.Â

Will this reduce fraud? Though this additional data will close a huge gap for banks, it is not a standalone fix. It will likely make it harder for attackers to exploit one of the most common entry points, and frankly, easy-to-obtain methods of identity farming, which are mobile numbers.Â

However, the extent of regulatory oversight is still unknown. It is unclear whether banks, for example, will have autonomy to report compromised phone numbers to law enforcement agencies, or how they will handle such cases.

This matters because fraud cases succeed when systems are disconnected. This collaboration could reduce fraud vulnerabilities.

20+ Markets. One API.

Fincra connects your business to Africa’s payment rails without building market by market. For collection, payout, FX, and settlement through a single integration. See what this means for your business.

Cryptocurrency

Kenya freezes accounts of Binance users

Image Source: Zikoko Memes

POV: you’re a Binance user in Kenya, and you wake up to check if your trades are up or down, or maybe even cash out. But suddenly, you can’t access your account or move anything.

It’s not a glitch: Kenya’s Directorate of Criminal Investigations (DCI), an investigative agency, has moved to freeze an undisclosed number of Binance accounts, in a crackdown on crypto-linked fraud, money laundering, and suspected terrorism financing. Binance has told affected users that the restrictions came at the request of authorities.

Crypto must conform: Kenya is under pressure to tighten its financial controls and exit the Financial Action Task Force (FATF) grey list, following Nigeria and South Africa’s exits in October 2025. This list flags countries with gaps in anti-money laundering controls, including crypto.Â

The Virtual Asset Service Providers (VASP) Act, passed in 2025, will regulate virtual asset businesses in the country by bringing exchanges and intermediaries under formal oversight. Freezes on accounts such as this seem like early enforcement; authorities acting on suspected risks even as the full regulatory framework is still being operationalised.Â

What happens to the frozen accounts? That really depends on what investigators find. Once an account is flagged on such suspicions, it stays restricted while investigations are ongoing.Â

Authorities may request transaction histories, identity verification, and links to other flagged accounts to determine whether the funds are tied to illicit activity. Access to their accounts can be restored if they are cleared. Otherwise, their funds could remain frozen for a longer time or be subject to forfeiture under anti-money laundering laws.

20+ Markets. One API.

Breet is offering a $10,000 equity-free grant to growth-stage fintech, crypto and payments startups in Africa. Integrate the API, submit your product, and pitch live at ATE Lagos. Two winners get $5,000 each. Deadline by May 31. Learn more.

Regulation

South Africa takes aim at Netflix and WhatsApp as TV money dries up

Image Source: Zikoko Memes

South Africans are watching less traditional TV and spending more time on Netflix and WhatsApp, and the regulator is starting to ask whether that balance is fair.Â

The Independent Communications Authority of South Africa (ICASA), the telecoms and ICT regulator, now plans to investigate how over-the-top (OTT) platforms, like streaming and messaging services, are affecting broadcasting revenue, just as the country’s pay-TV market slipped below 7 million subscribers for the first time in five years.

The regulator says services like Netflix, YouTube, and WhatsApp are no longer simple “alternatives†to television, but direct competitors for both audiences and advertising income. Its upcoming market inquiry will look at whether this shift is weakening the financial base of licenced broadcasters. While we smell a fish behind this plan, we still wonder what will come out of this. If OTT streaming platforms like Netflix are, indeed, found guilty, what’s a realistic way to ensure market control or fairness?

Between the lines: This is where the debate turns uncomfortable for traditional media. Pay-TV operators argue that while they carry regulatory obligations, global platforms operate in South Africa without the same rules, yet still pull away viewers and ad spend. Competitive tension is now being packaged under “fair share†discussions.

What is really happening? Telecom operators in South Africa, through the industry body Association of Comms and Technology (ACT), want streaming and messaging platforms to contribute to network costs, arguing that services like Netflix and WhatsApp only work because broadband infrastructure exists in the first place. ICASA will weigh this against broader policy changes already being drafted by the government, including possible content quotas and tax reviews for global streaming platforms.

Zoom out: The timing matters. Traditional broadcasting is shrinking, streaming is growing, and messaging apps have become a default communication layer. ICASA is stepping into a market where old revenue models are already under pressure, and trying to decide who should pay for the infrastructure behind it all, and how much.

TECHCABAL 4.0

In March 2013, TechCabal published its first article. Thousands of stories later, the work continues, and today, it goes deeper.

TechCabal has always been free. That’s not changing.

We’ve opened a new layer. Reporting that goes further, built on sources you won’t find anywhere else, and told in ways we haven’t tried before. You’re among the first to see it.

Getting in takes less than 15 seconds.

You’re one step away from the other side.

Click the button below to see what TechCabal 4.0 looks like and what it means for you.

South African carmakers sold a record 664 plug-in hybrid electric cars in March

Image Source: Tenor

South Africans are slowly realising that petrol stations are not the only place to fill up anymore, and plug-in hybrids are starting to reflect that shift in a way that is finally showing up in the numbers.

March marked a record month for plug-in hybrid electric vehicle (PHEV) sales in the country, with 664 units sold, according to the National Association of Automobile Manufacturers of South Africa (Naamsa), the industry group for carmakers.

Why it matters: It is a 130% jump from February and comfortably above the previous record set in September 2025. In Q1 2026, South African carmakers sold over 1,200 PHEVs, already outpacing Q1 2025 levels, and pointing to a market that is picking up speed rather than drifting. The uptake also comes amid petrol price hikes in South Africa, where it increased by 20 cents per litre in March. Another planned petrol hike is already underway in April.

Between the lines: This is not happening in a vacuum. The fuel price pressure and a wave of more affordable Chinese models are doing most of the heavy lifting. Until recently, plug-in hybrids were firmly in the luxury bracket. Now, several options are landing between R500,000 and R1 million, pulling them closer to mainstream buyers.

What is really happening? BYD, the Chinese EV manufacturer, is leading the charge, followed closely by Chery and its sister brands Omoda and Jaecoo. BMW, Volvo, and a handful of legacy automakers are still present, but the centre of gravity is clearly shifting toward Chinese manufacturers offering cheaper, feature-heavy alternatives.

Zoom out: PHEVs sit in a strange middle ground. They are not fully electric, but they offer enough electric driving range to meaningfully cut fuel use for typical daily commutes. In a country where most drivers cover under 50km a day, that hybrid flexibility is starting to feel less like a compromise and more like a practical option.

CRYPTO TRACKER

The World Wide Web3

Source:

Coin Name

Current Value

Day

Month

Bitcoin

$78,043

+ 2.90%

+ 13.83%

Ether

$2,389

+ 3.04%

+ 15.53%

OpenGradient

$0.3773

+ 97.10%

+ 97.10%

Solana

$87.87

+ 2.74%

+ 1.12%

* Data as of 06.30 AM WAT, April 22, 2026.

Opportunities

Applications are open for ClimateLaunchpad, the world’s largest green business ideas competition run by Climate-KIC. The programme helps early-stage climate founders turn rough ideas into viable startups through training, mentorship, and pitch competitions. Entrepreneurs from around the world, including Africa, can apply for the 2026 cohort and compete for up to €10,000 in prize money and access to a global cleantech network. Apply here.

Google for Startups: Africa, a three-month hybrid accelerator for growth-stage startups on the continent, is now accepting applications. The accelerator will provides equity-free support for the duration of the programme, mentorship, training, cloud credits, and access to Google’s AI products designed to bring the best of its programmes, products, people, and technology to communities across Africa. Apply here.

Google and UpSkill Universe have partnered to relaunch Hustle Academy, now offering free AI and business training to individuals and small businesses across Africa. The programme features 60-minute expert-led webinars and 1-day bootcamps (3–5 hours), covering digital marketing, e-commerce, business strategy, financial management, and AI tools. Open to students, jobseekers, entrepreneurs, and past applicants, it provides practical, hands-on skills that can be immediately applied to grow careers or businesses. Apply here.

P:S If you’re often missing TC Daily in your inbox, check your Promotions folder and move any edition of TC Daily from “Promotions†to your “Main†or “Primary†folder and TC Daily will always come to you.

The money had just hit Sylvia Wanjiru’s account when her phone rang. It was a million-shilling ($7,773) payment from a client, and the caller claimed to be from her bank’s customer service. He spoke confidently, offering to “help confirm the transaction.â€

“At first I thought it was just a coincidence,†Wanjiru recalls. But when the same thing happened again, she realised someone was wa

The money had just hit Sylvia Wanjiru’s account when her phone rang. It was a million-shilling ($7,773) payment from a client, and the caller claimed to be from her bank’s customer service. He spoke confidently, offering to “help confirm the transaction.â€

“At first I thought it was just a coincidence,†Wanjiru recalls. But when the same thing happened again, she realised someone was watching her transactions and reported it to the bank.

Her parents were not so fortunate. Pension payments of KES 34,000 ($263) and KES 2,500 ($19) from a mobile money wallet disappeared after they called a number that texted: “*** BANK. Dear Customer, your account has been SUSPENDED. Please contact 010****366 within 24 hours.â€Â Â

The money was long gone by the time they rushed to the bank and mobile money provider. Wanjiru’s experience is one among many others. Across Kenya, customers report similar encounters, including calls moments after cash deposits or transfers and text messages disguised as official alerts followed by withdrawals.

The speed and timing point to a possibility that the fraudsters work hand in glove with bank staff and mobile money agents with access to customer information.

Rising cyber-threats

The Central Bank of Kenya (CBK), in its Financial Sector Stability Report 2025, in August reports cases of cyber fraud in the banking sector more than doubled in 2024, rising from 153 to 353, with the amount exposed increasing to KES 1.9 billion ($14.7 million) and losses nearly quadrupling to KES 1.5 billion ($11.6 million).

The Communications Authority of Kenya (CA) reported 7.9 billion cyber threats in the first eight months of 2025, double the figure for 2024. CBK said attacks rose from 7.7 million in 2016 to billions due to Kenya’s economy’s rapid digitisation.

The regulator insists that despite rising risks, Kenya’s banking sector remains “resilient,†able to withstand shocks from successful cyber-attacks. However, accounts from victims, bank staff, and law enforcement suggest that most losses of funds are inside jobs.

A former compliance officer described a shadow industry in Nairobi neighbourhoods like Utawala and Ruiru, which thrives on mobile banking fraud. The setups look like call centre outsourcing hubs with rows of desks, computers, and phones.

“There are bank staff who monitor accounts, tip off the fraudsters, and within minutes, money is pushed into mule accounts,†says one ex-risk and compliance at a major bank. The cash is laundered through mobile money wallets and withdrawn at agents, or some are pushed to crypto wallets.

With 67% youth unemployment, workers are recruited through job ads for “customer service†roles, only to discover that the scripts involve impersonating bank officials or mobile money agents. And because it’s quick cash, many stay.

Pay is per successful hit, which means the more money they steal from customers, the more they earn. Corrupt police officers, according to the former compliance officer, are paid to protect operations, tip off the syndicates before raids, or frustrate investigations.

“It’s a big operation, more than you can imagine,†the former officer says. “The real people behind these schemes are known to some in Kenya Police’s serious crimes division.â€

Targets the biggest banks

The people behind the schemes design them for scale, according to an investigations officer at Banking Fraud Investigations Unit (BFIU)—a unit under the Directorate of Criminal Investigations (DCI)—who has handled such cases and asked not to be named. They target banks with vast retail business like Equity Bank, KCB Group, and Co-operative Bank— Kenya’s biggest retail lenders with a combined customer base of over 50 million. With such big operations, the fraudsters hide in the noise of millions of daily transactions.

Rural pensioners, urban traders, and salaried workers with predictable income streams make easy prey.

“It’s a numbers game,†says the BFIU officer. “The bigger the bank, the more likely someone will slip.â€

Most of these frauds are not violent, but sometimes they turn deadly. In April, a teacher in Mumias was trailed and killed after withdrawing KES 285,000 ($206). Detectives believe two bank tellers may have passed on the information to robbers, pointing to insider collusion with criminals.

There are numerous reports of customers being trailed after withdrawing or depositing large sums at banks and mobile money agents across the country.

In 2024, Equity Bank reported it lost KES 1.5 billion ($11.6 million) in what was initially described by news outlets as a sophisticated hacking attack. However, investigators later alleged that bank staff colluded with property developers and lawyers to siphon off the bank’s money from the salary suspense account in thousands of small, salary-like transfers to avoid detection.

Deeper rot

On social media, many Kenyans brush off mobile banking fraud as the work of prisoners with smuggled phones when they are operations run by people living among them. While some operations enjoy corrupt officials’ backing, the BFIU officer concedes that the regulators are overstretched.

“Mobile money and banks process millions of payments daily, and that’s why some of the cases even go unnoticed,†says the officer.

However, faced with mounting fraud, most Kenyan banks have begun housecleaning to restore customer confidence. KCB Group, NCBA, Absa, and Co-operative Bank are some lenders that have recently fired staff over misconduct.

In May, Equity Group took a bolder step, announcing publicly that it was firing 1,500 staff to protect the bank’s image and its customers.

“The moment of reckoning has come,†Equity Bank CEO James Mwangi said in May. “It doesn’t matter how many I will lose. I don’t even care. I will protect the customers and the bank. I will be ruthless.â€

The bank has since extended the exercise to its subsidiary in Uganda, which has also suffered staff-linked fraud in the past two years.

Blurring of lines

The lines between cyber fraud, insider theft, and organised crime are blurred. According to the BFIU officer, most victims never report, whether from embarrassment, the small sums involved, or the hassle of filing a complaint with the police, making the CBK’s figure of KES1.5 billion an understatement.

The BFIU investigator says the schemes rarely fall into specific categories. A phishing text may be the start, but a bank teller can pass on stolen data, laundered through mobile money, and protected by police officers. Each stage blurs the line between cyber-attacks, insider theft, and organised racketeering.

The consequence, the former compliance officer warns, is erosion of trust. Many customers, unsure whether the fraudsters are hackers or someone inside their bank, choose not to report. Anxious to reassure shareholders and depositors, lenders frame the losses as “cyber threats†even when investigations show human hands.

This gap between the official narrative and what victims experience is where the danger lies. The BFUI investigator says that as Kenya’s financial system grows, the weakest link may be the people inside—tellers, agents, and officers with access to real-time customer records. Â

Mark your calendars! Moonshot by TechCabal is back in Lagos on October 15–16! Meet and learn from Africa’s top founders, creatives & tech leaders for 2 days of keynotes, mixers & future-forward ideas. Get your tickets now: moonshot.techcabal.com

Table of contents

The types of SASSA social grants

How to apply for the SASSA SRD R350 grant

How to check your SASSA status online

How to change your SASSA banking details

How to change your SASSA phone number

How to check your SASSA balance

SASSA payment dates for October 2025

SASSA child support grant amount for 2025

SASSA old-age grant amount for 2025

The South African Social Security Agency (SASSA) was established by the South African government in 2005 und

The South African Social Security Agency (SASSA) was established by the South African government in 2005 under the Social Assistance Act of 2004, with the primary goal of administering and managing the payment of social assistance grants to the country’s poor and vulnerable citizens.

SASSA handles everything from processing applications and checking eligibility to paying grants and fraud prevention. Its centralised system is designed to make it easier for South Africans to access support once they qualify.

The types of SASSA social grants

SASSA offers different grants depending on your situation. SASSA pays 26-million grants monthly to help reduce poverty and hardship. The central grants include:

Support for children and caregivers

Child Support Grant (CSG): For the primary caregiver of a child under 18.

Foster Child Grant: For people legally appointed as foster parents.

Care Dependency Grant: For caregivers of children under 18 with severe disabilities.

Support for adults

Older Persons Grant: Also known as the state pension, for South Africans aged 60 and above.

Disability Grant: For individuals aged 18 to 59 with a disability that prevents them from working.

War Veteran’s Grant: For former members of the armed forces.

Grant-in-Aid: Extra support for people already receiving a central grant but who need full-time care.

Temporary support

Social Relief of Distress (SRD) Grant: Often called the SASSA R350 grant, this temporary grant is for unemployed people with no other source of income or social assistance.

How to apply for the SASSA SRD R350 grant

The Social Relief of Distress (SRD) grant, often called the SASSA R350 grant, was first introduced during the COVID-19 pandemic to help unemployed South Africans. In 2025, the amount has increased to R370 per month. This shows that the government now treats it as more than just short-term help; it is ongoing support for people without income.

Eligibility requirements for 2025

To qualify for the SRD grant in 2025, you must meet these conditions:

Be a South African citizen, permanent resident, refugee, asylum seeker, or special permit holder living in South Africa.

Be between 18 and 60 years old.

Be unemployed and not receiving any other SASSA grant, UIF payments, or NSFAS funding.

Pass the means test, which checks that your monthly income is R624 or less.

Step-by-Step online application (2025)

You can only apply online. Applications are free, and SASSA warns people not to pay anyone to apply on their behalf. Here’s how to do it:

Select your ID type: Choose if you’re a South African ID holder or applying with an asylum/special permit.

Enter your phone number: You’ll get a One-Time Pin (OTP) to confirm your identity.

Fill in your details: Provide your ID number, full name, and contact information.

Choose a payment method: Payments can go into your bank account or be collected at stores like Pick n Pay or Shoprite.

Submit your application: Double-check your details before submitting. SASSA will then check your financial records against government and banking databases.

How to check your SASSA status online

After applying, you’ll want to know if your grant is approved and when payments will be made. You can check your SASSA SRD status using any of these official methods:

SRD website: Visit srd.sassa.gov.za, enter your ID number and phone number, and view your application status.

WhatsApp: Send “status†to 082 046 8553, then follow the prompts.

USSD code: Dial 1347737# on your phone, then enter your details.

SASSA Call Centre: Call 0800 60 10 11 to speak with an agent who will verify your details and confirm your status.

Moya App: Download the Moya App to check your SRD status without using mobile data.

How to change your SASSA banking details

Keeping your SASSA banking details up to date is essential to avoid interruptions in your grant payments. The update process depends on the type of grant: SRD grant recipients can update details online, while those on permanent grants — such as the Older Person’s Grant, Disability Grant, or Child Support Grant — must visit a SASSA office.Â

Changing banking details for the SRD grant (Online)

If you are an SRD grant beneficiary, you can update your banking details through the official SRD website. Here’s how:

Provide your new bank name, account number, and any other required details. Double-check for accuracy to avoid payment delays.