What do you think of when you hear “financial inclusionâ€, access to bank accounts? It’s more than that! Financial inclusion involves all-around financial services for everyone; however, over 1.3 billion adults worldwide remain unbanked, predominantly in emerging markets across Sub-Saharan Africa, South Asia, and parts of Latin America.? Emerging technologies, particularly Artificial Intelligence (AI) and...

The post Fintech Innovation: The R

What do you think of when you hear “financial inclusionâ€, access to bank accounts? It’s more than that! Financial inclusion involves all-around financial services for everyone; however, over 1.3 billion adults worldwide remain unbanked, predominantly in emerging markets across Sub-Saharan Africa, South Asia, and parts of Latin America.? Emerging technologies, particularly Artificial Intelligence (AI) and...

Cape Town venture capital firm HAVAÃC has secured USD 25 M toward its USD 50 M African Innovation Fund 3, with major backing from financial services group Sanlam Multi-Manager. The fund targets 15 early-stage African tech startups with global potential, focusing on fintech, agritech and other high-growth sectors.

The investment marks Sanlam’s first significant move into South Africa’s VC space, joining existing backers Fireball Capital and the

Cape Town venture capital firm HAVAÃC has secured USD 25 M toward its USD 50 M African Innovation Fund 3, with major backing from financial services group Sanlam Multi-Manager. The fund targets 15 early-stage African tech startups with global potential, focusing on fintech, agritech and other high-growth sectors.

The investment marks Sanlam’s first significant move into South Africa’s VC space, joining existing backers Fireball Capital and the SA SME Fund. HAVAÃC has already deployed capital from the fund, including USD 1 M investments in SAPay (digitising taxi payments) and sports analytics platform Sportable. These join earlier 2025 investments in pan-African payments platform NjiaPay and livestock trading platform SwiftVEE.

The announcement follows several successful exits from HAVAÃC’s portfolio, most notably emergency response tech firm RapidDeploy’s acquisition by Motorola Solutions; one of South Africa’s largest tech exits. Another portfolio company, hearX Group, recently merged with hearing tech firm Eargo in a USD 100 M deal.

With its current portfolio already serving 22 million customers across 183 countries, HAVAÃC is positioning itself as a key player in Africa’s growing VC landscape. The firm plans to continue identifying and supporting African tech entrepreneurs building scalable solutions, with particular interest in businesses that can expand across multiple African markets and beyond. The remaining USD 25 M of the fund is expected to be raised in the coming months.

Nigeria’s bubbly fintech sector is under fresh scrutiny after the country’s anti-corruption agency uncovered a sprawling identity fraud scheme involving thousands of young Nigerians selling biometric data to digital finance platforms.

According to the Economic and Financial Crimes Commission (EFCC), over 12,000 individuals are allegedly harvesting and reselling critical identity information—including Bank Verification Numbers (BVNs) and N

Nigeria’s bubbly fintech sector is under fresh scrutiny after the country’s anti-corruption agency uncovered a sprawling identity fraud scheme involving thousands of young Nigerians selling biometric data to digital finance platforms.

According to the Economic and Financial Crimes Commission (EFCC), over 12,000 individuals are allegedly harvesting and reselling critical identity information—including Bank Verification Numbers (BVNs) and National Identification Numbers (NINs)—to fintech companies for as little as NGN 5 K (~USD 3.33) per identity.

The illicit trade, described by the EFCC as a “threat to national security,†exposes a troubling weakness in the Know Your Customer (KYC) processes meant to secure Nigeria’s digital financial systems.

In some cases, scammers reportedly pay victims between NGN 1.5 K and NGN 2 K to surrender personal data, including ID photos, address details, and national ID slips. These details are then used to open accounts linked to fraudulent investment schemes, or to launder money via cryptocurrency and microfinance channels.

The alleged fraudsters, often referred to as “Account Suppliers†or “KYC Groups,†have created a black market for verified identities, exploiting the very infrastructure designed to enhance trust and access in the country’s digital economy.

While the EFCC did not publicly name the fintech companies implicated in the ongoing investigation, it confirmed that arrests have been made and that recovery efforts are underway.

The fallout has also reached Nigeria’s National Identity Management Commission (NIMC), which has moved to distance itself from the scandal. In a statement, NIMC’s spokesperson Kayode Adegoke denied institutional responsibility, stressing that the commission had repeatedly warned citizens against disclosing their NINs to unauthorised parties.

“The NIMC will not be held responsible for any personal information shared by an individual directly or by proxy for the purpose of financial gain,†the statement read. The agency encouraged the public to use its NINAuth mobile app to better control and protect their identity data.

Beyond the data-selling racket, the EFCC also flagged a parallel scheme involving malware and phishing. In one instance, victims were lured by a fake airline promo offering 50% off tickets in exchange for a NGN 500.00 “charity†donation. The scam prompted users to download a counterfeit app embedded with spyware capable of siphoning sensitive banking credentials.

Once accessed, victims’ funds were funneled into accounts, often opened with stolen identities, then converted to crypto to obscure the trail.

The revelations cast a shadow over Nigeria’s fintech boom, which has attracted billions in venture capital and positioned itself as a beacon of innovation and financial inclusion on the continent. The EFCC’s findings now raise urgent questions about compliance lapses and data protection standards in the sector.

It’s safe to say Multichoice Nigeria’s legal team isn’t having a good morning as they grapple with a hefty ₦766 million (500,000) fine from the Nigeria Data Protection Commission (NDPC) for violating the Nigeria Data Protection Act (NDP Act).

On a different note, how’s your second half of the year going? If you’re Gen Z, odds are you’re venting on TikTok about low pay, zero flexibility, and office drama. Owl Labs’ 2024 report says 43% of workers are more stressed than last year and 89% see no improvement in their work-related stress. The grind isn’t getting easier. How’s work treating you?

PS: If you’re curious about the tech ecosystem in Francophone Africa, sign up for our latest newsletter, TNW: Francophone Africa. We’ll bring the biggest insider insights and analysis of the region’s technology landscape bi-monthly. Sign up here and be the first to know.

Nigerians can now swipe their naira card globally again

Image Source: Zikoko Memes

After three years, Nigerian banks have finally opened the gates for naira debit cards to roam globally again. That means you can now pay for your Apple Music, Amazon orders, or even that random item on AliExpress with the same card you use for Jumia.

United Bank for Africa (UBA) and Wema Bank are leading the comeback, confirming that their Premium Naira Cards and Naira Mastercards are once again enabled for international transactions—online transactions, POS machines, and ATMs abroad.

Why was there even a restriction? The year was 2022 and the survival of key sectors in the Nigerian economy were under threat. Foreign exchange was scarce, oil revenues were shaky, and Nigeria’s Central Bank’s managed exchange rate wasn’t helping. Eventually, financial institutions pulled the plug on global naira transactions. To keep their playlists going, people turned to virtual dollar cards from fintechs like Chipper Cash, Eversend, Cardtonic, and Payday.

What changed? It appears the confidence in Nigeria’s foreign exchange market is slowly creeping back to Nigeria’s Central Bank. The naira has shown signs of appreciation and diaspora remittances are now over $20 billion.

This is a curveball for virtual card providers. When banks locked international payments, startups like Chipper Cash, Eversend, Cardtonic, and Payday, stepped in with dollar cards. But now? These companies will have to step it up: offer better rates, more flexibility, or risk becoming irrelevant.

This is because not everyone will keep paying extra for what their naira card can now do natively. And in Nigeria’s fast-moving payment space, only the most adaptable will survive the next chapter.

Save more on every NGN transaction with Fincra

Stop overpaying for NGN payments. Fincra’s fees are more affordable than other payment platforms for collections & payouts. The bigger the transaction, the more you save. Create a free account in 3 minutes and start saving today.

Get the best African tech newsletters in your inbox

E-commerce

Takealot wants to hire 18,000 new workers from the ruins of the Post Office

Image Source: Zikoko Memes/TechCabal

18,000 workers who lost their jobs at South Africa’s Post Office, one of the country’s largest public employer, are about to get a new home.

Takealot is in talks to hire up to 18,000 retrenched workers from the South African Post Office, as part of a government-backed plan to repurpose state talent for private sector growth.

The plan, confirmed by the Department of Communications on July 3, is still under discussion. But the direction is clear: Takealot is ramping up its logistics workforce at scale ahead of a delivery war with the likes of new entrants Amazon, Shein, and Temu.

Why does it matter? Takealot is expanding aggressively to maintain its lead in South Africa’s e-commerce market. Amazon’s full local launch in 2024 changed the game. In response, Takealot has grown its revenue by 15%, offloaded non-core assets like Superbalist, and invested in AI tools, dark stores, and delivery operations. Now it’s looking at labour—skilled, available, and already trained in logistics basics.

This potential hiring wave reveals where Takealot’s focus is: building delivery muscle and shifting to an operations-heavy setup. Many of these former Post Office workers already know routing, package handling, and customer service. They also live close to the communities that Takealot wants to reach.

The online retail giant is also exploring township delivery programmes and driver development. It wants to build a national last-mile network that’s faster, more flexible, and harder for Amazon to replicate.

The state sees this as an opportunity to soften the blow of the Post Office collapse. Takealot sees a logistics edge and political capital. South Africa may get both jobs and an improved service delivery. A win for everyone involved.

Drive your business forward with Doroki

Whether you are a retail store, restaurant, pharmacy, supermarket, salon or spa, Doroki helps simplify your operations so you can focus on what matters most: your customers and your growth. Manage your business smarter, start here.

Internet

Egypt just landed two subsea cables with 126 TeraBits per second capacity

Subsea internet cables/Image Source: The Spectator

Telekom Egypt and SubCom just pulled off two key landings of the SEA-ME-WE-6 subsea cable system—one on the Mediterranean and the other on the Red Sea.

SEA-ME-WE-6: Southeast Asia-Middle East-Western Europe 6 (pretty cool, huh?)

Why does this matter? This isn’t just confusing wiring talk, and the SEA-ME-WE-6 isn’t just a shiny new pipeline. It is built to deliver a design capacity of 126 terabits per second, enough to handle millions of high resolution video calls all at the same time. Think faster internet connection, fewer network outages, and better protection against cable disruptions, like the seismic shock that hit West Africa in 2024.

For Egypt, it strengthens its role as a digital transit hub. The country already hosts 10 cable landing stations, supports 15 live subsea cables, and has five more under construction. But the SEA-ME-WE-6 puts Egypt back at the centre of the internet map. With growing demand for high-speed connections driven by cloud services, remote work, and digital trade, Egypt is well-positioned to monetise its geography.More global players will pay to move traffic through its routes, and more investors will look at Egypt’s internet economy seriously. With this, comes more economic power and digital influence for Egypt.

The signal is clear: Egypt isn’t just hosting internet traffic, it is routing the future. Soon, the world won’t just be connecting to Egypt, it will be connecting through it.

Accept in-person payments with Paystack Virtual Terminal!

Anyone can sell in-person. With Paystack Virtual Terminal, you can accept secure payments anywhere using just a QR code. No hardware needed.

Learn more here →

Get the best African tech newsletters in your inbox

Telecoms

NCC gives tower companies until August to improve internet quality or face fines

Image Source: TechCabal

Dear Nigerians, the next time your internet glitches midway through your Netflix binge or a Zoom call, the NCC wants you to know who is responsible.

In a sweeping change, the Nigerian Communications Commission (NCC), the regulator for telecom firms and internet service providers (ISPs), has said it will introduce a portal for tower companies to report downtimes on their network facilities. It has also given them an August deadline to improve their infrastructure or face fines.

Why does this matter? According to the NCC, Nigeria experiences an average of two network outages daily, with a total of 349 major outages recorded across the country between January and June 2025.

The NCC wants every company involved in the network connectivity value chain to be held accountable. When your internet connection frustrates you next time, it’s not enough to blame MTN, Airtel, Glo, or 9mobile. There are more players behind the scenes that make internet connectivity happen. Tower Companies (TowerCos) are one of them; they manage and maintain the cell towers you see in your streets, lease them to telecom companies, and charge for it. When their infrastructure fails, it affects you too.

Zoom out: Since the telecom tariff hike took effect in February, Nigerians have been paying more for internet, voice, and SMS services. Now the NCC is saying: if consumers must pay more, then service providers—especially TowerCos—must deliver more. And fast.

In September 2024, the telecom regulator reviewed its Quality of Service (QoS) benchmarks for mobile operators to improve internet quality and call drop rate. As part of that review, mobile operators now face a fine of ₦5 million ($3,300) if they fail to improve their service, and an additional ₦500,000 ($330) daily for the period the infraction lasts.

TowerCos too, like mobile operators, will get the same accountability treatment. No more excuses about diesel costs or unpaid bills from mobile operators. The Commission has made it clear: downtime has a deadline. And it expires in August.

Women, Apply to TC’s Battlefield Mentorship Programme.

If you’re a Nigerian woman in middle management with an ambitious idea and a passion to build, this is for you.

TechCabal Battlefield and Ventures Platform are offering a mentorship program to help you explore and build your first tech-enabled venture. You’ll get practical insights, honest conversations with founders and investors, and a 1-on-1 session with venture builders and ecosystem enablers.

Apply here→

CRYPTO TRACKER

The World Wide Web3

Source:

Coin Name

Current Value

Day

Month

Bitcoin

$109,191

+ 1.09%

+ 1.43%

Ether

$2,577

+ 2.59%

+ 3.59%

XRP

$2.27

+ 2.02%

+ 4.21%

Solana

$151.93

+ 3.11%

+ 1.37%

* Data as of 06.15 AM WAT, July 7, 2025.

Introducing, The Naira Life Conference by Zikoko

This August, the Naira Life Con will bring together wealth builders, entrepreneurs, financial leaders, and everyday Nigerians to share their experiences with earning, managing, and spending money. Think: bold conversations, immersive workshops, and content tracks that hand you a playbook for building real wealth. Get early bird tickets now at 30% off only for a limited time.

Opportunities

MEST Africa has opened applications for its 2026 AI Startup Programme. The 12-month training and incubation programme will equip West African software developers aged 21–30 with the skills to build scalable AI startups. Selected participants will undergo seven months of hands-on training in Ghana starting January 2026, followed by a four-month incubation for the most promising teams. Applications close August 22, 2025. Apply here.

Applications are still open for the 2025 FATE Institute Fellowship, a two-year, part-time and virtual programme for experienced Nigerian professionals passionate about entrepreneurship and policy reform. The fellowship is open to candidates with at least 10 years of relevant experience and a completed or ongoing Master’s or PhD in fields like Economics, Law, or Political Science. Fellows will work remotely, contribute to research on Nigeria’s entrepreneurship ecosystem, engage with policymakers, and take part in virtual policy discussions, without needing to leave their current roles. Apply by July 25.

We’re launching TechCabal Insights Market Researcher, a tool that helps you find and analyse African tech and business data in seconds. Whether you’re looking for startup funding numbers, market trends, or investor activity, it does the digging for you—fast and accurately. Be the first to try it. Join the waitlist.

P:S If you’re often missing TC Daily in your inbox, check your Promotions folder and move any edition of TC Daily from “Promotions” to your “Main” or “Primary” folder and TC Daily will always come to you.

As OkayAfrica marks our 15th anniversary, we're taking a look back at 15 defining African moments of the past 15 years that deserve to be remembered, and the impact they've had. Here's Moment No. 14. Click here for more OkayAfrica15 stories.Africa’s financial technology revolution didn’t happen overnight, but its speed and general impact in the past 15 years has been – and continues to be – nothing short of inspiring. Over the last decade and a half, the breadth of financial services Africans ha

As OkayAfrica marks our 15th anniversary, we're taking a look back at 15 defining African moments of the past 15 years that deserve to be remembered, and the impact they've had. Here's Moment No. 14. Click here for more OkayAfrica15 stories.

Africa’s financial technology revolution didn’t happen overnight, but its speed and general impact in the past 15 years has been – and continues to be – nothing short of inspiring. Over the last decade and a half, the breadth of financial services Africans have access to has been greatly widened, from digital payments processing and seamless global remittances to accessible premium banking services and even crypto investments.

At the start of the 2010s, using debit cards to withdraw cash from Automated Teller Machines (ATMs) was arguably the most impactful financial advancement in many African countries. However, in Kenya, the mobile money revolution was in full swing with M-PESA, which launched a few years earlier and fundamentally affected the landscape of financial inclusion.

With just T9 keyboard phones, Kenyans could deposit, send, receive and withdraw money through a network of agents and retail outlets, services that would typically require trips to bank branches. Targeted at the unbanked population, M-PESA, fronted by telecommunication giant Safaricom, was immediately popular and lauded as “the most successful mobile phone‐based financial service in the developing world.”

The blistering success of M-PESA was an indicator that Africa’s financial services system was in need of inventive approaches to widen possibilities. It also showed that widespread trust – a longtime issue in the sector – was attainable. “What M-PESA really did was to put some doubt into that idea that many of Africa’s unbanked did so because they didn’t trust banks,” economic consultant Gregory Hunpiyah tells OkayAfrica. “It takes a lot of boldness to get people to buy into having a wallet on phones that aren’t smartphones and it paid off.”

Although their contexts are different, there’s correlation between the explosion of M-PESA in Kenya to the breakouts of Fawry in Egypt and TymeBank in South Africa, and the fairly recent ultra-ubiquity of Opay in Nigeria. The premise of making financial services available to unbanked and underbanked populations represents an opportunity that has led to the launch of dozens of products across the continent, while traditional banks have also had to evolve accordingly.

Leveraging the internet as the ultimate technological advancement and coinciding with the rise of smartphone technology, fintech in Africa quickly diversified and has grown more effective over the years.

When Interswitch started operations in Nigeria in 2002, its ambitions as an integrated payment processing platform for businesses and banks was lofty. The process itself was cumbersome, requiring upfront payment and filling of multiple forms. In its evolution, Interswitch offered digital and data solutions to banks, was key to the ATM revolution, launched its own payments card company Verve, and ran the popular payment platform Quickteller. By 2019, Interswitch became the first African fintech company to be valued at $1 billion and earn the unicorn status.

“Interswitch obviously paved the way for Flutterwave, Paystack, HUB2 and these other payments companies,” Hunpiyah says. Late last year, HUB2 closed its Series A investment round, securing $8.5 million in funding as it looks to expand its payment solutions services across French-speaking African countries. Founder Ashley Gauzeresaid his company is “creating infrastructure and unifying payments in the region like a Stripe-like platform,” referencing the well-known American payments unicorn.

In October 2020, Stripe acquired Nigerian startup Paystack, which had been referred to as “the Stripe of Africa.” The merger and acquisition deal, which was reportedly worth about $200 million, was momentous, further proof that African fintech companies are creating world class products.

“That was the second deal that year that everyone went, ‘Wow!’ It was a little surreal,” Hunpiyah says. Two months before the Stripe-Paystack deal, cross-border payments company WorldRemit announced it was acquiring Sendwave, a remittance-focused company, in a deal worth over $500 million. “Granted, Sendwave operates from the U.S. but its focus is in Africa, and that’s what made the deal possible in the first place.”

During the COVID-19 pandemic, dozens of African tech companies received millions of dollars in investments, a show of optimism in a growing ecosystem. That funding spree has slowed down as the limitations of operating fintech startups in Africa have surfaced over the years, including low but growing level of internet penetration, stiff competition and oversaturation, regulatory obstacles, and a few cases of financial mismanagement. With investors, mainly outside the continent, being more selective about who to back, the question of scale and profitability have become more prominent than ever.

“A lot was made out of potential during COVID,” Hunpiyah says. “I think hard lessons were learnt after that and, to be positive, I think it’s shown that African startups can be resilient. Many companies have scaled back and tried new execution strategies to figure out what can work, which is something to write home about.”

Even amidst the market correction, the number of fintech companies in Africa almost tripled between 2020 and 2024, according to a report by the European Investment Bank. It signals a positive future outlook for fintech growth across the continent, as new unicorns are minted and more join the club. Last year, TymeBank and Nigeria’s Moniepoint joined the billion-dollar valuation list, stamping their impact on retail commerce and their role in improving the accessibility of banking services.

In its report, ‘Redefining Success: A New Playbook for African Fintech Leaders,’ McKinsey suggests that fintech revenues could reach up to $47 billion, depending on penetration across the continent reaching 15%. The report also shared six dynamics shaping trends in the ecosystem, including the acceleration of product innovation and fintechs integrating into other verticals. Opay is a great example of the latter, it evolved from the popular browser Opera into a superapp where users can open a bank account just with their phone numbers and carry out a myriad of transactions.

“It’s impossible to miss the impact of fintech companies that have proven themselves by just growing,” Hunpiyah says, referencing MNT-Halan, Egypt’s first fintech unicorn that started as a digital lending service. MNT-Halan has expanded into e-commerce and also offers buy now, pay later solutions.

Hunpiyah concludes that as much as it is about profits, the social aspect of African fintech will always be relevant because “these products are clearly improving quality of life for many Africans.”

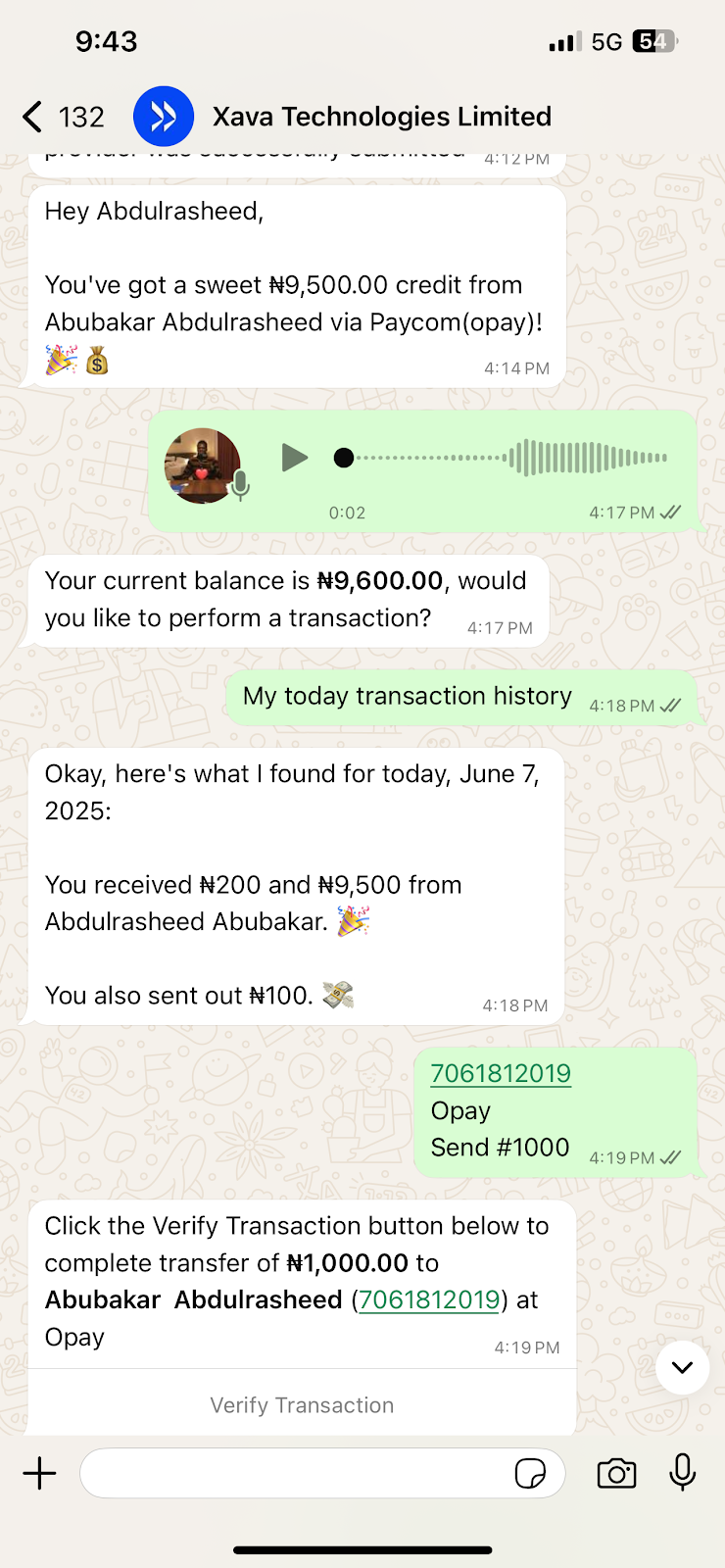

As mobile banking adoption surges across Nigeria, users demand faster and simpler ways to manage their money, without switching apps or dealing with clunky interfaces. Xara, a new WhatsApp-based AI assistant, is promising to change that.

Xara, a multimodal artificial intelligence banking bot launched in June by Nigerian software engineer Sulaiman Adewale, allows people to send money, pay bills, and analyse spending as naturally as texting a friend. The bot is built entirely inside WhatsApp, u

As mobile banking adoption surges across Nigeria, users demand faster and simpler ways to manage their money, without switching apps or dealing with clunky interfaces. Xara, a new WhatsApp-based AI assistant, is promising to change that.

Xara, a multimodal artificial intelligence banking bot launched in June by Nigerian software engineer Sulaiman Adewale, allows people to send money, pay bills, and analyse spending as naturally as texting a friend. The bot is built entirely inside WhatsApp, used by 95% of Nigeria’s 31.6 million social media users.

“I wanted an easier way that carries everybody along in banking, and if you look at it properly, you will see that WhatsApp is what even the oldest people among us use,” Adewale told TechCabal.

The product enters Nigeria’s crowded fintech space with a different approach: cut out the friction and build on top of what consumers already use. The company considers Owo, an AI managed by Mono and designed to facilitate payments on WhatsApp, as its closest competitor.

According to Adewale, Xara is powered by an existing large language model (LLM), the same underlying technology behind generative AI tools like ChatGPT. It is also trained on images and voices, especially accented Nigerian speech patterns, using open-source data tailored to its specific use case.

The AI understands commands in natural language, interprets them appropriately to confirm details, and processes the transaction in real time. “Send ₦10,000 to Abubakar for breakfast,” a user might chat this with the AI, and it will process.

“We have focused on just pidgin and English, but we are currently working on it to make it even understand our local languages like Hausa and Yoruba,” said Adewale.

To make the AI a personal financial assistant, users add their WhatsApp number, and once onboarded, they are linked to a payment source, currently 9 Payment Service Bank (9PSB), which issues user account numbers. Adewale said the team is working on partnering with more banks, so users can choose their preferred bank.

TechCabal tested the AI bot for two weeks and found that it understands and can process transactions with images, voice notes, text, and can analyse user spending and schedule payments. It remembers conversions with users and is capable of saving recipients as beneficiaries.

About 10,000 users have been registered on the platform, and over ₦135 million ($88,200) worth of transactions have been recorded within the two weeks of its launch, Adewale claims. He added that his team is currently working on partnerships with other banks as its initial payment provider, 9PSB, could no longer handle the inflow of new users, causing it to pause new registrations

Stella Adeboye, a server at Kilimanjaro restaurant in Ilorin, said Xara could serve as an alternative for easy payment for customers who had to raise their heads multiple times to check account details on the wall to make transfers for bill payment.

“If this tool can take a picture of an account number and process the transfer instantly, I think it would help us and also make payments much easier for customers,” Adeboye said.

To its early users, how their personal and financial data are secured has been a major concern. “Being able to bank via WhatsApp without opening another app is convenient, since it works even on a low network connection,” said Babatunde Hassan, one of the users. “But I’m worried about how our information is secured, and I’m sure that doubt may also hold other people back.”

In response to how users’ data is secured, Adewale said that the AI is built to use WhatsApp’s existing end-to-end encryption to safeguard users’ data. This means that conversations are private and inaccessible to third parties. He also noted that it requires an optional 4-digit authentication PIN to authorise transactions to beat fraud or compromise accounts.

“We don’t retain those personal banking details ourselves; the only data we log is related to payment transactions, just for tracking and resolution purposes, if any issues arise,” he said. “For extra security, we advise users to lock their WhatsApp using Face ID or a password, or even lock their chats with the AI to keep transactions private.”

Adewale explained that in case of a WhatsApp account breach or lost phone, users can visit its customer support to “request that your account be blocked instantly.” Accounts can be reinstated once identification is provided.

When asked about the type of licensing governing their multimodal AI service, Adewale stated that they currently “rely on banking partners’ license” for regulatory cover, indicating functions through existing compliance frameworks held by its financial institution partners.

A game changer for financial inclusion?

According to the Central Bank of Nigeria (CBN), over 28 million Nigerians lack access to financial products and services, including money transfer services, despite the country’s financial exclusion rate dropping from 46.3% in 2010 to around 26% in 2023.

Financial analyst Victor Daniel said leveraging WhatsApp for banking services could encourage even further financial inclusion, especially since the platform works on low-end smartphones despite poor network connections.

“In the past years, fintech innovations have helped reduce the financial exclusion in the country, but we need more innovations like this that can give us more alternatives to traditional systems to achieve more financial inclusion,” he said.

Daniel added that tools like Xara may also offer a strong alternative to QR code payments, which have seen limited adoption in Nigeria due to technical know-how and fraud concerns. “By allowing users to simply snap an account number from a note or screen and initiate a transfer through natural language, that provides a simpler payment service.”

While the focus is currently on Nigeria, Adewale said he envisions Xara AI banking assistant reaching more African countries where WhatsApp is dominant and banking remains a challenge. He also bets that the tool will disrupt the fintech landscape and “replace a lot of fintechs, hopefully.”

“We are still working on integrating additional services like savings plans, utility payment, and even e-commerce and logistics, like telling it to order food for you, and it will still do.”

Mark your calendars! Moonshot by TechCabal is back in Lagos on October 15–16! Join Africa’s top founders, creatives & tech leaders for 2 days of keynotes, mixers & future-forward ideas. Early bird tickets now 20% off—don’t snooze! moonshot.techcabal.com

Cape Town-based venture capital firm Knife Capital is marking its 15th anniversary with a pair of new Series A investments into South African startups Sticitt and Optique; two tech-driven businesses tackling entrenched problems in school payments and eye care.

Fintech startup Sticitt, founded in 2018 by Theo Kitshof, is digitising school payments while gamifying financial literacy for students. Its platform is used by over 75,000 users across 841 schools and has processed more than ZAR 6.3 B

Cape Town-based venture capital firm Knife Capital is marking its 15th anniversary with a pair of new Series A investments into South African startups Sticitt and Optique; two tech-driven businesses tackling entrenched problems in school payments and eye care.

Fintech startup Sticitt, founded in 2018 by Theo Kitshof, is digitising school payments while gamifying financial literacy for students. Its platform is used by over 75,000 users across 841 schools and has processed more than ZAR 6.3 B in transactions.

Beyond simplifying how parents pay for school services, the company, which previously raised seed funding in 2022, is positioning its youth banking tool as a driver of long-term financial inclusion. Knife’s investment builds on earlier backing via Grindstone Ventures, with this latest round intended to streamline the cap table and accelerate expansion.

Optique, launched in 2017, is challenging the traditional optometry model with a digitally enabled, low-cost offering. With 19 branches and an online store, the company targets under-served South Africans, offering ZAR 99.00 eye tests, all-inclusive pricing, and interest-free plans.

Founder Leon van Vuuren said the Knife backing will support national growth and bring world-class eye care to consumers left behind by legacy providers.

Knife Capital, which manages three funds, including the newly launched Knife Fund III, says these bets reflect a sharper focus on scalable, impact-driven innovation as it enters its next growth phase.

In much of Africa, trade isn’t held back by a lack of goods or buyers but stalled by cash flow. Exporters ship products, then wait 30, 60, sometimes 90 days to get paid. Banks, when they show up at all, take weeks to process financing and charge fees that make it unworkable for small firms.

Ghanaian startup Liquify is betting that this friction can be abstracted, standardised, and sold as a scalable asset class.

The company just raised USD 1.5 M in seed equity and additional debt financing

In much of Africa, trade isn’t held back by a lack of goods or buyers but stalled by cash flow. Exporters ship products, then wait 30, 60, sometimes 90 days to get paid. Banks, when they show up at all, take weeks to process financing and charge fees that make it unworkable for small firms.

Ghanaian startup Liquify is betting that this friction can be abstracted, standardised, and sold as a scalable asset class.

The company just raised USD 1.5 M in seed equity and additional debt financing to expand its digital invoice-financing platform, which helps small exporters in Ghana and Kenya get same-day cash for unpaid invoices.

Since launching its beta in late 2024, Liquify has financed over USD 4 M in transactions, mostly agricultural and light manufacturing exports headed to Europe and North America, as it pursues a quest to close Africa’s USD 120 B annual trade finance gap.

The pitch is classic fintech: speed, automation, and bypassing banks. Liquify’s platform wraps onboarding, KYC, AML, credit scoring, and settlement into a streamlined process that clears invoices in hours, not weeks.

“The average bank process takes over 10 days and costs more than USD 10 K to serve a single SME,” said co-founder and CEO Nadya Yaremenko, a former Citi exec who managed a USD 3 B trade finance portfolio. “We bring that down to a fraction of the time and cost.”

But what Liquify is really doing is making trade receivables investable. The startup buys export invoices at a discount, offering liquidity to SMEs while giving global investors access to short-term, self-liquidating assets, unlinked from broader financial market swings. Investors get yield; exporters get working capital. Everyone avoids the banks.

Of course, there’s a reason this gap hasn’t been filled. The team has had to build trust with SMEs used to informal lending and persuade foreign investors that fragmented invoice claims from African exporters can function like an asset class.

Co-founder Alberta Asafo-Asamoah, who came from the impact investing world, saw up close how “patient capital” wasn’t fast or flexible enough to scale SME exports. Liquify is taking a more transactional route, one that looks less like aid and more like arbitrage.

With the new funding, Liquify plans to expand its risk and compliance engine, grow into Francophone Africa, and test structured investment products.

Whether African trade finance becomes fintech’s next frontier or just another category of repackaged risk may depend on how well the startup balances local complexity with global appetite. For now, Liquify is betting that Africa’s slowest money problem is also its most bankable.

Banking in South Africa just took a sharp digital turn. Lesaka Technologies, the fintech firm formerly known as Net1, is acquiring 100% of digital banking upstart Bank Zero in a ZAR 1.1 B (~USD 61 M) deal.

It’s a rare merger of fintech infrastructure and a full banking license that could redefine how financial services reach underserved customers across the country.

The acquisition—announced via a late-night social post by Bank Zero chairman and ex-FNB CEO Michael Jordaan—is being paid for

Banking in South Africa just took a sharp digital turn. Lesaka Technologies, the fintech firm formerly known as Net1, is acquiring 100% of digital banking upstart Bank Zero in a ZAR 1.1 B (~USD 61 M) deal.

It’s a rare merger of fintech infrastructure and a full banking license that could redefine how financial services reach underserved customers across the country.

The acquisition—announced via a late-night social post by Bank Zero chairman and ex-FNB CEO Michael Jordaan—is being paid for in a mix of Lesaka shares and up to ZAR 91 M in cash.

The deal gives Bank Zero’s shareholders a 12% stake in Lesaka and signals a strategic pivot. Lesaka, having made its name providing fintech rails, now wants to own a bank, too.

Founded in 2021 by Jordaan and banking veteran Yatin Narsai, Bank Zero has quietly built one of the most radically low-cost banking platforms in South Africa.

Its digital-first, zero-fee model has attracted more than 40,000 funded accounts and ZAR 400 M in deposits, without a physical branch in sight. Its patented card technology, which offers separate numbers for different transaction types, is one of many innovations designed to limit fraud and put control back in the hands of users.

But while Bank Zero focused on design and compliance, it lacked scale. Lesaka, on the other hand, has deep distribution across consumer and merchant segments, including a presence on both the Nasdaq and Johannesburg Stock Exchange.

The pitch is synergy: embedded lending, cross-sell, operational leverage. But the real story is about control—of data, of deposits, and of destiny.

By absorbing Bank Zero’s banking license and tech stack, Lesaka gets to escape its dependency on third-party banks. That opens the door to better margins on lending, a tighter loop on customer behaviour, and more regulatory flexibility. It’s also a bet on long-term infrastructure over short-term fintech flash.

Jordaan and Narsai will stay on, and no layoffs are expected following a move that may well signal what the future of South African finance could look like—digitally native, vertically integrated, and built for people who have never truly had a bank that worked for them.

Kenya’s digital payments infrastructure is growing. But growth alone is not enough. Without open, affordable, and interoperable systems, the promise...

Source

Kenya’s digital payments infrastructure is growing. But growth alone is not enough. Without open, affordable, and interoperable systems, the promise...

Integrated Payment Services Limited (IPSL), the operator of Pesalink, has signed a Memorandum of Understanding (MoU) with The Fintech Alliance,...

Source

Mastercard has collaborated with payments solutions company enza to connect fintech companies across Africa to the Mastercard network. This collaboration...

Source

Mastercard has collaborated with payments solutions company enza to connect fintech companies across Africa to the Mastercard network. This collaboration...