Africa’s leading policymakers, innovators, and technology leaders are set to converge in Nairobi for the highly anticipated Connected Africa Summit...

Artificial Intelligence (AI), Digital Public Infrastructure (DPI), and cybersecurity will headline discussions at the Connected Africa Summit 2026, taking place...

Jomo Kenyatta University of Agriculture and Technology (JKUAT) hosted its flagship NextGen Technopreneur Forum, bringing together students, industry leaders, and...

Put a finger down if you experienced poor service with Nigerian telecom operators between November 2025 and January 2026.

The Nigerian Communications Commission (NCC), the country’s telecoms regulator, has said that subscribers will receive airtime refunds as compensation for poor service experienced within the said time.

In other news, Nigeria’s elections have a retention problem. A new Zikoko Citizen report predicts what participation in the 2027 election might look like, drawing on trends from previous cycles, and explores what could bring about a massive turnaround.

Kolawole Bekes is a Database Administrator, Database Reliability Engineer, and DevOps Engineer with over a decade of experience spanning multiple industries. He holds a Bachelor’s degree in Mathematics from the University of Abuja. Following his relocation to the United States in 2015 and subsequently to Canada in 2017, he has built a career working with organisations such as Microsoft, AppDirect, WorkJam, Sunwing Airlines, Agio, and Big Fish Games.Â

He is also the founder and chief executive officer of WakaMi, an on-demand errand service platform focused on delivering reliable and efficient errand solutions to Nigerians both locally and in the diaspora.

Explain what you do to a 5-year-old.

Once upon a time, there was a big fruit garden where fruits kept falling everywhere—apples here, bananas there, and oranges rolling all over the ground. Nobody could find what they wanted.

So I became the helper of the garden. I picked up all the fruits and put them into the right baskets; apples in one basket, bananas in another, and oranges in their own place. My job is to keep everything neat, safe, and easy to find, just like the fruit baskets in the garden.

How did you become a Database Administrator?

I became a Database Administrator as part of a deliberate effort to improve my earning potential and build a more reliable career path. I joined a community of IT professionals in North America, where I was exposed to new ideas and opportunities.Â

Through that network, I discovered and enrolled in a bootcamp, completed several training sessions, and gained hands-on experience. I then applied to multiple roles, and eventually secured an opportunity that marked the beginning of my career as a Database Administrator.

If your job had a warning label, what would it say?

Warning: Unexpected issues may occur at any time. Requires patience, quick thinking, and a strong relationship with coffee.

What’s the vision behind WakaMi and why do you think a marketplace for managed services can scale in Nigeria?

The vision behind WakaMi came from a personal experience. While living in Canada, I needed someone to handle an errand for me in Nigeria. I tried finding help online, but unfortunately, I had a bad experience where I lost money.

That led me to dig deeper, and I realised this was not just my problem. Many people, especially those in the diaspora, face the same challenge. There is no reliable, structured way to get trusted services done remotely in Nigeria.

I believe it can scale in Nigeria because it addresses a real and growing problem. As more Nigerians live and work abroad, and as urban life becomes busier locally, the demand for trusted on-demand services will continue to increase.

20+ Markets. One API.

Fincra connects your business to Africa’s payment rails without building market by market. For collection, payout, FX, and settlement through a single integration. See what this means for your business.

BANKING

Ethiopia’s second-largest commercial bank has listed on the country’s stock market

Image Source: Tenor

Awash Bank, Ethiopia’s second-largest commercial bank by assets—and largest privately-owned lender—has listed on the Ethiopian Stock Exchange (ESX), the country’s stock exchange. Launched in 2025, the ESX brought the total number of stock exchanges in Africa to 30 at the time. Awash’s listing is only the third since that launch.

State of play: Awash Bank listed 37.9 million shares by introduction, out of the 54 million which it previously registered with the Ethiopian Capital Market Authority (ECMA), the country’s capital markets regulator, in March.

The listing allows Awash to provide liquidity for its existing shareholders, while diversifying its shareholder base. The listing by introduction method is typically used by companies that have listed on other stock exchanges or have recently raised capital.

In Awash’s case, the bank previously raised its paid-up capital in 2022 to ETB 55 billion (about $1 billion), a few months after Ethiopia opened up its banking sector to foreign investors.

Why this matters: Awash Bank serves over 15 million customers, runs nearly 1,000 branches, and reported a record profit of ETB 25.67 billion ($163.9 million) last year. When a company of that size goes public, investors now have a heavyweight stock to trade. It also signals confidence. If a market leader is willing to show up, others are more likely to follow.

What happens next: Awash is only the third listing on the ESX, but it likely won’t be alone for long. Other major banks are already lining up to join, with more listings expected before mid-2026.Â

Apply to Africa’s Business Heroes

Africa’s Business Heroes is calling Africa’s boldest entrepreneurs, shaping the future today. If you’re building a high-impact business, this is your moment. Apply for a chance to win a share of the $1.5M prize pool, plus mentorship and access to a powerful pan-African network. Applications close April 28. Start your journey now.

GOVERNMENT

South Africa plans a 3-year reset for its troubled State IT Agency

Image source: TechCentral

South Africa’s Department of Communications & Digital Technologies, the government agency that regulates broadcasting and communications services, has put down a three-year plan to fix the State Information Technology Agency (SITA), the state-owned IT company responsible for managing IT resources for the government.Â

Why does it need a reset? If SITA were graded for its performance, it was doing very badly. In the 2024/2025 fiscal year, in its audit, the communications regulator found that the IT agency failed to deliver R12. 1 billion ($729 million) worth of projects. The operator was struggling to function properly; a lack of staff and leadership gaps stalled multiple projects.

Now, the regulator wants to make sure SITA has no excuses in the coming fiscal year.

Rebuilding it brick by brick: The restructuring will happen in three phases. First, SITA mustdefine the problem, then diagnose what happened before designing a new framework for its operation. The third phase is a consultation with stakeholders, and then a final draft of the new business model will be presented.

Planning is the easy part: This is not the first attempt to rejig the agency. Those plans were among the institutional reform priorities for the year ended 2025. So this plan is less about what needs to be done (they already know that) and more about whether it can actually be done this time.

TECHCABAL 4.0

In March 2013, TechCabal published its first article. Thousands of stories later, the work continues, and today, it goes deeper.

TechCabal has always been free. That’s not changing.

We’ve opened a new layer. Reporting that goes further, built on sources you won’t find anywhere else, and told in ways we haven’t tried before. You’re among the first to see it.

Getting in takes less than 15 seconds.

You’re one step away from the other side.

Click the button below to see what TechCabal 4.0 looks like and what it means for you.

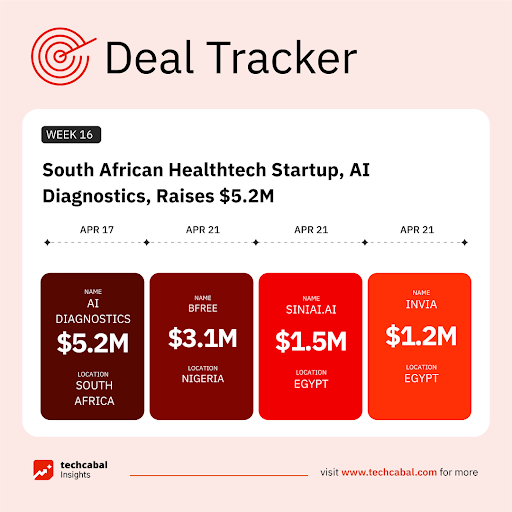

AI Diagnostics, a South African healthtech startup, raised 5.2 million in a funding round led by The Steele Foundation for Hope, with participation from the iFSP Group, Global Innovation Fund, and angel investors. (Apr 17)

Here are the other deals for the week:

BFree, a Nigerian fintech startup, raised $3.1 million in debt funding from undisclosed investors. (Apr 21)

Sinai.ai, an Egyptian edtech startup, raised $1.5 million in a pre-seed funding round led by KAUST Innovation Ventures and DisrupTech Ventures, with participation from Maza Ventures, YOUXEL Ventures, and several angel investors. (Apr 21)

INVIA, an Egyptian fintech startup, raised $1.2 million in seed funding from angel investors and strategic backers. (Apr 21)

Swoop, an Eswatini food delivery startup, raised $7.3 million in seed funding from Silicon Valley investors including Long Journey, Variant, Version One, Dune Ventures, Soma Capital, and Zero Knowledge Ventures. (Apr 23)

P:S If you’re often missing TC Daily in your inbox, check your Promotions folder and move any edition of TC Daily from “Promotions†to your “Main†or “Primary†folder and TC Daily will always come to you.

In the world of Kenyan elites, wristwatches are becoming the new real estate. Yes, instead of land plots, some of the crème de la crème are now putting money into pre-owned luxury watches, because apparently, you can wear your investment and flip it later for profit. What makes this wild is how much it makes sense. Unlike property, a watch doesn’t need permits or months to sell. It can be liquidated in days and carried across borders on your wrist.

If you were to invest in something unconventional, what would it be?

In other news, Nigeria’s elections have a retention problem. A new Zikoko Citizen report predicts what participation in the 2027 election might look like, drawing on trends from previous cycles, and explores what could bring about a massive turnaround.

Nigeria’s consumer protection watchdog approves five airtime lenders

Image source: The Punch

After Nigeria’s largest telecom operators MTN and Airtel temporarily suspended airtime lending last week, new players have swooped in to take their place—at least temporarily.

On Wednesday, the Federal Competition and Consumer Protection Commission (FCCPC), Nigeria’s consumer protection watchdog, approved five companies to operate airtime and data lending services: Total TIM Nigeria Limited, Rane Interactive Medien CLS Limited, Mode NG Applications Nigeria Limited, Cloud Interactive Associate Limited, and Coverage Broadband Limited.

The move comes as Globacom and T2, which round up the four telcos operating in Nigeria, have also quietly paused their own lending services, according to our checks.

Will telcos resume airtime lending? Airtime lending has not been scrapped; it is being reorganised. Under the FCCPC’s 2025 regulations, services like MTN’s Xtratime are now classified as consumer credit, requiring proper licencing, disclosure of fees, and clearer accountability.

For users, the immediate question is what happens to existing debt. Telecom operators haven’t addressed this yet.

There is another wrinkle. The newly approved lenders, it is worth noting, do not yet have listed consumer-facing apps in the FCCPC’s disclosure, making it unclear how Nigerians can actually access these services for now.

Between the lines: This is opening the door to new competition. Telcos have long dominated airtime credit, but once they secure approval and return, they may find themselves sharing that space with licenced third-party lenders operating under stricter rules.

What is really happening? Airtime credit is being pulled into the formal lending system, where the business is clearer, and the players are easier to hold accountable.

20+ Markets. One API.

Fincra connects your business to Africa’s payment rails without building market by market. For collection, payout, FX, and settlement through a single integration. See what this means for your business.

companies

M-Tiba is shutting down its health savings wallet

Image Source: M-Tiba

A curious little back story: In 2025, a cyberattack hit M-Tiba, a Kenyan healthtech platform, and went undetected for ten days. That attack exposed the personal and medical information of nearly five million Kenyans, including insurance claims, patient information, and clinical records.

What’s the news here? The same platform is now shutting down its My Health Funds (MHF) wallet, the feature that allowed people to set aside money strictly for healthcare. M-Tiba users have begun receiving refunds of the amount in the wallet into their M-PESA accounts without requesting withdrawals.

There is no confirmed link between the breach and the decision to shut down the wallet, but the timing raises eyebrows. Plus, the explanation that CarePay Limited, M-Tiba’s operator, gave is… thin. The official line is that it is evolving and will now shift its focus to “improving health insurance management.â€Â

Beyond that, there is very little detail on why the wallet is being retired, how many users were affected, no clarity on how affected users transition, and no real sense of what this new focus will look like. Will this mean deeper partnerships with insurers? A new insurance-led product? Or a full pivot away from individual users entirely? For now, it seems like a product shutdown wrapped in a vague strategy shift.Â

While one can make guesses about what might be happening behind the scenes, this is one of those moments where CarePay needs to spill a bit more tea.

TECHCABAL 4.0

In March 2013, TechCabal published its first article. Thousands of stories later, the work continues, and today, it goes deeper.

TechCabal has always been free. That’s not changing.

We’ve opened a new layer. Reporting that goes further, built on sources you won’t find anywhere else, and told in ways we haven’t tried before. You’re among the first to see it.

Getting in takes less than 15 seconds.

You’re one step away from the other side.

Click the button below to see what TechCabal 4.0 looks like and what it means for you.

Absa Kenya is spending $23.2 million on digital banking

Absa Kenya headquarters in Nairobi. Image source: Absa

Across Africa, walking into a bank branch is becoming a backup plan, as digital payments deepen. Absa Kenya, the country’s seventh-largest bank by assets, is leaning fully into that shift. The lender says it plans to spend up to KES 3 billion ($23.2 million) annually on technology as it pushes more customers toward mobile and self-service banking.

The investment is not new, but it is becoming routine. Absa spent KES 2.16 billion ($16.7 million) on technology in 2025, and now treats digital spend as a recurring cost of staying competitive. The payoff is already visible: 94% of all transactions now happen outside branches, a sharp jump from roughly 40–50% a decade ago.

This is less about innovation and more about survival. Kenya’s banking sector has long been shaped by mobile money, and customer expectations now revolve around speed, convenience, and always-on access. Traditional banks are adjusting or risking irrelevance.

What is really happening? Absa is rebuilding its retail strategy around digital channels, and leadership changes reflect that shift. The appointment of former M-Pesa Africa chief executive Sitoyo Lopokoiyit to lead personal and private banking signals where future growth is expected to come from.

The efficiency gains are starting to show. The bank’s cost-to-income ratio improved to 36.5% in 2025 from 46% a year earlier, while operating expenses dropped 21% to KES 7.35 billion ($56.9 million). At the same time, net profit rose 10% to KES 22.9 billion ($177.3 million), suggesting the digital push is not just about convenience, but also margins.

Zoom out: Kenyan banks are no longer just competing with each other. They are competing with the habits shaped by mobile money, where transactions are instant and physical branches are optional. Absa’s spending signals that keeping up now comes with a permanent technology bill.

All the technical ways to describe a cool car: The Chery Q comes with a 42.7kWh battery, up to 400km range, a peak power output of 90kW, a rear-mounted motor, and a cabin that leans heavily into screens and software, including a 15.6-inch infotainment display and a 360-degree panoramic camera.

The EV market is getting busy: South Africa’s new energy vehicles (NEV) growth was valued at R244 million ($14.3 million) in 2024, with about 3,800 units sold, as reported by Forbes Africa.

Competition in this sector is already there from Chinese automakers like BYD and Geely— which recently made its local debut at a starting price of R339,900 ($20,600). Though Chery claims some of the features of the Q car trumps those of the competitor (peak power output), its edge is that it has already built its reputation locally with its non-EV models.Â

A familiar name with a heavy past: If the Chery Q sounds familiar, it should. This is a modern reboot of the QQ3, one of the cheapest cars South Africa had seen when it first arrived in 2008. It was cheap, only going for R59,900 ($3,600) at the time.Â

However, these cars received a zero-star safety rating in a South African car safety campaign conducted by the Global New Car Assessment Programme (NCAP). While this new version has history, the Chery Q is now getting a second chance to meet a higher safety and car quality expectation.

CRYPTO TRACKER

The World Wide Web3

Source:

Coin Name

Current Value

Day

Month

Bitcoin

$77,800

– 0.62%

+ 10.90%

Ether

$2,343

– 2.30%

+ 10.01%

XRP

$1.41

– 2.92%

+ 0.35%

Solana

$85.84

– 2.65%

– 4.73%

* Data as of 06.34 AM WAT, April 23, 2026.

Events

The voices shaping Africa’s digital future are taking the stage. From AI and IoT to cloud, connectivity and smart infrastructure, IOT West Africa | Data Centre & Cloud Expo Africa 2026 brings together the leaders building the continent’s next digital chapter. This is where the ecosystem meets, and we’ll see you there. The event kicks off on April 28–30 at the Landmark Centre, Victoria Island, Lagos. Register here to attend.

All roads lead to Nairobi on May 7, 2026. Gathered at the Sarit Expo Centre, senior leaders from across Africa’s fintech and payments ecosystem will gather for a day of meaningful connections, market insights, and cross-border collaboration. The focus of the Africa Fintech Live event is on driving real engagement, bringing together industry leaders and emerging innovators to spark strategic conversations that will shape the future of finance on the continent. Secure your early bird ticket now at 50% off

On May 6–8, 2026, policy, capital, and innovation in Africa will take centre stage at the 3i Africa Summit. Happening at the Destiny Arena, Accra, Ghana, it will pack operators, investors, and policymakers in one room to answer questions about the continent’s integrated fintech future, and what it’s still missing. Register here to attend.

The Africa Tech Summit London 2026 is back for its 10th edition. Held at the London Stock Exchange building in London on May 29, it will feature 350 attendees from over 200 companies, the event will be a small, high-impact gathering of founders, investors, and global partners driving the future of tech in Africa. Use the code TC10 to get 10% off tickets. Apply to attend.

P:S If you’re often missing TC Daily in your inbox, check your Promotions folder and move any edition of TC Daily from “Promotions†to your “Main†or “Primary†folder and TC Daily will always come to you.

Absa Bank Kenya will spend up to KES 3 billion ($23.2 million) a year on technology to deepen its digital strategy, according to a Business Daily report, as the lender seeks to move more customer activity to mobile and other self-service channels.

The bank said the recurring investment will make transactions easier and support its push into digital banking, even as competition intensifies and customer expectations shift away from branches.

The change reflects a broader migration across Kenya’s banking sector towards mobile and self-service channels, a trend accelerated by the country’s entrenched mobile money ecosystem and rising expectations for instant, always-on financial services.

“Typically, we now do KES 2 billion ($15.4 million) to KES 3 billion ($23.2 million) of investments per year [in technology], and 2025 was no different in ensuring we are migrating transactions to digital platforms. We are making it easier for our customers to transact with us,†Absa Kenya chief executive Abdi Mohamed told Business Daily.

The bank spent KES 2.16 billion ($16.7 million) on technology in 2025, underscoring how quickly digital investment has become a fixed cost in its operations. About 94% of all transactions in 2025 took place outside branches, compared with roughly 40–50% a decade ago, according to the lender.

The technology push comes as Absa continues to reshape parts of its consumer banking leadership around digital banking. In February, the bank appointed former M-Pesa Africa chief executive Sitoyo Lopokoiyit to head its personal and private banking division, a move widely read as a signal of where it expects retail growth to come from.

Lopokoiyit, who built his reputation overseeing the expansion of M-Pesa, is expected to bring mobile banking experience to retail and affluent banking at a time when the boundaries between banks and fintechs are becoming blurred.

Efficiency gains

The efficiency gains are already visible in the bank’s cost base. Other operating expenses fell 21% to KES 7.35 billion ($56.9 million) in the year to December 2025, with management attributing much of the decline to digitisation and automation. The impact of the technology push has also been reflected in performance metrics.

Absa’s cost-to-income ratio—a measure of banking efficiency—improved to 36.5% in 2025 from 46% a year earlier, helped by lower costs and improved revenue generation.

Net profit rose 10% to KES 22.9 billion ($177.3 million) over the period, suggesting that efficiency gains from digitisation are beginning to support bottom-line growth, even as investment spending remains elevated.

Introducing… WhatsApp Premium (because money must be made).

You read that right. WhatsApp is testing paid subscriptions that unlock features like more pinned chats, custom app icons, themed interfaces, and exclusive ringtones and stickers. Fun, but we’ll see how that plays out.

South Africa’s communication regulator, the Independent Communications Authority of South Africa (ICASA), is also side-eyeing the platform and other over-the-top (OTT) services like Netflix. The focus is to open a market inquiry into whether these services are eating into the space that traditional broadcasters once dominated, and what that means for competition and regulation. Findings are expected after the 2026/2027 financial year.

Fingers crossed for whatever ICASA finds.

In other news, Nigeria’s elections have a retention problem. A new Zikoko Citizen report predicts what participation in the 2027 election might look like, drawing on trends from previous cycles, and explores what could bring about a massive turnaround.

Nigeria’s Central Bank and telecoms regulator team up to give banks real-time access to telecom data

Aminu Maida, the EVC of Nigerian Communications Commission (Middle) and Cardoso Olayemi, the Governor the Central Bank (Right) of Nigeria during the signing of the MoU. Image source: NCC

Financial fraud in Nigeria has gone beyond stealing passwords or tricking people into sending over sensitive financial information. SIM cards are now identity anchors used in financial services; recycled or swapped phone numbers have become a sort of back door for fraudsters to intercept one-time passwords (OTPs) and move money before anyone notices. The impact is ₦52.26 billion ($37.86 million) in losses in 2024.

Now, the Central Bank of Nigeria (CBN) and the Nigerian Communications Commission (NCC), the country’s telecoms regulator, have signed a new agreement that would allow banks to check mobile number activity before a transaction goes through.

How would it work? At the centre of this partnership is something called the Telecom Identity Risk Management System (TIRMS), a centralised platform designed to track and verify the risk status of mobile numbers. With this new setup, banks can see what’s going on behind a phone number in real-time: whether it has been recently altered, reassigned, flagged for suspicious activity, or is inactive. It’s like sharing intelligence.

What does peeking into this data do? With real-time verification, banks can flag risky transactions before they happen. It will increase scrutiny on phone numbers that show signs of compromise in the system. This could mean that banks can pause authentication steps or transactions tied to those phone numbers before money is transferred.Â

Will this reduce fraud? Though this additional data will close a huge gap for banks, it is not a standalone fix. It will likely make it harder for attackers to exploit one of the most common entry points, and frankly, easy-to-obtain methods of identity farming, which are mobile numbers.Â

However, the extent of regulatory oversight is still unknown. It is unclear whether banks, for example, will have autonomy to report compromised phone numbers to law enforcement agencies, or how they will handle such cases.

This matters because fraud cases succeed when systems are disconnected. This collaboration could reduce fraud vulnerabilities.

20+ Markets. One API.

Fincra connects your business to Africa’s payment rails without building market by market. For collection, payout, FX, and settlement through a single integration. See what this means for your business.

Cryptocurrency

Kenya freezes accounts of Binance users

Image Source: Zikoko Memes

POV: you’re a Binance user in Kenya, and you wake up to check if your trades are up or down, or maybe even cash out. But suddenly, you can’t access your account or move anything.

It’s not a glitch: Kenya’s Directorate of Criminal Investigations (DCI), an investigative agency, has moved to freeze an undisclosed number of Binance accounts, in a crackdown on crypto-linked fraud, money laundering, and suspected terrorism financing. Binance has told affected users that the restrictions came at the request of authorities.

Crypto must conform: Kenya is under pressure to tighten its financial controls and exit the Financial Action Task Force (FATF) grey list, following Nigeria and South Africa’s exits in October 2025. This list flags countries with gaps in anti-money laundering controls, including crypto.Â

The Virtual Asset Service Providers (VASP) Act, passed in 2025, will regulate virtual asset businesses in the country by bringing exchanges and intermediaries under formal oversight. Freezes on accounts such as this seem like early enforcement; authorities acting on suspected risks even as the full regulatory framework is still being operationalised.Â

What happens to the frozen accounts? That really depends on what investigators find. Once an account is flagged on such suspicions, it stays restricted while investigations are ongoing.Â

Authorities may request transaction histories, identity verification, and links to other flagged accounts to determine whether the funds are tied to illicit activity. Access to their accounts can be restored if they are cleared. Otherwise, their funds could remain frozen for a longer time or be subject to forfeiture under anti-money laundering laws.

20+ Markets. One API.

Breet is offering a $10,000 equity-free grant to growth-stage fintech, crypto and payments startups in Africa. Integrate the API, submit your product, and pitch live at ATE Lagos. Two winners get $5,000 each. Deadline by May 31. Learn more.

Regulation

South Africa takes aim at Netflix and WhatsApp as TV money dries up

Image Source: Zikoko Memes

South Africans are watching less traditional TV and spending more time on Netflix and WhatsApp, and the regulator is starting to ask whether that balance is fair.Â

The Independent Communications Authority of South Africa (ICASA), the telecoms and ICT regulator, now plans to investigate how over-the-top (OTT) platforms, like streaming and messaging services, are affecting broadcasting revenue, just as the country’s pay-TV market slipped below 7 million subscribers for the first time in five years.

The regulator says services like Netflix, YouTube, and WhatsApp are no longer simple “alternatives†to television, but direct competitors for both audiences and advertising income. Its upcoming market inquiry will look at whether this shift is weakening the financial base of licenced broadcasters. While we smell a fish behind this plan, we still wonder what will come out of this. If OTT streaming platforms like Netflix are, indeed, found guilty, what’s a realistic way to ensure market control or fairness?

Between the lines: This is where the debate turns uncomfortable for traditional media. Pay-TV operators argue that while they carry regulatory obligations, global platforms operate in South Africa without the same rules, yet still pull away viewers and ad spend. Competitive tension is now being packaged under “fair share†discussions.

What is really happening? Telecom operators in South Africa, through the industry body Association of Comms and Technology (ACT), want streaming and messaging platforms to contribute to network costs, arguing that services like Netflix and WhatsApp only work because broadband infrastructure exists in the first place. ICASA will weigh this against broader policy changes already being drafted by the government, including possible content quotas and tax reviews for global streaming platforms.

Zoom out: The timing matters. Traditional broadcasting is shrinking, streaming is growing, and messaging apps have become a default communication layer. ICASA is stepping into a market where old revenue models are already under pressure, and trying to decide who should pay for the infrastructure behind it all, and how much.

TECHCABAL 4.0

In March 2013, TechCabal published its first article. Thousands of stories later, the work continues, and today, it goes deeper.

TechCabal has always been free. That’s not changing.

We’ve opened a new layer. Reporting that goes further, built on sources you won’t find anywhere else, and told in ways we haven’t tried before. You’re among the first to see it.

Getting in takes less than 15 seconds.

You’re one step away from the other side.

Click the button below to see what TechCabal 4.0 looks like and what it means for you.

South African carmakers sold a record 664 plug-in hybrid electric cars in March

Image Source: Tenor

South Africans are slowly realising that petrol stations are not the only place to fill up anymore, and plug-in hybrids are starting to reflect that shift in a way that is finally showing up in the numbers.

March marked a record month for plug-in hybrid electric vehicle (PHEV) sales in the country, with 664 units sold, according to the National Association of Automobile Manufacturers of South Africa (Naamsa), the industry group for carmakers.

Why it matters: It is a 130% jump from February and comfortably above the previous record set in September 2025. In Q1 2026, South African carmakers sold over 1,200 PHEVs, already outpacing Q1 2025 levels, and pointing to a market that is picking up speed rather than drifting. The uptake also comes amid petrol price hikes in South Africa, where it increased by 20 cents per litre in March. Another planned petrol hike is already underway in April.

Between the lines: This is not happening in a vacuum. The fuel price pressure and a wave of more affordable Chinese models are doing most of the heavy lifting. Until recently, plug-in hybrids were firmly in the luxury bracket. Now, several options are landing between R500,000 and R1 million, pulling them closer to mainstream buyers.

What is really happening? BYD, the Chinese EV manufacturer, is leading the charge, followed closely by Chery and its sister brands Omoda and Jaecoo. BMW, Volvo, and a handful of legacy automakers are still present, but the centre of gravity is clearly shifting toward Chinese manufacturers offering cheaper, feature-heavy alternatives.

Zoom out: PHEVs sit in a strange middle ground. They are not fully electric, but they offer enough electric driving range to meaningfully cut fuel use for typical daily commutes. In a country where most drivers cover under 50km a day, that hybrid flexibility is starting to feel less like a compromise and more like a practical option.

CRYPTO TRACKER

The World Wide Web3

Source:

Coin Name

Current Value

Day

Month

Bitcoin

$78,043

+ 2.90%

+ 13.83%

Ether

$2,389

+ 3.04%

+ 15.53%

OpenGradient

$0.3773

+ 97.10%

+ 97.10%

Solana

$87.87

+ 2.74%

+ 1.12%

* Data as of 06.30 AM WAT, April 22, 2026.

Opportunities

Applications are open for ClimateLaunchpad, the world’s largest green business ideas competition run by Climate-KIC. The programme helps early-stage climate founders turn rough ideas into viable startups through training, mentorship, and pitch competitions. Entrepreneurs from around the world, including Africa, can apply for the 2026 cohort and compete for up to €10,000 in prize money and access to a global cleantech network. Apply here.

Google for Startups: Africa, a three-month hybrid accelerator for growth-stage startups on the continent, is now accepting applications. The accelerator will provides equity-free support for the duration of the programme, mentorship, training, cloud credits, and access to Google’s AI products designed to bring the best of its programmes, products, people, and technology to communities across Africa. Apply here.

Google and UpSkill Universe have partnered to relaunch Hustle Academy, now offering free AI and business training to individuals and small businesses across Africa. The programme features 60-minute expert-led webinars and 1-day bootcamps (3–5 hours), covering digital marketing, e-commerce, business strategy, financial management, and AI tools. Open to students, jobseekers, entrepreneurs, and past applicants, it provides practical, hands-on skills that can be immediately applied to grow careers or businesses. Apply here.

P:S If you’re often missing TC Daily in your inbox, check your Promotions folder and move any edition of TC Daily from “Promotions†to your “Main†or “Primary†folder and TC Daily will always come to you.

The Communications Authority of Kenya (CA) has announced its decision to revoke the licenses of 42 television stations. Citing a persistent failure to comply with regulatory requirements, the move signals a continued effort by the CA to enforce the provisions of the Kenya Information and Communications Act (Cap. 411).

The stations have been given a seven-day notice to cease operations, with all broadcast resources reverting to the Authority. It is not clear when the licences will be revoked, because the statement was issued on August 22, but gazetted on September 12. So far, most of the TV stations listed are still in operation.

The revocation, announced by CA Director-General David Mugonyi, is the latest in a series of actions aimed at sanitising the broadcasting sector. This follows a similar crackdown in 2024, when the Authority revoked the licenses of 75 TV and radio stations.

The current list of affected broadcasters includes well-known outlets such as Mount Kenya TV, owned by politician Purity Ngirici and her husband; NAI TV, owned by renown media personality Jimmi Gathu; Wananchi TV, owned by Wananchi Group, which also owns ISP Zuku; Fanaka TV, owned by politician and former cabinet secretary Moses Kuria, and Metropol TV, owned by the parent company that also owns credit reference bureau Metropol.

According to a statement from the CA, the reasons for the revocations are wide-ranging but centre on critical regulatory breaches. These include the failure to pay license fees, non-compliance with licensing conditions, and in some cases, a complete cessation of operations. The Authority maintains that these measures are essential to uphold broadcasting standards and ensure a fair and transparent media environment.

The directive has raised concerns about the future of many smaller and independent media houses. For the affected stations, the immediate implication is a total shutdown of their operations, rendering them unable to broadcast or provide any services. For Zuku in particular, this will curtail one of their critical value-add services.

While the affected stations have the option to appeal, the CA’s stance indicates that the path to reinstatement will be challenging. This action underscores the CA’s commitment to holding all broadcasters accountable, regardless of their size or reach.

Here is the full list of affected stations:

Apple Truth Television owned by Apple Truth Television Network Limited Metropol TV owned by Comprehensive Business Media Limited Corporate Media TV owned by Corporate Media Communications DG TV owned by Dominion Generation Limited Doxa TV owned by Doxa Television Dunamis KTV owned by Dunamis Television Network Limited Masai TV owned by Enaang Maa TV Limited Ezra Christian TV owned by Ezra Christian TV Limited Fanaka TV owned by Fanaka Television Limited Faith Estate TV owned by Fort Hall College Limited Talent TV owned by Gates Africa Education Trust Champion TV owned by Heroes Communications Limited ILM TV owned by ILM Media Limited NAI TV owned by JimmiGathu Incorporated Limited The Mirror Television owned by Jmax Media Services Limited Ziwa TV owned by Jusga Wanjira Construction Limited Kingdom Ambassadors TV owned by Kingdom Ambassadors Media Group Limited Uboro TV owned by Kirinyaga Multimedia College Kokwo Television owned by Kokwo Radio International Limited Bulsho TV owned by Lufman Company Limited Manifestation TV owned by Manifestation TV Limited Mount Kenya TV owned by Mount Kenya Media Limited Limited Pillar TV owned by Mt. Kenya Blessings Company Tourism and Wildlife TV (Safari Channel) owned by Next Options Limited

Ongatet owned by Ongatet Television Network Mbugi TV owned by Outcom Media Limited Safina Television owned by Safina T.V Limited Shakaal Television owned by Shakaal Media Network Limited Sugan TV owned by Sugan Media Group Tama TV owned by Tama Media Group Limited Sawa Television owned by Tano Entertainment Network The Word Music TV owned by The Word Music Limited Soko TV owned by Thirties Media Limited Thjiwe TV owned by Thstone Television Limited Tem TV owned by Triple Edge Media Limited Ukweli TV Kenya owned by Ukweli Sounds and Video Limited Value TV owned by Valutel Limited Wananchi TV owned by Wananchi Television Network Limited 009 TV owned by 009 Television Limited Ability TV owned by Ability Channel Limited Ace TV owned by Ace Television Limited Superflex Television owned by Admerline Construction Limited

The money had just hit Sylvia Wanjiru’s account when her phone rang. It was a million-shilling ($7,773) payment from a client, and the caller claimed to be from her bank’s customer service. He spoke confidently, offering to “help confirm the transaction.â€

“At first I thought it was just a coincidence,†Wanjiru recalls. But when the same thing happened again, she realised someone was watching her transactions and reported it to the bank.

Her parents were not so fortunate. Pension payments of KES 34,000 ($263) and KES 2,500 ($19) from a mobile money wallet disappeared after they called a number that texted: “*** BANK. Dear Customer, your account has been SUSPENDED. Please contact 010****366 within 24 hours.â€Â Â

The money was long gone by the time they rushed to the bank and mobile money provider. Wanjiru’s experience is one among many others. Across Kenya, customers report similar encounters, including calls moments after cash deposits or transfers and text messages disguised as official alerts followed by withdrawals.

The speed and timing point to a possibility that the fraudsters work hand in glove with bank staff and mobile money agents with access to customer information.

Rising cyber-threats

The Central Bank of Kenya (CBK), in its Financial Sector Stability Report 2025, in August reports cases of cyber fraud in the banking sector more than doubled in 2024, rising from 153 to 353, with the amount exposed increasing to KES 1.9 billion ($14.7 million) and losses nearly quadrupling to KES 1.5 billion ($11.6 million).

The Communications Authority of Kenya (CA) reported 7.9 billion cyber threats in the first eight months of 2025, double the figure for 2024. CBK said attacks rose from 7.7 million in 2016 to billions due to Kenya’s economy’s rapid digitisation.

The regulator insists that despite rising risks, Kenya’s banking sector remains “resilient,†able to withstand shocks from successful cyber-attacks. However, accounts from victims, bank staff, and law enforcement suggest that most losses of funds are inside jobs.

A former compliance officer described a shadow industry in Nairobi neighbourhoods like Utawala and Ruiru, which thrives on mobile banking fraud. The setups look like call centre outsourcing hubs with rows of desks, computers, and phones.

“There are bank staff who monitor accounts, tip off the fraudsters, and within minutes, money is pushed into mule accounts,†says one ex-risk and compliance at a major bank. The cash is laundered through mobile money wallets and withdrawn at agents, or some are pushed to crypto wallets.

With 67% youth unemployment, workers are recruited through job ads for “customer service†roles, only to discover that the scripts involve impersonating bank officials or mobile money agents. And because it’s quick cash, many stay.

Pay is per successful hit, which means the more money they steal from customers, the more they earn. Corrupt police officers, according to the former compliance officer, are paid to protect operations, tip off the syndicates before raids, or frustrate investigations.

“It’s a big operation, more than you can imagine,†the former officer says. “The real people behind these schemes are known to some in Kenya Police’s serious crimes division.â€

Targets the biggest banks

The people behind the schemes design them for scale, according to an investigations officer at Banking Fraud Investigations Unit (BFIU)—a unit under the Directorate of Criminal Investigations (DCI)—who has handled such cases and asked not to be named. They target banks with vast retail business like Equity Bank, KCB Group, and Co-operative Bank— Kenya’s biggest retail lenders with a combined customer base of over 50 million. With such big operations, the fraudsters hide in the noise of millions of daily transactions.

Rural pensioners, urban traders, and salaried workers with predictable income streams make easy prey.

“It’s a numbers game,†says the BFIU officer. “The bigger the bank, the more likely someone will slip.â€

Most of these frauds are not violent, but sometimes they turn deadly. In April, a teacher in Mumias was trailed and killed after withdrawing KES 285,000 ($206). Detectives believe two bank tellers may have passed on the information to robbers, pointing to insider collusion with criminals.

There are numerous reports of customers being trailed after withdrawing or depositing large sums at banks and mobile money agents across the country.

In 2024, Equity Bank reported it lost KES 1.5 billion ($11.6 million) in what was initially described by news outlets as a sophisticated hacking attack. However, investigators later alleged that bank staff colluded with property developers and lawyers to siphon off the bank’s money from the salary suspense account in thousands of small, salary-like transfers to avoid detection.

Deeper rot

On social media, many Kenyans brush off mobile banking fraud as the work of prisoners with smuggled phones when they are operations run by people living among them. While some operations enjoy corrupt officials’ backing, the BFIU officer concedes that the regulators are overstretched.

“Mobile money and banks process millions of payments daily, and that’s why some of the cases even go unnoticed,†says the officer.

However, faced with mounting fraud, most Kenyan banks have begun housecleaning to restore customer confidence. KCB Group, NCBA, Absa, and Co-operative Bank are some lenders that have recently fired staff over misconduct.

In May, Equity Group took a bolder step, announcing publicly that it was firing 1,500 staff to protect the bank’s image and its customers.

“The moment of reckoning has come,†Equity Bank CEO James Mwangi said in May. “It doesn’t matter how many I will lose. I don’t even care. I will protect the customers and the bank. I will be ruthless.â€

The bank has since extended the exercise to its subsidiary in Uganda, which has also suffered staff-linked fraud in the past two years.

Blurring of lines

The lines between cyber fraud, insider theft, and organised crime are blurred. According to the BFIU officer, most victims never report, whether from embarrassment, the small sums involved, or the hassle of filing a complaint with the police, making the CBK’s figure of KES1.5 billion an understatement.

The BFIU investigator says the schemes rarely fall into specific categories. A phishing text may be the start, but a bank teller can pass on stolen data, laundered through mobile money, and protected by police officers. Each stage blurs the line between cyber-attacks, insider theft, and organised racketeering.

The consequence, the former compliance officer warns, is erosion of trust. Many customers, unsure whether the fraudsters are hackers or someone inside their bank, choose not to report. Anxious to reassure shareholders and depositors, lenders frame the losses as “cyber threats†even when investigations show human hands.

This gap between the official narrative and what victims experience is where the danger lies. The BFUI investigator says that as Kenya’s financial system grows, the weakest link may be the people inside—tellers, agents, and officers with access to real-time customer records. Â

Mark your calendars! Moonshot by TechCabal is back in Lagos on October 15–16! Meet and learn from Africa’s top founders, creatives & tech leaders for 2 days of keynotes, mixers & future-forward ideas. Get your tickets now: moonshot.techcabal.com

with Kolawole Bekes

with Kolawole Bekes

The voices shaping Africa’s digital future are taking the stage. From AI and IoT to cloud, connectivity and smart infrastructure, IOT West Africa | Data Centre & Cloud Expo Africa 2026 brings together the leaders building the continent’s next digital chapter. This is where the ecosystem meets, and we’ll see you there. The event kicks off on April 28–30 at the Landmark Centre, Victoria Island, Lagos.

The voices shaping Africa’s digital future are taking the stage. From AI and IoT to cloud, connectivity and smart infrastructure, IOT West Africa | Data Centre & Cloud Expo Africa 2026 brings together the leaders building the continent’s next digital chapter. This is where the ecosystem meets, and we’ll see you there. The event kicks off on April 28–30 at the Landmark Centre, Victoria Island, Lagos.