Why Brand Evolution Could Be Catalyst For Growth

26 août 2025 à 07:49

Everything evolves—people, markets, businesses. Comfort is temporary, and real growth demands a measure of change. For some companies, that change...

Everything evolves—people, markets, businesses. Comfort is temporary, and real growth demands a measure of change. For some companies, that change...

Kenya is once again setting the pace for digital finance innovation in Africa. Building on the runaway success of M-Pesa,...

Ghana is taking decisive steps to bring cryptocurrency under official oversight, with plans to license and regulate digital asset platforms in a move that could reshape the country’s financial landscape.

The Bank of Ghana is finalising a regulatory framework expected to reach parliament by September, according to Governor Johnson Asiama. This development comes as millions of Ghanaians have already embraced cryptocurrencies for daily transactions and cross-border trade, despite operating in a legal gray area until now.

The push for regulation reflects both the growing influence of digital currencies in Ghana’s economy and the challenges they pose to traditional financial systems.

With an estimated 3 million Ghanaians (about 17% of the adult population) using virtual currencies, authorities are keen to bring these transactions into the formal financial sector. Recent data shows Ghana recorded USD 3 B in cryptocurrency transactions between July 2023 and June 2024, per Web3 Africa Group, though this pales in comparison to neighboring Nigeria’s USD 59 B volume during the same period.

Governor Asiama acknowledged the urgency of regulation, stating “We are actually late in the game.†Many economic activities involving cryptocurrency payments currently escape official records due to the lack of oversight, creating blind spots for monetary policymakers.

This gap has become particularly problematic given the Ghanaian cedi’s dramatic fluctuations – the currency gained 48% over the past year following a 25% drop in the previous 12 months. Such volatility complicates inflation management in a country heavily dependent on imports.

The proposed framework aims to strike a balance between harnessing cryptocurrency’s potential benefits and mitigating its risks. Officials hope regulation will help stabilise the local currency, attract strategic investment, and improve financial transparency while protecting consumers from fraud. Kwame Oppong, head of fintech and innovation at the central bank, emphasised the need for safeguards, noting “Our goal for this whole process is to put safe guards and rails around it.â€

With inflation at 13.7% and policy interest rates at 28%, the stakes for getting this balance right couldn’t be higher for Ghana’s economic future. As Ghana joins a growing list of African nations establishing cryptocurrency regulations, the coming months will reveal how effectively the new framework can reconcile innovation with financial stability in one of West Africa’s most dynamic economies.

The post Ghana Moves To Regulate Cryptocurrency As Millions Embrace Digital Assets appeared first on WeeTracker.

If you earned crypto for the first time ever during the mid-2010’s, chances are you made that money creating posts on Steemit.

For many Nigerians and Africans, crypto publishing apps like Steemit and Publish0x provided the gateway to access crypto. Users made money by writing micro-blogs, growing their engagement and following, and earning from being top contributors on the platforms.

Platforms like Steemit and the much-changed Publish0x were social finance (“SocialFi†in Web3 lingo) apps that allowed users to monetise interactive activities. It was like using Facebook or Reddit, but in a way that you were paid for simply being online.

At its peak between 2017 and 2018, Steemit had over 100,000 Nigerian users on its platform; in Africa, the number was slightly more. The SocialFi app claimed micro-bloggers could earn up to $2.11 for a day’s work.

Nigerian users took it seriously. Influencers on the platform and community leaders hosted physical meet-ups in cities like Lagos, Ibadan, Kaduna, Uyo, and Port Harcourt to teach others how to use the app. They formed local support groups to help newcomers sign up, learn the basics, and grow their earnings.

All that hype from several years ago has now died down. Users, impatient with Steemit’s reward system, began leaving the platform. In recent times, there’s been little sign of platform upgrades or efforts to fix ongoing issues.

Founded in 2016 by Ned Scott and Dan Larimer, Steemit was built as a social media platform on the Steem blockchain, owned by the same company. The Steem blockchain also has its digital token, $STEEM, currently priced at $0.1430. Outside of the Steemit platform, people hardly used $STEEM.

People created posts—educational, inspirational, topical, or anything else—and earned money when others “upvoted†them. The more upvotes (similar to “likes†on Facebook or Instagram) your posts received, the more money you made—usually a few $STEEM tokens. During payout days, creators could then transfer their earnings from their Steemit wallet, a built-in custodial wallet, to other crypto wallets like Trust Wallet.

This was before crypto exchanges such as Quidax, Busha, Luno, and the likes exploded in popularity. So, to get other mainstream crypto coins like Bitcoin or Ether, Steemit bloggers had to explore informal peer-to-peer (P2P) channels like WhatsApp groups, to find whom to exchange their $STEEM tokens with. In the same vein, they could also exchange $STEEM for fiat currencies like US dollars or Naira.

Steemit had a feature called “Steem Powerâ€â€”a locked-up version of the token that gave users more voting power. If you had more of it, your upvotes carried more weight and could help creators earn more. This meant that the people with the most Steem Power had a lot of influence on who got rewarded.

Steemit also rewarded people for curating content. This means if you upvoted good content early enough, you earned a part of the payout too. Users also earned through comments, especially if their replies added value to a post or conversation. The more helpful your activity on the platform, the more likely you were to earn something from it.

The platform ran a built-in reward cycle that took about seven days. So every post had about a week to gather engagement before it was evaluated for payout. All of this was tracked publicly on the blockchain, so people could always check the numbers for themselves.

However, the kryptonite of most creator-centric platforms is human wisdom—and how far people are willing to go with that wisdom. As you may already suspect, Steemit users saw a way to game the system. They would cluster themselves in small groups, called “podsâ€, on Telegram or WhatsApp, and engage with one another’s posts.

This made it easy to cheat the system. People would just upvote their friends’ posts to help them earn more. Over time, this led to poor-quality content rising to the top. The platform tried to stop it with “downvotes,†a way for users to call out low-value and spam posts. Creators caught doing this forfeited a significant portion of their earnings.

In 2019, Steemit broadened its community rules in a further bid to curtail low-value posts. Afterward, it also started taking action against users who used AI tools to generate content, especially when it was obvious the content lacked originality or context.

To tackle the pod problem, Steemit introduced a reputation system, rating users on a scale of 1 to 100. The more your reputation grew through valuable posts and comments, the more weight your upvotes and downvotes carried. If a user with a high reputation upvoted your content, you earned more money than if someone with a low reputation did. This discouraged people from creating fake accounts or relying on new users to game the system.Â

But these strict measures came with a price. As the rules became more rigid, some users felt discouraged. Many of them began migrating to Publish0x, which launched in 2019, and others moved to Hive, a spin-off platform, in hopes of increasing their earnings.

Publish0x started as a social media and microblogging platform. Today, Publish0x partners with survey providers to allow eligible users, depending on their location and interests, to take part in surveys and earn credits. These credits can then be swapped for real money. Though still active, user activity appears to have dropped over time.Â

Steemit claims it has now crossed over 1 million users, and that 14.4% of them, as of June 2025, are Nigerians. Around the world, 63.8% of its users are from emerging economies like Indonesia, Bangladesh, Nigeria, Pakistan, and Thailand.

The company also says it paid out $59.6 million to creators in June 2025 alone and records over 1 million transactions every 24 hours on its blockchain, pointing to high demand and usage.

According to Semrush, a content marketing platform, Steemit’s website had about 2.2 million visits in June. Online traffic tracker, Similarweb, says 67% of those visitors are men, while 33% are women.

While there may now be over 140,000 Nigerian users on Steemit, a generous estimate will put active daily users—people who use Steemit app daily—in the low thousands. Many Steemit communities have gone quiet, and several of the influencers who helped popularise the platform in Nigeria have since left.

Yet, some Nigerians, still active on Steemit, have managed to cash out over $10,000 from their lifetime activity on the app. For example, Joseph (@josepha), a Nigerian Steemit user who was active 6 hours ago, has earned $7,214.42 overtime; $165.72 in the last month, and $35.26 in the last week. TechCabal was able to verify this on Steemit’s publicly accessible records domain.

Ruth Joe (@ruthjoe), another influential user, has earned $4,076.75, while Ngoenyi (@ngoenyi), another influencer with 2,286 followers, has made over $12,500 in lifetime rewards.

Steemit’s engine is now sputtering, but it hasn’t hit the brakes yet. Devoted fans are still making money from the SocialFi app, often replacing it as their main hustle, or a side income.Â

Mark your calendars! Moonshot by TechCabal is back in Lagos on October 15–16! Join Africa’s top founders, creatives & tech leaders for 2 days of keynotes, mixers & future-forward ideas. Early bird tickets now 20% off—don’t snooze! moonshot.techcabal.com

Luno, the UK-based crypto company which operates in South Africa, Nigeria—and recently, Uganda—now has a fourth horse to back in its Africa race: Kenya. On June 23, the company announced its re-entry into the East African country after a 2014 exit, expanding its regional presence.

Luno, operating as BitX, first entered Kenya in 2013. It was one of the first startups to offer cryptocurrency trading services in the country, alongside then-competitors—both foreign and local startups—such as Kipochi (which shut down after Safaricom blocked its access to M-Pesa), BitPesa (now AZA Group), and early peer-to-peer (P2P) marketplaces such as LocalBitcoins and Paxful.

The market Luno is returning to ten years later radically differs from the one it left behind. Over the past decade, Kenya has grown into East Africa’s most active cryptocurrency market. The rise of mobile money platforms like M-Pesa, coupled with increasing smartphone penetration and youth-driven digital adoption, has made Kenya a fertile ground for the sector.

Regulatory uncertainty pushed Luno to exit in 2014, but today, that environment is cautiously evolving. A new Virtual Asset Service Providers (VASP) Bill is in the works, promising formal licencing under the oversight of the Central Bank of Kenya (CBK) and the Capital Markets Authority (CMA).

In its comeback, Luno is betting on this regulatory shift—and its decade of experience across Africa. The company has grown to over 15 million global users and now holds a crypto licence in South Africa.

Yet, it won’t be an easy ride for Luno, as Kenya has become a tougher market to compete in with deep-pocketed foreign players such as Binance, Huobi, and OKX, gaining a foothold in the market with their local presence.

TechCabal spoke with Apollo Sande, Luno’s country manager for Kenya and Uganda, who has led the company’s expansion efforts in East Africa for six years.

This interview has been edited for length and clarity.

After more than a decade, why did it make sense to re-enter a market where there is still no licencing framework in place for crypto exchanges?

In 2014, the Central Bank released a circular that stopped banks from working with crypto exchanges and crypto enterprises in Kenya. This made Luno leave the market. Kenya was actually Luno’s second launched market back in 2013, before it began a global expansion.

Then sometime in 2019, Luno decided to take another look at its Africa expansion. I got onboarded and analysed the various markets in East Africa. We prioritised Uganda because it had regulatory certainty. It was easier to have discussions with the Bank of Uganda and other regulators—but Kenya was the prize. Kenya had always been in our sights given the size of its crypto market.

We planned for it and waited while maintaining ongoing interactions with regulators. We were involved in many discussions with authorities in Kenya and Uganda. In December 2024, we decided to re-enter the market. A soft launch has been running since then, and we have now moved to a full launch.

What structural risks existed in 2014 when Luno exited Kenya, and do they still exist today?

The biggest risk was the banking ban. It prevented the integration of crypto players with the formal financial system. Startups had to find alternative channels to on- and off-ramps, which led to the rise in P2P payment rails.

P2P rails pose massive risks for customers. They transfer platform risk to the customer. We have seen traders getting arrested or taken to court because they innocently transacted with bad actors. There have been lots of transaction failures, delays, and bad counterparties. The lack of regulation meant players had lax Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols.

This has continued until now. The upcoming regulations will clearly set the standard for crypto platforms. Back in 2012 and 2013, Luno deliberately chose to pay the cost of compliance in advance, knowing it would position us better for a regulated environment. That regulated space is now within reach.

We have formal anti-money laundering regulations and recognition for the industry. Compliant crypto players will secure a position in the market because of the level of trust and stability we bring to the market. We’re banking on this.

Crypto companies still operate in a grey area and no licences have been issued so far. Is this sustainable for long-term operations?

Based on earlier discussions, we observed progress in the regulatory environment. We positioned ourselves while continuing active engagement with regulators. Crypto is not banned in Kenya; only the payment rails were restricted. The methods customers use to deposit and withdraw money in the crypto industry are not yet optimal because we operate outside the existing traditional finance systems. It makes things a little difficult because the playing field is not level.

But see crypto startups as small businesses. It’s not banned, so we just find workarounds. For our Kenyan operations, we’ll make the same play we used in Nigeria when banks stopped working with crypto companies there, too, in 2021. We’ll introduce voucher payments to our Kenyan customers to enable them to easily deposit fiat, buy and sell crypto, and off-ramp to local currency.

In anticipation of upcoming regulations, we expect a lot more certainty. The tax code in Kenya for crypto is undergoing favourable improvement. Regulations are in the final stages at the National Assembly. We think the outcome will be very good for the industry. A lot of the dots have connected, and it is a timely move for us.

Who did Luno Kenya partner with for voucher payment services?

I’d prefer not to provide details about our partner.

The proposal in Kenya is to tax 10% excise duty on crypto transactions. If this goes through, how will this tax demand affect startups’ ability to comply?

Crypto tax was first enacted in 2013 with the previous finance bill. It was set at 3% of the gross value of all crypto exchanges and transfers. That tax was never collected because it was just impractical.

First, there weren’t any banking rails to remit the taxes. Second, that tax was almost 30 times the revenue that crypto exchanges made from commissions. It would have pushed the industry underground.

There has been intense lobbying from the industry. Fortunately, we have a strong team of technocrats within various regulatory bodies who can understand the issue, research it further, and engage with the industry. It became clear that the tax was unsustainable.

There is now an alternative proposal to tax the industry at 10% of the commissions. This is more or less in line with mobile money transfer charges—actually a little lower—plus a corporate income tax. There are still discussions about the applicability of value-added taxes (VAT). However, the tax now makes the industry sustainable. So pending how the regulations work out, at least taxation is not a barrier.

With regards to licencing, the Virtual Asset Service Providers (VASP) Bill has passed a second reading in Parliament. It was really encouraging to hear that level of understanding and foresight from Honourable Moses Kuria and several members of the National Assembly. We are hopeful of a forward-looking regulatory framework.

I always say we should ask what this industry could do for the economy and the country. Then from there, we can take out the risky parts that diminish that potential. Once the VASP Bill passes, the appointed regulators will then create specific licencing frameworks for the various types of players in the crypto industry. That is when we will have clarity about the pathway to licencing.

Who bears this 10% excise duty burden—the users or the crypto companies?

Previously, we would have had to withhold the customer’s trading capital, which could have made us a target. But with the 10% excise duty, which is common in financial services, we bear it. It is worked into our fees. It eats into our margins but offers a better customer experience and makes collection and remittance easier.

How does this affect Luno’s pricing model and trading margins?

It certainly reduces our margin because it is 10% of the fees we charge customers. There’s also a 30% corporate income tax to bear, and potentially a 16% VAT. Yes, it reduces our margins, but in a sustainable way. It’s workable compared to the previous proposal.

Does this result in additional costs for users on Luno Kenya?

That depends on individual business practices. Some businesses may pass the tax on through their fees. Others may absorb it and take the hit to their margins. Fee structures keep changing based on economic realities and business goals.

For Luno Kenya, we will continue to look at our pricing and keep adjusting it to ensure it’s sustainable, affordable, and acceptable for customers. It is an ongoing decision.

How do you view competition in Kenya, especially with P2P enablers like Binance?

Kenya is a rapidly maturing crypto market with many players. There’s a joke that a new crypto exchange or wallet service provider is launching every two or three weeks here. Competition is part of the game.

Over the past ten years, due to the regulatory environment, those who entered the space were mostly tech-savvy, young, high-risk, entrepreneurial individuals willing to endure the rough patches. They found a way with P2P, and that’s fine.

But there is a huge untapped market of people who would not operate within the frameworks of those P2P platforms. They prefer clarity and transparency in the services they use. That is the vast majority of Kenya’s potential crypto market.

Given the business conduct and governance structures of centralised exchanges like Luno, there is still a large gap we can fill. Competition will be tough, but the market is big enough. I don’t think P2P platforms have captured more than 20% of the potential market.

The VASP Bill will require companies to register with the Central Bank of Kenya and the Capital Markets Authority. How far along are you in engaging with these regulators?

We have engaged with all the regulators, with varying degrees of success. We have worked with the CBK, the CMA, and the Financial Reporting Centre. We’ve spoken to all relevant regulators. The same has happened across the industry.

In the past two years, the conversations have become clearer. Regulations are now under the government, and no regulator wants to front-run or prescribe anything until regulations are enacted.

Right now, it is about building relationships. Drafts indicate who will regulate what. But until licencing frameworks are issued, it’s a wait-and-see approach. A new regulator has also been proposed, and their scope will be defined once the bill and frameworks are formalised. Right now, we wait, observe, prepare, and adjust as needed.

How will Luno Kenya monitor transactions on its platform to meet AML expectations and regulatory standards like the travel rule?

Currently, Luno is available in about 40 countries and is licenced in multiple jurisdictions. Some of these countries have very strong AML, KYC, and counter-proliferation processes, which comply with requirements around the travel rule.

We have been managing these risks and monitoring transactions from the start. We’ve been self-regulating where necessary, even when specific crypto regulations did not yet exist. Many of these standards were adopted from the way traditional financial service providers are being regulated in Kenya.

We comply with FATF guidelines and those of other regulators. We have strong anti-financial crime, compliance, and cybersecurity teams and mature systems in place.

We also conduct training for regulators and law enforcement on various aspects of these systems. Transaction monitoring is one of our key strengths.

Can you describe some of the tools and methods Luno Kenya uses to flag suspicious transactions?

We have a team dedicated to this. We conduct basic KYC—individual and business due diligence (for institutional users). We also perform ongoing transaction monitoring and use tools like Chainalysis and Elliptic for on-chain monitoring.

During onboarding, we assess the source of funds and customer behaviour. We check for sanctions and politically exposed persons (PEPs). Chainalysis also flags wallets linked to banned activities. We monitor customers’ trading activity, and when there is a significant change from their usual pattern, we flag this and apply enhanced due diligence (EDD).

We also monitor third-party deposits and use geo-location and geofencing tools to identify high-risk areas and trace use of virtual private networks (VPNs). We monitor for on-chain and off-chain risks such as dark markets, gambling, and high-risk jurisdictions. We detect fraud, platform abuse, and payment fraud. We defend accounts by alerting customers to phishing and scams and blacklisting malicious devices.

Screening controls, alerts, and a comprehensive risk management framework help us integrate all compliance and monitoring tools into a cohesive system.

All this integrates into a centralised risk management framework for AML, CTF, and counter-proliferation compliance.

How much capital is Luno Kenya committing to its local operations?

We operate with the backing and support of our centralised teams that manage global operations. In markets with larger operations, there are more localised teams. Much of what we do is customised to each country’s needs. Luno Kenya benefits from strong support from our central team.

Luno has evolved from a crypto and stablecoin off-ramp into a broader crypto exchange. Will Luno Kenya launch with this full range of services or a more limited product?

Since 2013, Luno has had a full order book exchange alongside the instant buy/sell functionality. We’ve always offered wallets for storing, sending, and receiving crypto. The instant buy/sell option lets users trade without comparing quotes, and we also have a live exchange with an order book for more flexible trading.

In most markets, the wallet and instant buy/sell functions are the most used. These services have been part of Luno from the start, along with on- and off-ramping. We are debuting in Kenya with the full range of these services.

The change in recent years has been a ramp-up in the number of listed coins on our platforms.

Does Luno charge for listing coins? And how do you decide what to list?

Like most exchanges, we earn commission on transactions. We facilitate secure and liquid trades and charge a small fee for this.

We have a coin listing committee and team that relies on third-party analysis to assess the credibility of coins. We don’t list everything. We try to be responsible and only list coins we would be comfortable investing in ourselves.

We currently don’t have a process for applications or paid listings. We monitor customer demand, assess what we’re comfortable listing, and then we approach the coin issuers.

What’s Luno Kenya’s stance on enabling the adoption of local stablecoins? Could Luno list local stablecoins like the Kenyan Shilling built on the Celo blockchain (cKES)?

We will continue to monitor these developments. It’s not currently under consideration, but it is a possibility. As we did with USDT and USDC, if there is a strong business case and demand, we’ll look at it on a case-by-case basis.

From a growth perspective, what’s Luno Kenya’s immediate goal and key performance metric?

Given Kenya’s P2P heritage, the market needs safe, simple, secure, and transparent service providers. That is what we’re offering, based on over 13 years of secure operations with no hacks, a reliable and user-friendly interface, and trustworthy service.

That alone fills a gap in the market. It offers a significant improvement in customer safety and experience. From that foundation, we will identify more specific goals.

You’re also the Country Manager for Uganda. What does that mean for the scope of your role with Kenya’s operations kicking off?

We’ve been operational in Uganda since 2019. At first, we had access to banking and mobile money rails, but about two and a half years ago, those were banned. We shifted to a crypto-only platform there. You can get in and out using stablecoins and other crypto.

We believe Kenya’s regulatory progress could be replicated in other countries. When there’s regulatory clarity in Uganda, we may consider reopening a full product suite.

For now, we remain active in Uganda as a crypto-only platform. Operations at this capacity will continue in Uganda while we focus on Kenya.

Mark your calendars! Moonshot by TechCabal is back in Lagos on October 15–16! Join Africa’s top founders, creatives & tech leaders for 2 days of keynotes, mixers & future-forward ideas. Early bird tickets now 20% off—don’t snooze! moonshot.techcabal.com

Two months after CryptoBridge eXchange (CBEX), the Ponzi scheme which falsely claimed to be a cryptocurrency exchange, froze withdrawals for thousands of customers on its platform, it is back with another gimmick, much to the chagrin of regulators.

CBEX never shut down its platform, despite warnings from Nigeria’s Securities and Exchange Commission (SEC) and multiple public arrest warrants issued by the Economic and Financial Crimes Commission (EFCC) for several persons linked to the Ponzi scheme.

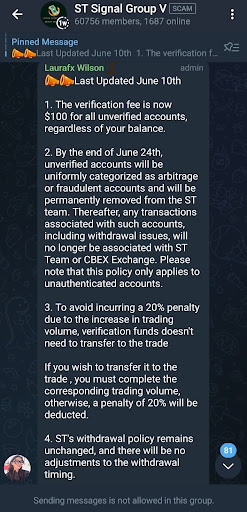

The platform has been operating under different domains, making it difficult for authorities to track its activities. CBEX is now asking users to pay a $100 “verification fee” to enable them to withdraw their frozen balances, according to messages shared on engagement groups seen by TechCabal. Once they do, these users get access to “sub-accounts” which allow them to continue their daily trading activities as they’re instructed on the platform.

“The verification fee is now $100 for all unverified accounts, regardless of your balance,” CBEX said in one of those messages. This is a deviation from its previous method, where it asked users to pay $100 for balances below $1,000 and $200 for balances above $1,000.

According to updates seen by TechCabal, withdrawals will be sorted out in batches and are contingent upon users completing their assigned daily trading activities. CBEX claims it will process 50% of all pending user withdrawals by June 25 and the remaining 50% by August 25. It also says 30% of profits from users’ trading activities will be paid out under a revenue-sharing model on October 25.

Nigerians, desperate to get back their money, have begun paying the verification fee. After payment, they gain access to a dashboard showing their frozen balance as of April. Their balance begins to grow again once they engage in activities that generate revenue, such as referring new users or trading using CBEX’s daily signals. The signals are codes shared manually on CBEX engagement groups; users copy them at specific times when they’re released and paste them in their apps.

Regulators are alert to the issue. On June 11, the SEC issued another warning, cautioning Nigerians to refrain from investing money in CBEX.

“The Commission hereby restates unequivocally that neither CBEX nor ST Technologies International Limited or Smart Treasure/Super Technology [CBEX’s partner] is registered with the Commission, or authorised to offer investment-related services to the Nigerian public,” SEC wrote in the public statement.

The EFCC has listed six Nigerians in connection with the platform, declaring them wanted. Several media publications also reported that the anti-graft agency recovered part of the stolen funds on May 26. However, Nigerians who were hopeful of the EFCC’s progress at the time, now left to hang dry, are taking matters into their own hands.

In one of the Telegram groups connected to ST Technologies, a CBEX partner, several Nigerians are already making payments and referring friends to the platform.

Old users are hurrying to pay the verification fee against a June 24 deadline. They are also roping in new entrants who are making USDT transfers exceeding thousands of dollars to join CBEX.

“Depositing $100 is the only way to verify your account,” wrote an ST admin, who only identified as Laurafx Wilson in one of the groups.

A CBEX user on Telegram claimed that he was paid by the platform after he verified his account. However, they declined to share proof of this payment when TechCabal reached out. CBEX still maintains it will clear 50% of all delayed payments on June 25.

While many Nigerians are shuffling back to CBEX to recover their money—and try to earn some more while they’re at it—others are cautious.

“Why can’t they charge the $100 on our balance and allow us back into the platform?” said Favour Kwaghgande, a CBEX user whose account got frozen in April. “That was my school fees I invested, and honestly, I have no idea where to raise another $100 to redeem my account.”

CBEX representatives have claimed that the verification fee is necessary to filter “fraudsters” and “illegal arbitrageurs” hidden among their members. The logic here is that if the platform remains free, fraudsters could exploit the system to create multiple fake accounts and siphon unearned money.

Arbitrageurs, on the other hand, could be using CBEX only to exploit price differences, buying cryptocurrencies low and selling high on other platforms. Therefore, the platform wants to keep these sets of users locked out.

Yet, it could just be a convenient ruse for CBEX to appear credible and collect more money from desperate users. By placing a fee on withdrawal, CBEX is dangling an apple in the faces of helpless Nigerians who are already taking the bait.

“[CBEX] is most likely fetching prices from an oracle,” said Adebayo Solomon, a Nigerian blockchain engineer. “The price differences [on its app] could vary slightly from other places, but most times, it is almost negligible. If they’re truly worried about people gaming the system, they could use a decentralised authentication solution like zkpass to ensure it’s one account per user, but they’re not doing that.”

It is also baffling that Ponzi schemes like CBEX remain in operation, with several others joining the fold. Tofro and FutCoreCoin—two platforms with similar operations as CBEX—are coming up, and they’re marketing themselves to the circle of users that invested in CBEX.

While the SEC has become more proactive in issuing warnings about these platforms through circulars, it may need to intensify efforts to cut these operations at the head. As far as consumer protection goes, the regulator has the authority to shut down non-compliant securities exchange platforms, and perhaps needs to, to protect Nigerians from themselves.

Mark your calendars! Moonshot by TechCabal is back in Lagos on October 15–16! Join Africa’s top founders, creatives & tech leaders for 2 days of keynotes, mixers & future-forward ideas. Early bird tickets now 20% off—don’t snooze! moonshot.techcabal.com