At Moonshot 2025, we’re bringing together the builders, dreamers, and doers who are turning ideas into impact and scaling what’s next for Africa’s digital economy.

Picture this: 5,000 attendees, founders, creators, investors, policymakers, and industry leaders in one space, sharing playbooks, lessons, and finding collaborators who understand the grind of building. This isn’t just a conference; it’s a propeller. Whether you’re fine-tuning your startup, scaling your operations, or creating digital products that push culture forward, Moonshot is the place to gain the insights, connections, and energy to keep building.

Don’t just watch the future take shape, be a part of the force driving it

We have no crystal ball, but you likely had two reactions when you saw MultiChoice in today’s newsletter: ‘Did the pay-TV company finally reduce its DSTv prices?’ or ‘has it entered trouble with another regulator?’

Your thoughts are well…your thoughts. But MultiChoice is hogging the headlines again for the high-profile Canal+ takeover. On Tuesday, the company said it has started restructuring its businesses to accommodate the French media outfit operated by the Vivendi Group. The R55 billion ($3.17 billion) buyout, which has been a public spectacle since Canal+ first bought shares five years ago, is coming to an end.

Catch up: After Canal+ made a mandatory buyout offer to acquire 36.6% of the South African pay-TV company in 2024, it triggered a clause that gave the acquirer the right to make a takeover bid. It offered R125 ($7.21) per share to take over MultiChoice. Following approval of the deal, both companies have been scrambling to set up rules that allow Canal+ to own controlling stakes.

State of play: MultiChoice has since established a subsidiary, LicenceCo, which holds its broadcasting licences. It will reduce its controlling stake in LicenceCo to 20% to allow the deal to meet competition and foreign takeover requirements in South Africa.

Questions, questions: With this restructuring, where do consumers fit in? What changes for them? MultiChoice continues to oversee its operations, media content, and branding across platforms, according to CEO Calvo Mawela. The deal is unlikely to include a resource-sharing pact, so Canal+, one of France’s largest streamers, won’t merge its content into MultiChoice or vice versa.

We are edging closer to a monumental shakeup in Africa’s pay-TV market, with one of the continent’s biggest companies at the centre of it.

eCommerce Without Borders: Get Paid Faster Worldwide

Whether you sell in Lagos or Nairobi, customers want local ways to pay. Let shoppers check out in their local currency, using cards, bank transfers, or mobile money. Set up seamless payments for your global online store with Fincra today.

Banking

Tanzania’s biggest bank upgrades its core banking system to chase growth

Tanzania’s largest bank by assets, CRDB Bank, has replaced its old core banking system, the Fusion Banking Essence (FBE) by Finastra, with Temenos T24, the Swiss platform used by heavyweights such as KCB and Stanbic Bank. This migration happened in early September.

Why? CRDB wants to move beyond East Africa into Dubai, and you can’t really make that big move with outdated infrastructure. Not to mention keeping pace with regional competitors.

Core banking isn’t like upgrading a mobile app. It requires shifting millions of sensitive user records at a go. CRDB’s migration had the usual teething problems of service lags and balance mismatches. But they insist it was a critical move for efficiency.

What’s new? CRDB can now allow people to initiate transactions in English, Swahili, French, Kirundi, and Arabic. The new system also supports transactions in multiple currencies.

Why it matters. By jumping on Temenos T24, CRDB is signalling regional and global players that it is ready to play hardball. The upgrade gives the lender the backbone to chase diaspora money in Dubai and roll out products faster. With the Bank of Tanzania (BoT) nudging local banks to modernise their systems, other East African banks are likely to follow CRDB’s footsteps.

Shop anywhere with Paga’s physical prepaid card

Own every checkout with Paga’s Physical Prepaid Card. Suitable for all your security and speed needs. Just fund, shop, and pay anywhere with confidence. Get yours today.

Companies

South Africa’s Naspers wants to make its shares 5 times cheaper for investors

Image Source: Bloomberg

Remember when Alphabet, the parent company of Google, did a 20-for-1 stock split on the NASDAQ in 2022? Did you buy its shares? Because Naspers, one of Africa’s largest technology conglomerates, is following suit.

When it comes to the stock market. Some may think it’s all just an expensive gamble with a bunch of imaginary numbers and prices for big players that make little sense. Naspers wants everyone to think differently.Â

State of play: It announced a 5-for-1 share split on the local bourse, the Johannesburg Stock Exchange (JSE), which will be effective from October 6. A stock split means each existing share is divided into smaller units, so the price per share drops, but the overall value of your investment stays the same. Companies with pricey shares typically use stock splits to make them affordable for smaller investors.Â

By the close of market on Tuesday, Naspers’ shares were trading for R5,885.40 ($339) per unit; this means buying 100 shares costs nearly R600,000 ($34,500) before the split, among the highest prices on the JSE and locking out smaller investors. With this new split, the R600,000 ($34,500) investment could become R120,000 ($6,900) for the same ownership stake.

Between the lines: Most of Naspers’ valuation comes from its roughly 23% stake in the Chinese technology giant, Tencent. Tencent is valued at approximately $760 billion. Despite Nasper’s high stake, it is only valued at $53 billion; this gap tends to raise eyebrows.Â

The split doesn’t change the company’s value, but it lowers the price per share, boosting liquidity and making the stock more accessible.Â

This move is part of a bigger clean-up: Naspers has been buying back shares and tidying up its structure to convince investors that its value should be closer to what its books show.Stock splits can’t solve everything, but they can help close that valuation gap by drawing in smaller investors and improving market trading activity.

Accept Payments with Apple Pay on Paystack!

Anyone can get paid globally. With Paystack and Apple Pay, let customers pay you instantly and securely from 60+ countries. Get started here →

Economy

Nigeria’s inflation rate goes down for the fifth consecutive month

Image Source: TechCabal

Nigeria’s inflation numbers are in, and they are a mixed bag. While inflation has eased for the fifth time in a row, reactions trailing the results question why the numbers don’t seem to match everyday economic reality. In August, Nigeria’s Inflation eased to 20.12%.

The stats say something: Inflation is way down from 32.15% a year ago, meaning prices are still rising, just at a slower rate. Essentially, if your internet bill increased by 20% instead of 30%, you’re still paying more than last year. In 2024, Nigeria’s inflation was one of the highest in Africa. The inflation surge between 2023 and 2024 was mainly due to issues with sourcing foreign exchange, the fuel subsidy removal that increased the cost of logistics, and other agricultural disruptions that increased food prices.Â

The Central Bank will decide next week whether to hold interest rates steady in its fight against inflation. Keeping rates unchanged would ease pressure on businesses and consumers who rely on fintech loans for daily expenses, but it could also risk prolonging inflationary pressures.

Nigeria is pushing ambitious economic reforms to boost investor confidence and hit a $1 trillion economy by 2030. But strong headline numbers don’t always translate into relief for ordinary Nigerians. Prices remain high, and consumer spending is still weak.

HOT TAKE!

Digital assets make up only 0.2% of global commerce, and stablecoins won’t change that overnight. The tech is impressive, but commerce runs on what people can actually use. For informal retailers, stablecoins are hard to grasp, and no one wants to fiddle with blockchain networks at the point of sale. Until stablecoin payments are built into familiar tools like cards, POS machines, and mobile apps that make the blockchain invisible, it’s hard to see them powering street-level commerce anytime soon.

CRYPTO TRACKER

The World Wide Web3

Source:

Coin Name

Current Value

Day

Month

Bitcoin

$115,207

– 0.58%

– 2.03%

Ether

$4,514

– 3.13%

+ 0.86%

Avantis

$1.12

+ 8.00%

+ 278.42%

Solana

$234.32

– 3.55%

+ 21.83%

* Data as of 05.30 AM WAT, September 17, 2025.

Opportunities

Applications are now open for Techstars’ Spring 2026 accelerators. Startups that make it in get a $220,000 investment, mentorship, lifetime access to a global network of investors and alumni, plus over $4 million worth of partner perks. Techstars says graduates raise an average of $1 million+ after the programme. Apply by November 19.

P:S If you’re often missing TC Daily in your inbox, check your Promotions folder and move any edition of TC Daily from “Promotions†to your “Main†or “Primary†folder and TC Daily will always come to you.

Welcome to The Next Wave: Francophone Africa, your weekly look at the tech ecosystem in French-speaking Africa. This newsletter is in French by default, but you can click the button below to read an English version.

Mark your calendars! Moonshot by TechCabal is back in Lagos on October 15–16! Join Africa’s top founders, creatives & tech leaders for 2 days of keynotes, mixers & future-forward ideas. Early bird tickets now 20% off—don’t snooze! Get your tickets.

Living and working in the UK on a Skilled Worker visa is like sleeping with one eye open. In a blink, migrants can lose access to their livelihoods and face a 60-day ultimatum to find another job or be deported back to their home countries.

A Skilled Worker visa can only be sponsored by an authorised company in the UK, few as they are. Things can quickly unravel once an employment is terminated. What follows is a frantic race against time where every rejection, delay or dead-end carries the risk of being forced to leave the country.

I spoke with a UK-based tech worker who experienced this distress firsthand. After leaving college in 2021, he worked as a tech creative in Rwanda but soon landed an opportunity to work at a global tech firm. He worked briefly as an intern and then, after becoming a full-time staff, came to the UK through the Skilled Worker visa program. But just as he was settling into his new life and career, a company-wide layoff left him in the lurch.

This is the story of the tech worker, who asked to remain anonymous for job security reasons, as told to TechCabal.

Welcome to the UK

I attended a session early in 2021 where volunteers were invited to get feedback on their portfolios. I signed up immediately. During that session, I met one of the panel reviewers, a recruiter working at a global tech company. She liked my drive. So, we connected on LinkedIn and kept in touch casually.

By the summer of 2021, she reached out again. There was an internship opportunity at the company—ideal for new graduates. I didn’t need convincing. I applied, went through interviews, and got the position. It was a remote role with the tech company, during a time when the world was still recovering from the 2020 global pandemic. I was based in Rwanda at the time and worked with a team spread across Europe.

Get the best African tech newsletters in your inbox

I joined a team focused on onboarding experiences for work account users. At the company, I met experienced creatives like myself, widened my network, and committed to a singular goal: to get a full-time offer. I networked, refined my portfolio, and ensured my performance was strong enough and visible to my employer.

When the internship ended, there was a performance evaluation. Fortunately, the company did a headcount and found out that it needed new employees in one of its creative departments. With help from the recruiter, I went through the internal hiring process and secured a full-time offer. Once I got the offer, the company started discussions to relocate me to the UK.

It partnered with an accounting firm to handle everything about my visa paperwork to a temporary accommodation in the UK. When I arrived, they advised me on neighbourhoods to live in, sorting taxes, healthcare, and more.

The process [to get my visa] took over two months. Despite corporate support, I still had to undergo health screenings, a tuberculosis test, and provide documents such as a police report and affidavits explaining discrepancies in my surname. But it was the waiting part that was the hardest: I went weeks without updates, unsure if I should plan or panic. It took a while.

But by 2022, I finally relocated to the UK on the Skilled Worker visa, sponsored by the tech company I worked for.

Fast forward to 2025, after working across various teams in the company, a sudden company-wide layoff came. My name was on the list of employees to be let go.

Find a new sponsor or go homeÂ

Within hours of being laid off, the UK Home Office emailed. My visa and stay in the UK was tied to my job, and with the layoff, the sponsorship from my employer had been terminated. I now had 60 days to find a new sponsor or leave the UK. This is called the curtailment period.

I panicked when the email came in. I was already grieving the job loss, and now immigration uncertainty loomed.

I began planning for three futures: find a new UK sponsor, relocate to another country, or return to Rwanda. I started browsing flats in Kigali and Lagos while sending out applications to UK companies. I interviewed at seven companies. Six rejected me outright—they didn’t offer to continue my visa sponsorship. Only one was open to discussing it.

Eventually, I applied to a fintech company I admired. I connected with a recruiter and rushed through the interview process. Fortunately, the company agreed to sponsor me. Due to the fact that it was a visa transfer, and not a fresh application, the process was quicker.

That was how I survived the 60-day countdown. But it took a toll on me.

Curtailment comes with a heavy emotional burden

There is no soft landing when a curtailment notice arrives. The message from the UK Home Office is coldly detached; for them, it’s business as usual. But for the migrant on the receiving end, the emotional weight is heavy.Â

Curtailment periods bring a sense of unadulterated dread—of losing a place to live, of disrupting fragile progress, of being told that years of effort might soon amount to nothing.Â

UK Twitter

I need help for a lady. She came as dependent but I don't know what the guy did. He has been deported under Part 9 of the Immigration rules. She has been given 2 months to leave or find alternative.

She has only 6 weeks left. Any help with COS will be appreciated

There is crippling uncertainty, too. Migrants know what comes next, but not how to get through it.

Faced with the curtailment notice, only three paths typically lie ahead for African migrants.

The first option is to find a new sponsor. That means finding a company that is not only hiring, but also licensed and ready to take on the responsibility of sponsoring a Skilled Worker visa. In the UK, only 134,901 companies—about 3% of the nearly 5.5 million registered companies in the country—are authorised to sponsor foreign workers on temporary work, Skilled Worker, or Global Mobility visas.Â

For a migrant looking for sponsorship, this drastically reduces the pool of employers they’re even willing to consider. Even when a migrant is making headway on a job application with one of the few authorised employers, these companies could lose interest the moment visa sponsorship is mentioned, according to another digital nomad who spoke to TechCabal. It simply means more paperwork.

Employers must prove why the role is essential, confirm that it cannot easily be filled by local talent, and then formally request permission to sponsor. Some companies find the process for getting approval for Certificate of Sponsorship (COS) issuance tedious. Not many are willing to take that on.

Beyond the paperwork, the problem could be that the employer has already filled the number of sponsorship slots it is authorised to offer for the year. Or it could be that the employer simply cannot afford to pay the new salary threshold required for visa sponsorship: £41,700 ($49,000) for most Skilled Worker roles (up from £38,700 as of July 22), while health and care jobs remain at £25,600 ($30,000). These thresholds mean that after tax deductions, those are the least amounts skilled workers must take home. It is also possible that the company has simply exhausted its budget for sponsoring new visa applicants.Â

As a result, even the most qualified candidates are often overlooked, not because they lack skill, but because of the cost and complexity of sponsorship.Â

The second option is to switch to a different visa route. But that comes with its own set of challenges. Some migrants who work in tech may qualify for a Global Talent visa if they can prove exceptional ability. Others might consider a Graduate visa or a Spouse visa, if their partner has British citizenship or a stable immigration status in the UK. Each of these options comes with its own requirements, restrictions, and timelines.Â

These paths demand careful preparation, eligibility, and often a bit of luck. In reality, they are out of reach for most people caught in the 60-day countdown, due to the length of the processing times.

The third and most painful option is to leave the country. Not just the UK, but the life that has been built there. Migrants on Skilled Worker visas often invest time and resources to reach that point. They leave families to adjust to new systems and settle into unfamiliar cities. Being forced to walk away from that progress is a loss that goes beyond employment. It means starting again, often in a place they thought they had left behind.

It currently takes five years on a Skilled Worker or Health and Care Worker visa to qualify for Indefinite Leave to Remain (ILR) in the UK. ILR is the legal right to live and work in the UK without needing a visa. It represents security, residency permanence, and a future that does not hinge on employer decisions. But that future is fragile.

For example, a migrant could lose their job in year 4 of their UK stay. If they cannot find a new sponsor, all that progress is erased. They return home with nothing to show for the years they spent building a life abroad.

Worse, that five-year path may grow longer. The UK government is considering a proposal to extend the ILR timeline to ten years. If that happens, the stakes get even higher.

What it means to stay, and what it takes to plan

Skilled Worker visa holders are vulnerable to disruptions. After years of work, system integration, and tax contributions, their future could be undone by a single corporate decision.

The precarity makes it difficult to plan a future. The idea of settling down, building a future, or even staying put starts to feel risky. Many African professionals left developing economies for the UK. But a curtailment notice could throw everything off-balance.

Migrants on Skilled Worker visas, skilled as they come, remain some of the most precariously placed residents in the UK. Their competence on the job typically carries them through the five-year period to ILR. But as an added layer of caution, it pays for migrants to be on their best behaviour, according to one digital nomad who asked to remain anonymous.

Some sponsoring companies are starting to recognise the emotional toll that comes with sudden layoffs. In a few cases, especially in industries hit hard by economic downturns, migrants are being given advance notice when workforce reductions are on the horizon.Â

While that warning does not soften the emotional blow, it gives migrants a sliver of time to plan, offering them a chance to prepare for what comes next.

* The names of the individuals featured in this story and where they work have been kept anonymous to maintain privacy.

Mark your calendars! Moonshot by TechCabal is back in Lagos on October 15–16! Join Africa’s top founders, creatives & tech leaders for 2 days of keynotes, mixers & future-forward ideas. Early bird tickets now 20% off—don’t snooze! moonshot.techcabal.com

If you earned crypto for the first time ever during the mid-2010’s, chances are you made that money creating posts on Steemit.

For many Nigerians and Africans, crypto publishing apps like Steemit and Publish0x provided the gateway to access crypto. Users made money by writing micro-blogs, growing their engagement and following, and earning from being top contributors on the platforms.

Platforms like Steemit and the much-changed Publish0x were social finance (“SocialFi†in Web3 lingo) apps that allowed users to monetise interactive activities. It was like using Facebook or Reddit, but in a way that you were paid for simply being online.

At its peak between 2017 and 2018, Steemit had over 100,000 Nigerian users on its platform; in Africa, the number was slightly more. The SocialFi app claimed micro-bloggers could earn up to $2.11 for a day’s work.

Nigerian users took it seriously. Influencers on the platform and community leaders hosted physical meet-ups in cities like Lagos, Ibadan, Kaduna, Uyo, and Port Harcourt to teach others how to use the app. They formed local support groups to help newcomers sign up, learn the basics, and grow their earnings.

Physical hangout of Steemit users in Nigeria; circa 2017/Image Source: posted by now-inactive user, @vwovwe; retrieved by TechCabal on July 25, 2025

All that hype from several years ago has now died down. Users, impatient with Steemit’s reward system, began leaving the platform. In recent times, there’s been little sign of platform upgrades or efforts to fix ongoing issues.

Get the best African tech newsletters in your inbox

Steemit and crypto’s early adoption

Founded in 2016 by Ned Scott and Dan Larimer, Steemit was built as a social media platform on the Steem blockchain, owned by the same company. The Steem blockchain also has its digital token, $STEEM, currently priced at $0.1430. Outside of the Steemit platform, people hardly used $STEEM.

People created posts—educational, inspirational, topical, or anything else—and earned money when others “upvoted†them. The more upvotes (similar to “likes†on Facebook or Instagram) your posts received, the more money you made—usually a few $STEEM tokens. During payout days, creators could then transfer their earnings from their Steemit wallet, a built-in custodial wallet, to other crypto wallets like Trust Wallet.

This was before crypto exchanges such as Quidax, Busha, Luno, and the likes exploded in popularity. So, to get other mainstream crypto coins like Bitcoin or Ether, Steemit bloggers had to explore informal peer-to-peer (P2P) channels like WhatsApp groups, to find whom to exchange their $STEEM tokens with. In the same vein, they could also exchange $STEEM for fiat currencies like US dollars or Naira.

Steemit had a feature called “Steem Powerâ€â€”a locked-up version of the token that gave users more voting power. If you had more of it, your upvotes carried more weight and could help creators earn more. This meant that the people with the most Steem Power had a lot of influence on who got rewarded.

Steemit also rewarded people for curating content. This means if you upvoted good content early enough, you earned a part of the payout too. Users also earned through comments, especially if their replies added value to a post or conversation. The more helpful your activity on the platform, the more likely you were to earn something from it.

An example of how a “creator†and a “curator†earned on a popular Steemit post/Image Source: Steemit

The platform ran a built-in reward cycle that took about seven days. So every post had about a week to gather engagement before it was evaluated for payout. All of this was tracked publicly on the blockchain, so people could always check the numbers for themselves.

Crackdown on engagement farming

However, the kryptonite of most creator-centric platforms is human wisdom—and how far people are willing to go with that wisdom. As you may already suspect, Steemit users saw a way to game the system. They would cluster themselves in small groups, called “podsâ€, on Telegram or WhatsApp, and engage with one another’s posts.

This made it easy to cheat the system. People would just upvote their friends’ posts to help them earn more. Over time, this led to poor-quality content rising to the top. The platform tried to stop it with “downvotes,†a way for users to call out low-value and spam posts. Creators caught doing this forfeited a significant portion of their earnings.

In 2019, Steemit broadened its community rules in a further bid to curtail low-value posts. Afterward, it also started taking action against users who used AI tools to generate content, especially when it was obvious the content lacked originality or context.

To tackle the pod problem, Steemit introduced a reputation system, rating users on a scale of 1 to 100. The more your reputation grew through valuable posts and comments, the more weight your upvotes and downvotes carried. If a user with a high reputation upvoted your content, you earned more money than if someone with a low reputation did. This discouraged people from creating fake accounts or relying on new users to game the system.Â

But these strict measures came with a price. As the rules became more rigid, some users felt discouraged. Many of them began migrating to Publish0x, which launched in 2019, and others moved to Hive, a spin-off platform, in hopes of increasing their earnings.

Publish0x started as a social media and microblogging platform. Today, Publish0x partners with survey providers to allow eligible users, depending on their location and interests, to take part in surveys and earn credits. These credits can then be swapped for real money. Though still active, user activity appears to have dropped over time.Â

Get the best African tech newsletters in your inbox

Powering crypto adoption in emerging marketsÂ

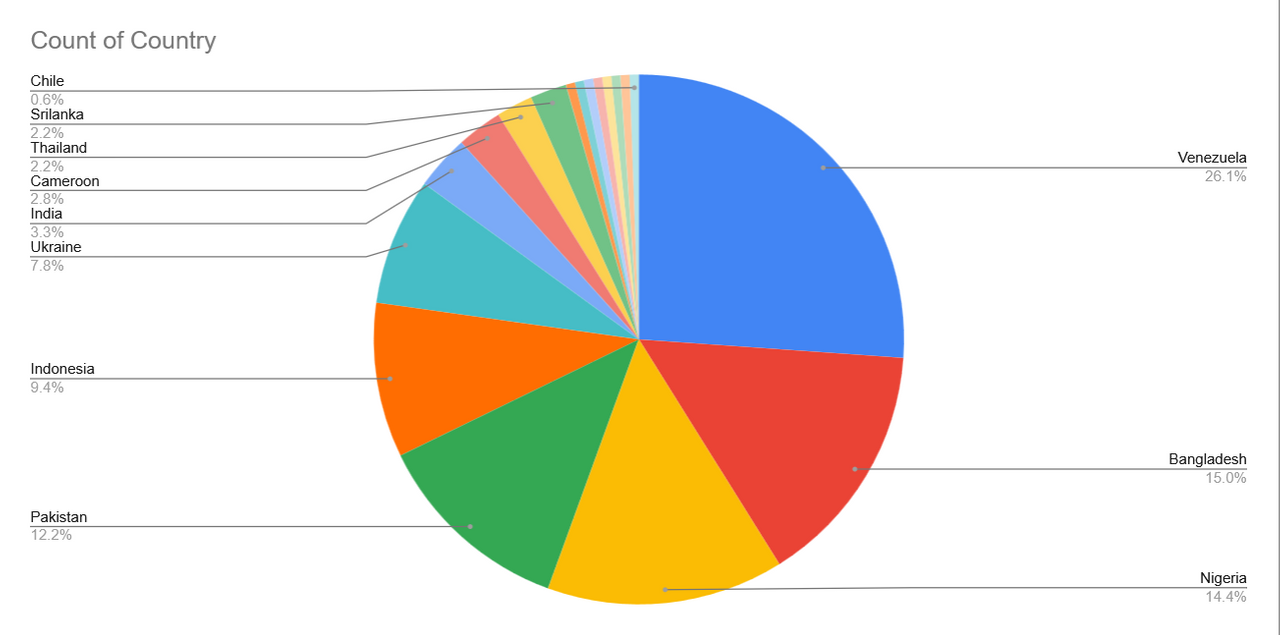

Steemit claims it has now crossed over 1 million users, and that 14.4% of them, as of June 2025, are Nigerians. Around the world, 63.8% of its users are from emerging economies like Indonesia, Bangladesh, Nigeria, Pakistan, and Thailand.

Share of Steemit users as of July 2025/Image Source: The Steem Proof of Development (POD) team, a group of developers building the Steem blockchain ecosystem

The company also says it paid out $59.6 million to creators in June 2025 alone and records over 1 million transactions every 24 hours on its blockchain, pointing to high demand and usage.

According to Semrush, a content marketing platform, Steemit’s website had about 2.2 million visits in June. Online traffic tracker, Similarweb, says 67% of those visitors are men, while 33% are women.

While there may now be over 140,000 Nigerian users on Steemit, a generous estimate will put active daily users—people who use Steemit app daily—in the low thousands. Many Steemit communities have gone quiet, and several of the influencers who helped popularise the platform in Nigeria have since left.

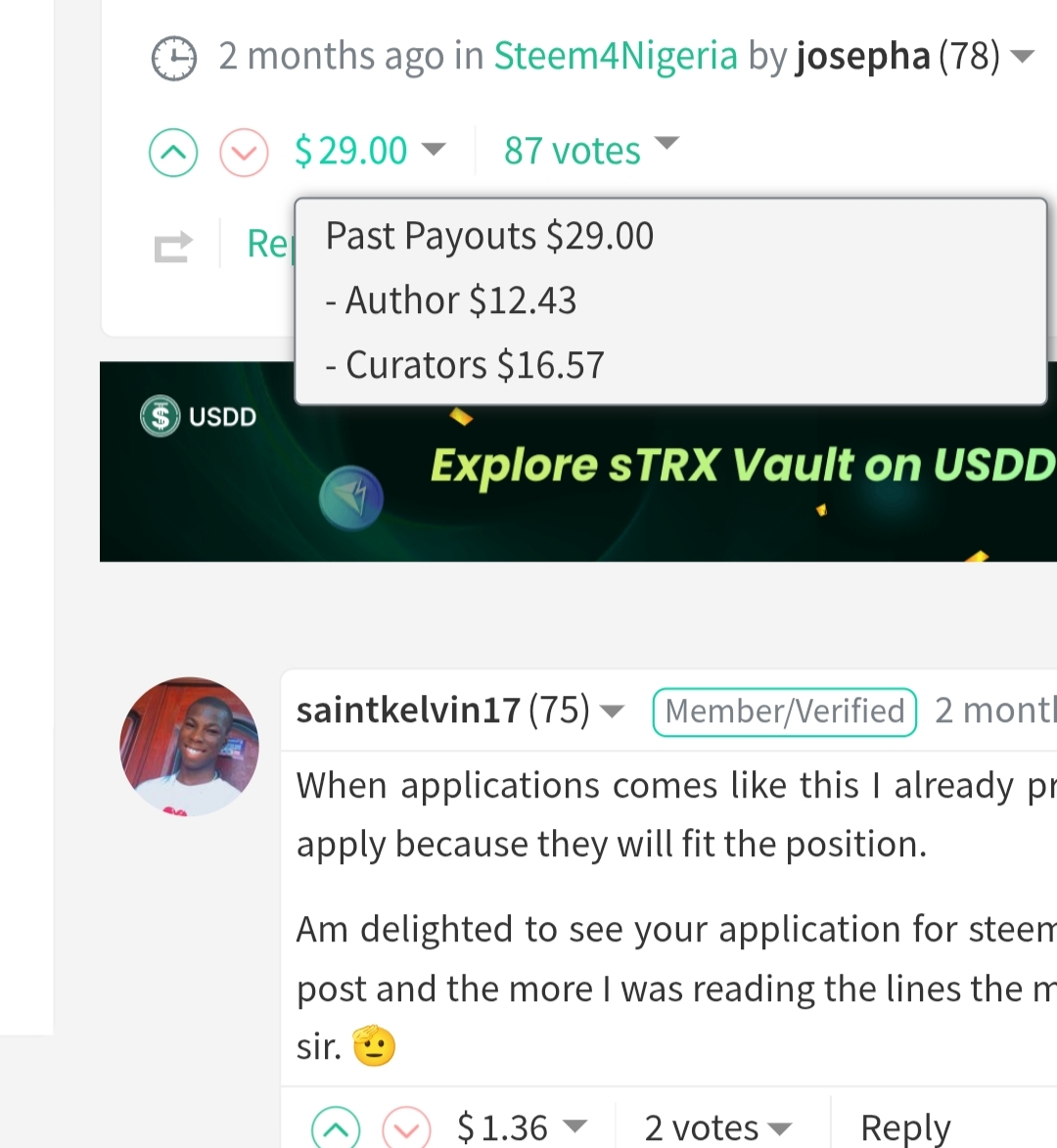

Yet, some Nigerians, still active on Steemit, have managed to cash out over $10,000 from their lifetime activity on the app. For example, Joseph (@josepha), a Nigerian Steemit user who was active 6 hours ago, has earned $7,214.42 overtime; $165.72 in the last month, and $35.26 in the last week. TechCabal was able to verify this on Steemit’s publicly accessible records domain.

Ruth Joe (@ruthjoe), another influential user, has earned $4,076.75, while Ngoenyi (@ngoenyi), another influencer with 2,286 followers, has made over $12,500 in lifetime rewards.

Steemit’s engine is now sputtering, but it hasn’t hit the brakes yet. Devoted fans are still making money from the SocialFi app, often replacing it as their main hustle, or a side income.Â

Mark your calendars! Moonshot by TechCabal is back in Lagos on October 15–16! Join Africa’s top founders, creatives & tech leaders for 2 days of keynotes, mixers & future-forward ideas. Early bird tickets now 20% off—don’t snooze! moonshot.techcabal.com

It’s safe to say Multichoice Nigeria’s legal team isn’t having a good morning as they grapple with a hefty ₦766 million (500,000) fine from the Nigeria Data Protection Commission (NDPC) for violating the Nigeria Data Protection Act (NDP Act).

On a different note, how’s your second half of the year going? If you’re Gen Z, odds are you’re venting on TikTok about low pay, zero flexibility, and office drama. Owl Labs’ 2024 report says 43% of workers are more stressed than last year and 89% see no improvement in their work-related stress. The grind isn’t getting easier. How’s work treating you?

PS: If you’re curious about the tech ecosystem in Francophone Africa, sign up for our latest newsletter, TNW: Francophone Africa. We’ll bring the biggest insider insights and analysis of the region’s technology landscape bi-monthly. Sign up here and be the first to know.

Nigerians can now swipe their naira card globally again

Image Source: Zikoko Memes

After three years, Nigerian banks have finally opened the gates for naira debit cards to roam globally again. That means you can now pay for your Apple Music, Amazon orders, or even that random item on AliExpress with the same card you use for Jumia.

United Bank for Africa (UBA) and Wema Bank are leading the comeback, confirming that their Premium Naira Cards and Naira Mastercards are once again enabled for international transactions—online transactions, POS machines, and ATMs abroad.

Why was there even a restriction? The year was 2022 and the survival of key sectors in the Nigerian economy were under threat. Foreign exchange was scarce, oil revenues were shaky, and Nigeria’s Central Bank’s managed exchange rate wasn’t helping. Eventually, financial institutions pulled the plug on global naira transactions. To keep their playlists going, people turned to virtual dollar cards from fintechs like Chipper Cash, Eversend, Cardtonic, and Payday.

What changed? It appears the confidence in Nigeria’s foreign exchange market is slowly creeping back to Nigeria’s Central Bank. The naira has shown signs of appreciation and diaspora remittances are now over $20 billion.

This is a curveball for virtual card providers. When banks locked international payments, startups like Chipper Cash, Eversend, Cardtonic, and Payday, stepped in with dollar cards. But now? These companies will have to step it up: offer better rates, more flexibility, or risk becoming irrelevant.

This is because not everyone will keep paying extra for what their naira card can now do natively. And in Nigeria’s fast-moving payment space, only the most adaptable will survive the next chapter.

Save more on every NGN transaction with Fincra

Stop overpaying for NGN payments. Fincra’s fees are more affordable than other payment platforms for collections & payouts. The bigger the transaction, the more you save. Create a free account in 3 minutes and start saving today.

Get the best African tech newsletters in your inbox

E-commerce

Takealot wants to hire 18,000 new workers from the ruins of the Post Office

Image Source: Zikoko Memes/TechCabal

18,000 workers who lost their jobs at South Africa’s Post Office, one of the country’s largest public employer, are about to get a new home.

Takealot is in talks to hire up to 18,000 retrenched workers from the South African Post Office, as part of a government-backed plan to repurpose state talent for private sector growth.

The plan, confirmed by the Department of Communications on July 3, is still under discussion. But the direction is clear: Takealot is ramping up its logistics workforce at scale ahead of a delivery war with the likes of new entrants Amazon, Shein, and Temu.

Why does it matter? Takealot is expanding aggressively to maintain its lead in South Africa’s e-commerce market. Amazon’s full local launch in 2024 changed the game. In response, Takealot has grown its revenue by 15%, offloaded non-core assets like Superbalist, and invested in AI tools, dark stores, and delivery operations. Now it’s looking at labour—skilled, available, and already trained in logistics basics.

This potential hiring wave reveals where Takealot’s focus is: building delivery muscle and shifting to an operations-heavy setup. Many of these former Post Office workers already know routing, package handling, and customer service. They also live close to the communities that Takealot wants to reach.

The online retail giant is also exploring township delivery programmes and driver development. It wants to build a national last-mile network that’s faster, more flexible, and harder for Amazon to replicate.

The state sees this as an opportunity to soften the blow of the Post Office collapse. Takealot sees a logistics edge and political capital. South Africa may get both jobs and an improved service delivery. A win for everyone involved.

Drive your business forward with Doroki

Whether you are a retail store, restaurant, pharmacy, supermarket, salon or spa, Doroki helps simplify your operations so you can focus on what matters most: your customers and your growth. Manage your business smarter, start here.

Internet

Egypt just landed two subsea cables with 126 TeraBits per second capacity

Subsea internet cables/Image Source: The Spectator

Telekom Egypt and SubCom just pulled off two key landings of the SEA-ME-WE-6 subsea cable system—one on the Mediterranean and the other on the Red Sea.

SEA-ME-WE-6: Southeast Asia-Middle East-Western Europe 6 (pretty cool, huh?)

Why does this matter? This isn’t just confusing wiring talk, and the SEA-ME-WE-6 isn’t just a shiny new pipeline. It is built to deliver a design capacity of 126 terabits per second, enough to handle millions of high resolution video calls all at the same time. Think faster internet connection, fewer network outages, and better protection against cable disruptions, like the seismic shock that hit West Africa in 2024.

For Egypt, it strengthens its role as a digital transit hub. The country already hosts 10 cable landing stations, supports 15 live subsea cables, and has five more under construction. But the SEA-ME-WE-6 puts Egypt back at the centre of the internet map. With growing demand for high-speed connections driven by cloud services, remote work, and digital trade, Egypt is well-positioned to monetise its geography.More global players will pay to move traffic through its routes, and more investors will look at Egypt’s internet economy seriously. With this, comes more economic power and digital influence for Egypt.

The signal is clear: Egypt isn’t just hosting internet traffic, it is routing the future. Soon, the world won’t just be connecting to Egypt, it will be connecting through it.

Accept in-person payments with Paystack Virtual Terminal!

Anyone can sell in-person. With Paystack Virtual Terminal, you can accept secure payments anywhere using just a QR code. No hardware needed.

Learn more here →

Get the best African tech newsletters in your inbox

Telecoms

NCC gives tower companies until August to improve internet quality or face fines

Image Source: TechCabal

Dear Nigerians, the next time your internet glitches midway through your Netflix binge or a Zoom call, the NCC wants you to know who is responsible.

In a sweeping change, the Nigerian Communications Commission (NCC), the regulator for telecom firms and internet service providers (ISPs), has said it will introduce a portal for tower companies to report downtimes on their network facilities. It has also given them an August deadline to improve their infrastructure or face fines.

Why does this matter? According to the NCC, Nigeria experiences an average of two network outages daily, with a total of 349 major outages recorded across the country between January and June 2025.

The NCC wants every company involved in the network connectivity value chain to be held accountable. When your internet connection frustrates you next time, it’s not enough to blame MTN, Airtel, Glo, or 9mobile. There are more players behind the scenes that make internet connectivity happen. Tower Companies (TowerCos) are one of them; they manage and maintain the cell towers you see in your streets, lease them to telecom companies, and charge for it. When their infrastructure fails, it affects you too.

Zoom out: Since the telecom tariff hike took effect in February, Nigerians have been paying more for internet, voice, and SMS services. Now the NCC is saying: if consumers must pay more, then service providers—especially TowerCos—must deliver more. And fast.

In September 2024, the telecom regulator reviewed its Quality of Service (QoS) benchmarks for mobile operators to improve internet quality and call drop rate. As part of that review, mobile operators now face a fine of ₦5 million ($3,300) if they fail to improve their service, and an additional ₦500,000 ($330) daily for the period the infraction lasts.

TowerCos too, like mobile operators, will get the same accountability treatment. No more excuses about diesel costs or unpaid bills from mobile operators. The Commission has made it clear: downtime has a deadline. And it expires in August.

Women, Apply to TC’s Battlefield Mentorship Programme.

If you’re a Nigerian woman in middle management with an ambitious idea and a passion to build, this is for you.

TechCabal Battlefield and Ventures Platform are offering a mentorship program to help you explore and build your first tech-enabled venture. You’ll get practical insights, honest conversations with founders and investors, and a 1-on-1 session with venture builders and ecosystem enablers.

Apply here→

CRYPTO TRACKER

The World Wide Web3

Source:

Coin Name

Current Value

Day

Month

Bitcoin

$109,191

+ 1.09%

+ 1.43%

Ether

$2,577

+ 2.59%

+ 3.59%

XRP

$2.27

+ 2.02%

+ 4.21%

Solana

$151.93

+ 3.11%

+ 1.37%

* Data as of 06.15 AM WAT, July 7, 2025.

Introducing, The Naira Life Conference by Zikoko

This August, the Naira Life Con will bring together wealth builders, entrepreneurs, financial leaders, and everyday Nigerians to share their experiences with earning, managing, and spending money. Think: bold conversations, immersive workshops, and content tracks that hand you a playbook for building real wealth. Get early bird tickets now at 30% off only for a limited time.

Opportunities

MEST Africa has opened applications for its 2026 AI Startup Programme. The 12-month training and incubation programme will equip West African software developers aged 21–30 with the skills to build scalable AI startups. Selected participants will undergo seven months of hands-on training in Ghana starting January 2026, followed by a four-month incubation for the most promising teams. Applications close August 22, 2025. Apply here.

Applications are still open for the 2025 FATE Institute Fellowship, a two-year, part-time and virtual programme for experienced Nigerian professionals passionate about entrepreneurship and policy reform. The fellowship is open to candidates with at least 10 years of relevant experience and a completed or ongoing Master’s or PhD in fields like Economics, Law, or Political Science. Fellows will work remotely, contribute to research on Nigeria’s entrepreneurship ecosystem, engage with policymakers, and take part in virtual policy discussions, without needing to leave their current roles. Apply by July 25.

We’re launching TechCabal Insights Market Researcher, a tool that helps you find and analyse African tech and business data in seconds. Whether you’re looking for startup funding numbers, market trends, or investor activity, it does the digging for you—fast and accurately. Be the first to try it. Join the waitlist.

P:S If you’re often missing TC Daily in your inbox, check your Promotions folder and move any edition of TC Daily from “Promotions” to your “Main” or “Primary” folder and TC Daily will always come to you.

Cross-border payment is the most bankable buzzword in finance right now and pretty much the side of tech that deals with heft money. Globally, monies that crossed borders in 2024 reached $194.8 trillion.

It’s becoming important in how we work. Freelancers need to get paid from global employers. Digital nomads need their money to cross borders with them. Businesses of all sizes make payments to bring shipments into their home countries. Students studying abroad want to withdraw the money sent to them from home, and diasporan Africans want to send the same back home.

This demand is driving fintechs to build rails that allow money flow smoothly across borders. There is a joke that if you shake a tree, any tree, a remittance fintech will fall. But these startups are overlooking one critical aspect of cross-border payments: intra-African payments.

The problem with intra-African payments

Nnenna Nkata, a Nigerian who went to college in Ghana, and completed her master’s in the UK, has seen both worlds and witnessed the difficulty firsthand. Monirates was her solution to what she describes as “the harder problem.”

“The idea [for Monirates] came when we realised that we could see different fintech startups out there and the various means of sending money from the diaspora to Africa,” said Nkata. “But as a student in Ghana, it was almost difficult to send money from Ghana to Nigeria.” Both countries are about a one-hour flight apart.

It wasn’t just difficult. At one point, she had to move across borders with ₦150,000 ($750)* in her handbag—tuition fees in cash—because digital options were limited, unreliable, or inaccessible. The lack of alternatives wasn’t a bug in the system; it was the system.

“As an undergraduate, I didn’t really realise the effect of this,” she said. “I took it as a norm.”

That changed when she moved to the UK for graduate school. There, sending money back home meant opening five apps, comparing rates, and completing transactions in minutes.

The arguments for why the problem with intra-African payments persists are familiar: there are 42 different currencies in Africa, and regulations, like payments, are fragmented. Where Europe has the Euro and North America spans only three main currencies, Africa is a patchwork quilt.

Get the best African tech newsletters in your inbox

Finding workarounds

Back in 2013, when Nkata schooled at Accra Institute of Technology in Ghana, she and her peers relied on Ecobank automated teller machines (ATMs) to withdraw cash. If you had a Nigerian-issued Ecobank card, you could withdraw cash in cedis from ATMs in Ghana and other countries where Ecobank operated. For a time, it worked.

Then came Central Bank regulations in Nigeria that placed limits on international ATM withdrawals. First $300 per day. Then $100 per month. Eventually, transactions stopped altogether.

“At some point—I think in my final year—I had to move with cash,” Nkata recalled. “There was no way to move the money. You couldn’t even open a bank account as a Nigerian student in Ghana.”

Mobile money, while widely adopted in Ghana, had limits too. It couldn’t handle the large, one-time payments needed for tuition or rent. The fallback was to carry cash across borders, change it at the border unofficially, and hope nothing went wrong.

“It felt like you were smuggling gold when traveling with cash,” she said, laughing. “It came with a lot of risk and stress.”

Her former co-founder—who was a classmate at Accra Institute of Technology—a trader working across Ghana, Guinea, and Nigeria, had to do the same. With both founders living through the complications of everyday payments across borders, Monirates began to take shape.

Building intra-African payments rails from scratch

The product started out as a peer-to-peer tool, something lightweight that allowed users transfer funds directly to one another. But after two months, it pivoted. Escrow wasn’t scalable. What they needed was real infrastructure: rails that could support direct transfers and quick settlements.

“We built our infrastructure from scratch. Every single line of code,” Nkata said. “Eventually, we agreed that there was no point plugging into a system we couldn’t control.”

This decision defined the company’s trajectory. They moved from a consumer payments tool to an infrastructure provider—an “infrastructure-as-a-service” company for tech-enabled businesses moving money within Africa.

But the hurdles kept coming. Intra-African payment is complex not only because of the number of currencies, but because of how disconnected the regulatory frameworks are across regions.

“If you want to support even a quarter of Africa, you’re looking at 20 different currencies. That means 20 different regulations, 20 different central banks, and 20 different infrastructures,” said Nkata.

Expansion wasn’t just a matter of plugging into a new market. It often meant starting over.

“In Ghana, for example, you need to register your business there, and one of your board members has to be Ghanaian,” she said. “It’s like launching a new startup every time.”

The more she looked at the problem, the more she realised most players in the ecosystem were only doing the easy parts.

“What we saw were businesses out there who told customers, ‘We can help you collect payment and pay outright,’ which is fine. But two downsides to that was you could collect, but how do you convert?,” she asked. “If you find a way to convert, settlements become an issue. T+2, T+3. Some can go as far as T+5 days,” she said, referring to how long it can take for a business to receive its money.

“Then the cost is way too high. You are charged 2%, 3% to collect payment from a customer in Uganda, for example. Add that to the cost of FX and the settlement delay, and the business case falls apart,” Nkata added.

That’s why Monirates chose to build a full stack: collection, conversion, and payout. Its rails are designed to move money across corridors with low latency and low cost, making intra-African trade financially viable again.

Get the best African tech newsletters in your inbox

A new quest to power Africa’s SME economy

While Monirates continues to serve individuals, the company is leaning heavily into B2B. Their partners are procurement platforms, logistics firms, and commerce networks—businesses with recurring, high-value transactions.

“Businesses move more money,” Nkata said. “And when they trust you with their payment needs, it forces you to build more reliable systems.”

One such client is Brydge, a pan-African trade company. Monirates powers its cross-border payment flows, allowing them to focus on the rest of the supply chain without worrying about delayed settlements or unofficial agents.

The future of Monirates also includes stablecoins. The company is building capacity to allow customers to send funds in digital currencies such as USDC and USDT. These payments then settle in local African currencies.

“Stablecoin is the quickest and easiest way right now,” she said. “It helps us bridge corridors where we don’t yet have local liquidity.”

Underneath it all, Monirates is also investing in fraud prevention. Their internal system tracks patterns like repeated transfers, irregular intervals, and matching behavior that suggests abuse or circumvention. With over 15 fraud indicators being monitored, the system is constantly evolving.

“Everything is taken care of,” Nkata said. “You can’t scale in this space if you don’t take compliance seriously.”

Doing the hard part

For now, Monirates supports both individuals and businesses—but its energy is behind business infrastructure. Business users currently make up only 10% of their user base but account for significantly higher volume.

“That’s where our head is,” she said. “Building for business clients, because that’s where the impact and growth are.”

The company’s mission is to build Africa’s payment engine; one that supports intra-African trade, scales across regulation, and reflects the economic ties that already exist between countries.

“You can’t build African trade without African payments,” Nkata said. “And you can’t build African payments if you’re not willing to go through the hard part.”

* The exchange rate used in the article is ₦200/$1 in 2015.

Mark your calendars! Moonshot by TechCabal is back in Lagos on October 15–16! Join Africa’s top founders, creatives & tech leaders for 2 days of keynotes, mixers & future-forward ideas. Early bird tickets now 20% off—don’t snooze! moonshot.techcabal.com

Luno, the UK-based crypto company which operates in South Africa, Nigeria—and recently, Uganda—now has a fourth horse to back in its Africa race: Kenya. On June 23, the company announced its re-entry into the East African country after a 2014 exit, expanding its regional presence.

Luno, operating as BitX, first entered Kenya in 2013. It was one of the first startups to offer cryptocurrency trading services in the country, alongside then-competitors—both foreign and local startups—such as Kipochi (which shut down after Safaricom blocked its access to M-Pesa), BitPesa (now AZA Group), and early peer-to-peer (P2P) marketplaces such as LocalBitcoins and Paxful.

The market Luno is returning to ten years later radically differs from the one it left behind. Over the past decade, Kenya has grown into East Africa’s most active cryptocurrency market. The rise of mobile money platforms like M-Pesa, coupled with increasing smartphone penetration and youth-driven digital adoption, has made Kenya a fertile ground for the sector.

Regulatory uncertainty pushed Luno to exit in 2014, but today, that environment is cautiously evolving. A new Virtual Asset Service Providers (VASP) Bill is in the works, promising formal licencing under the oversight of the Central Bank of Kenya (CBK) and the Capital Markets Authority (CMA).

In its comeback, Luno is betting on this regulatory shift—and its decade of experience across Africa. The company has grown to over 15 million global users and now holds a crypto licence in South Africa.

Yet, it won’t be an easy ride for Luno, as Kenya has become a tougher market to compete in with deep-pocketed foreign players such as Binance, Huobi, and OKX, gaining a foothold in the market with their local presence.

TechCabal spoke with Apollo Sande, Luno’s country manager for Kenya and Uganda, who has led the company’s expansion efforts in East Africa for six years.

This interview has been edited for length and clarity.

After more than a decade, why did it make sense to re-enter a market where there is still no licencing framework in place for crypto exchanges?

In 2014, the Central Bank released a circular that stopped banks from working with crypto exchanges and crypto enterprises in Kenya. This made Luno leave the market. Kenya was actually Luno’s second launched market back in 2013, before it began a global expansion.

Then sometime in 2019, Luno decided to take another look at its Africa expansion. I got onboarded and analysed the various markets in East Africa. We prioritised Uganda because it had regulatory certainty. It was easier to have discussions with the Bank of Uganda and other regulators—but Kenya was the prize. Kenya had always been in our sights given the size of its crypto market.

We planned for it and waited while maintaining ongoing interactions with regulators. We were involved in many discussions with authorities in Kenya and Uganda. In December 2024, we decided to re-enter the market. A soft launch has been running since then, and we have now moved to a full launch.

Get the best African tech newsletters in your inbox

What structural risks existed in 2014 when Luno exited Kenya, and do they still exist today?

The biggest risk was the banking ban. It prevented the integration of crypto players with the formal financial system. Startups had to find alternative channels to on- and off-ramps, which led to the rise in P2P payment rails.

P2P rails pose massive risks for customers. They transfer platform risk to the customer. We have seen traders getting arrested or taken to court because they innocently transacted with bad actors. There have been lots of transaction failures, delays, and bad counterparties. The lack of regulation meant players had lax Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols.

This has continued until now. The upcoming regulations will clearly set the standard for crypto platforms. Back in 2012 and 2013, Luno deliberately chose to pay the cost of compliance in advance, knowing it would position us better for a regulated environment. That regulated space is now within reach.

We have formal anti-money laundering regulations and recognition for the industry. Compliant crypto players will secure a position in the market because of the level of trust and stability we bring to the market. We’re banking on this.

Crypto companies still operate in a grey area and no licences have been issued so far. Is this sustainable for long-term operations?

Based on earlier discussions, we observed progress in the regulatory environment. We positioned ourselves while continuing active engagement with regulators. Crypto is not banned in Kenya; only the payment rails were restricted. The methods customers use to deposit and withdraw money in the crypto industry are not yet optimal because we operate outside the existing traditional finance systems. It makes things a little difficult because the playing field is not level.

But see crypto startups as small businesses. It’s not banned, so we just find workarounds. For our Kenyan operations, we’ll make the same play we used in Nigeria when banks stopped working with crypto companies there, too, in 2021. We’ll introduce voucher payments to our Kenyan customers to enable them to easily deposit fiat, buy and sell crypto, and off-ramp to local currency.

In anticipation of upcoming regulations, we expect a lot more certainty. The tax code in Kenya for crypto is undergoing favourable improvement. Regulations are in the final stages at the National Assembly. We think the outcome will be very good for the industry. A lot of the dots have connected, and it is a timely move for us.

Who did Luno Kenya partner with for voucher payment services?

I’d prefer not to provide details about our partner.

The proposal in Kenya is to tax 10% excise duty on crypto transactions. If this goes through, how will this tax demand affect startups’ ability to comply?

Crypto tax was first enacted in 2013 with the previous finance bill. It was set at 3% of the gross value of all crypto exchanges and transfers. That tax was never collected because it was just impractical.

First, there weren’t any banking rails to remit the taxes. Second, that tax was almost 30 times the revenue that crypto exchanges made from commissions. It would have pushed the industry underground.

There has been intense lobbying from the industry. Fortunately, we have a strong team of technocrats within various regulatory bodies who can understand the issue, research it further, and engage with the industry. It became clear that the tax was unsustainable.

There is now an alternative proposal to tax the industry at 10% of the commissions. This is more or less in line with mobile money transfer charges—actually a little lower—plus a corporate income tax. There are still discussions about the applicability of value-added taxes (VAT). However, the tax now makes the industry sustainable. So pending how the regulations work out, at least taxation is not a barrier.

With regards to licencing, the Virtual Asset Service Providers (VASP) Bill has passed a second reading in Parliament. It was really encouraging to hear that level of understanding and foresight from Honourable Moses Kuria and several members of the National Assembly. We are hopeful of a forward-looking regulatory framework.

I always say we should ask what this industry could do for the economy and the country. Then from there, we can take out the risky parts that diminish that potential. Once the VASP Bill passes, the appointed regulators will then create specific licencing frameworks for the various types of players in the crypto industry. That is when we will have clarity about the pathway to licencing.

Who bears this 10% excise duty burden—the users or the crypto companies?

Previously, we would have had to withhold the customer’s trading capital, which could have made us a target. But with the 10% excise duty, which is common in financial services, we bear it. It is worked into our fees. It eats into our margins but offers a better customer experience and makes collection and remittance easier.

How does this affect Luno’s pricing model and trading margins?

It certainly reduces our margin because it is 10% of the fees we charge customers. There’s also a 30% corporate income tax to bear, and potentially a 16% VAT. Yes, it reduces our margins, but in a sustainable way. It’s workable compared to the previous proposal.

Does this result in additional costs for users on Luno Kenya?

That depends on individual business practices. Some businesses may pass the tax on through their fees. Others may absorb it and take the hit to their margins. Fee structures keep changing based on economic realities and business goals.

For Luno Kenya, we will continue to look at our pricing and keep adjusting it to ensure it’s sustainable, affordable, and acceptable for customers. It is an ongoing decision.

How do you view competition in Kenya, especially with P2P enablers like Binance?

Kenya is a rapidly maturing crypto market with many players. There’s a joke that a new crypto exchange or wallet service provider is launching every two or three weeks here. Competition is part of the game.

Over the past ten years, due to the regulatory environment, those who entered the space were mostly tech-savvy, young, high-risk, entrepreneurial individuals willing to endure the rough patches. They found a way with P2P, and that’s fine.

But there is a huge untapped market of people who would not operate within the frameworks of those P2P platforms. They prefer clarity and transparency in the services they use. That is the vast majority of Kenya’s potential crypto market.

Given the business conduct and governance structures of centralised exchanges like Luno, there is still a large gap we can fill. Competition will be tough, but the market is big enough. I don’t think P2P platforms have captured more than 20% of the potential market.

The VASP Bill will require companies to register with the Central Bank of Kenya and the Capital Markets Authority. How far along are you in engaging with these regulators?

We have engaged with all the regulators, with varying degrees of success. We have worked with the CBK, the CMA, and the Financial Reporting Centre. We’ve spoken to all relevant regulators. The same has happened across the industry.

In the past two years, the conversations have become clearer. Regulations are now under the government, and no regulator wants to front-run or prescribe anything until regulations are enacted.

Right now, it is about building relationships. Drafts indicate who will regulate what. But until licencing frameworks are issued, it’s a wait-and-see approach. A new regulator has also been proposed, and their scope will be defined once the bill and frameworks are formalised. Right now, we wait, observe, prepare, and adjust as needed.

How will Luno Kenya monitor transactions on its platform to meet AML expectations and regulatory standards like the travel rule?

Currently, Luno is available in about 40 countries and is licenced in multiple jurisdictions. Some of these countries have very strong AML, KYC, and counter-proliferation processes, which comply with requirements around the travel rule.

We have been managing these risks and monitoring transactions from the start. We’ve been self-regulating where necessary, even when specific crypto regulations did not yet exist. Many of these standards were adopted from the way traditional financial service providers are being regulated in Kenya.

We comply with FATF guidelines and those of other regulators. We have strong anti-financial crime, compliance, and cybersecurity teams and mature systems in place.

We also conduct training for regulators and law enforcement on various aspects of these systems. Transaction monitoring is one of our key strengths.

Get the best African tech newsletters in your inbox

Can you describe some of the tools and methods Luno Kenya uses to flag suspicious transactions?

We have a team dedicated to this. We conduct basic KYC—individual and business due diligence (for institutional users). We also perform ongoing transaction monitoring and use tools like Chainalysis and Elliptic for on-chain monitoring.

During onboarding, we assess the source of funds and customer behaviour. We check for sanctions and politically exposed persons (PEPs). Chainalysis also flags wallets linked to banned activities. We monitor customers’ trading activity, and when there is a significant change from their usual pattern, we flag this and apply enhanced due diligence (EDD).

We also monitor third-party deposits and use geo-location and geofencing tools to identify high-risk areas and trace use of virtual private networks (VPNs). We monitor for on-chain and off-chain risks such as dark markets, gambling, and high-risk jurisdictions. We detect fraud, platform abuse, and payment fraud. We defend accounts by alerting customers to phishing and scams and blacklisting malicious devices.

Screening controls, alerts, and a comprehensive risk management framework help us integrate all compliance and monitoring tools into a cohesive system.

All this integrates into a centralised risk management framework for AML, CTF, and counter-proliferation compliance.

How much capital is Luno Kenya committing to its local operations?

We operate with the backing and support of our centralised teams that manage global operations. In markets with larger operations, there are more localised teams. Much of what we do is customised to each country’s needs. Luno Kenya benefits from strong support from our central team.

Luno has evolved from a crypto and stablecoin off-ramp into a broader crypto exchange. Will Luno Kenya launch with this full range of services or a more limited product?

Since 2013, Luno has had a full order book exchange alongside the instant buy/sell functionality. We’ve always offered wallets for storing, sending, and receiving crypto. The instant buy/sell option lets users trade without comparing quotes, and we also have a live exchange with an order book for more flexible trading.

In most markets, the wallet and instant buy/sell functions are the most used. These services have been part of Luno from the start, along with on- and off-ramping. We are debuting in Kenya with the full range of these services.

The change in recent years has been a ramp-up in the number of listed coins on our platforms.

Does Luno charge for listing coins? And how do you decide what to list?

Like most exchanges, we earn commission on transactions. We facilitate secure and liquid trades and charge a small fee for this.

We have a coin listing committee and team that relies on third-party analysis to assess the credibility of coins. We don’t list everything. We try to be responsible and only list coins we would be comfortable investing in ourselves.

We currently don’t have a process for applications or paid listings. We monitor customer demand, assess what we’re comfortable listing, and then we approach the coin issuers.

What’s Luno Kenya’s stance on enabling the adoption of local stablecoins? Could Luno list local stablecoins like the Kenyan Shilling built on the Celo blockchain (cKES)?

We will continue to monitor these developments. It’s not currently under consideration, but it is a possibility. As we did with USDT and USDC, if there is a strong business case and demand, we’ll look at it on a case-by-case basis.

From a growth perspective, what’s Luno Kenya’s immediate goal and key performance metric?

Given Kenya’s P2P heritage, the market needs safe, simple, secure, and transparent service providers. That is what we’re offering, based on over 13 years of secure operations with no hacks, a reliable and user-friendly interface, and trustworthy service.

That alone fills a gap in the market. It offers a significant improvement in customer safety and experience. From that foundation, we will identify more specific goals.

You’re also the Country Manager for Uganda. What does that mean for the scope of your role with Kenya’s operations kicking off?

We’ve been operational in Uganda since 2019. At first, we had access to banking and mobile money rails, but about two and a half years ago, those were banned. We shifted to a crypto-only platform there. You can get in and out using stablecoins and other crypto.

We believe Kenya’s regulatory progress could be replicated in other countries. When there’s regulatory clarity in Uganda, we may consider reopening a full product suite.

For now, we remain active in Uganda as a crypto-only platform. Operations at this capacity will continue in Uganda while we focus on Kenya.

Mark your calendars! Moonshot by TechCabal is back in Lagos on October 15–16! Join Africa’s top founders, creatives & tech leaders for 2 days of keynotes, mixers & future-forward ideas. Early bird tickets now 20% off—don’t snooze! moonshot.techcabal.com

How much do you know about technology in Francophone Africa? What are the region’s most important startups or crucial policy developments around tech innovation? We’re excited to partner with Lina Kacyem, Investment Manager, Launch Africa Ventures to introduce a web-only newsletter about tech in Francophone Africa.

Lina has almost twenty years of experience in various sectors of the financial industry and is the co-founder of the angel network, Next Millennia Angels. As an investment manager, Lina leads investments in Francophone Africa and will bring decades of first-hand experience, insider insights and analysis of the region’s technology landscape into curating a newsletter that will help you and our wider audience learn about the tech innovation, policy, culture, and economy as it unfolds in Francophone Africa.

Expect a dispatch every two Tuesdays, beginning tomorrow. Sign up here.

DStv’s weekly subscription test: A new chapter in pay-TV?

Image Source: MultiChoice

We’ve heard Multichoice’s 9% year-on-year revenue decline in the recently ended financial year. We’ve heard of their 1.2 million decline in subscribers. Now, we are hearing that the pay-TV giant has quietly started testing weekly subscription plans in Uganda for the last seven weeks.

Users can now pay weekly, instead of paying for a full month. If this trial gains traction, it could spread to the company’s other markets in the coming months.

Why the sudden change? The short answer: people aren’t paying like they used to. Tough macroeconomic situations have made many users cut back on pay-TV, and DSTV wants to adapt. Weekly payments might feel less heavy for users.

What does this mean for viewers? In addition to weekly payments, this move means there’s some flexibility on the horizon, but not full control. MultiChoice still doesn’t believe in customers building their bundle by choosing channels. However, it is exploring an offering where customers could get a base product and then add channels to it. This is in line with its recent plan to unbundle SuperSport from its offerings.

Zoom out: If weekly plans catch on, could they replace monthly plans? Would paying week by week turn out to be cheaper, or become more expensive over time? Could this move bring back old users or lure people away from Netflix and other streaming services?

It’s still in its testing phase, but it is clear that DStv knows it has to evolve or risk being left behind.

Join Fincra for an Exclusive Networking Mixer at iFX Expo, Cyprus.

Fincra is co-hosting “AI-Powered Fintech and Blockchain” at iFX Expo, Cyprus, with Quidax. Join the brightest minds in fintech and blockchain for insightful panels & networking. Limited spots – RSVP here.

Get the best African tech newsletters in your inbox

Mobility

Tesla, the popular EV company, has opened an office in Morocco

Image Source: TechCabal

It looks like Elon Musk wants to lock in again.

After months of playing right-wing politics and being buddies with US President Donald Trump, Musk, the CEO of Tesla, has decided to turn his focus back on his companies.

In his first move after his very public, messy exit from the White House, Musk’s Tesla, the company which makes electric cars, has opened an office in Casablanca, Morocco, with an initial investment of $2.75 million. This is the first time the electric car company will enter an African country—and it’s an interesting play.

Tesla will make and sell its electric cars in Morocco, along with providing energy solutions like charging stations, solar panels, and photovoltaic technologies.

With a presence in Africa, Tesla can control the launch, distribution, and after-sales services of its cars in the market. This is a value chain it previously controlled remotely from the US. People didn’t just steer clear of buying a Tesla because of the lack of infrastructure (South Africans buy electric cars), but the lack of boots on the ground made them second-guess Tesla. This will change things.

But why Morocco? Tesla likely chose Morocco for its strategic location; the region offers a window into the rest of Africa—with cheaper duty-free exports—and also gives the mobility company the opportunity to export to Europe, Gulf countries, or the rest of the Middle East.

Again, with Trump’s “big, beautiful bill” threatening to cut EV subsidies—which have made Tesla cars affordable for Americans over the years—the car company could be looking elsewhere for growth opportunities.

Tesla is entering a $2.56 billion shared mobility market where longtime competitor, China’s BYD, already exists. In Morocco, Renault, Dacia, and Hyundai sell the most cars due to their low-cost maintenance, yet EV demand—especially for e-bikes—is growing.

Whether Tesla will start making e-bikes is something we cannot answer yet, but our guess is it will try to create demand for its cars. If you’re a Moroccan reading this newsletter, this news will make you happy. This author’s dream car is a Tesla.

Order physical Paga cards, spend with confidence.

Tired of declined payments? Avoid the side-eyes at the cash till with Paga’s physical prepaid card. Designed to give you control, security, and ease. Fund and spend with confidence.

Get yours today!.

Startups

Moove eyes $1 billion valuation with planned $300 million raise

Image Source: Tenor

From Lagos to Miami, Moove is on the move to become a unicorn.

The Uber-backed Nigerian startup wants $300 million, a cash injection that could drive its valuation over the $1 billion mark, earning it a unicorn badge.

“What’s this $300 million for?” See it as fuel for the next lap. Moove is growing (and expanding) at breakneck speed. The company’s revenue has climbed to $360 million from $115 million in just a little over a year. In January, it acquired Kovi, a Brazilian urban mobility provider that finances ride-hailing drivers, marking its footprint in Latin America.

The acquisition came after Moove’s partnership with Waymo, a self-driving vehicle division, to manage fleets of autonomous vehicles in US states, including Phoenix, Arizona, and Miami, Florida.

If you don’t know Moove: This startup buys cars with bank loans and offers them to Uber drivers through a drive-to-own model—meaning the drivers can pay for the cars with part of their earnings until they eventually own them.

The new capital will power its expansion ambitions and strengthen its US operations, pushing it further into the world of self-driving cars. This isn’t just another startup trying to bulk up on funding. Moove is plotting a full-blown global takeover, from Lagos to London, and to Waymo robo-taxis in the US.

Where the road leads for Moove: Although the company’s current agreement with Waymo is limited to fleet management, it plans to purchase AV-enabled cars from manufacturers and lease mini-fleets of robotaxis to individuals or businesses. Moove’s ambition is to become a key player in the autonomous mobility ecosystem.

If Moove lands this $300 million, it will possibly become a key infrastructure layer for autonomous vehicles, signalling that African-born startups can lead in shaping global tech infrastructure, not just participate in it.

Stay up to date with the latest Paystack news!

Subscribe to Paystack for a curated dose of product updates, insights, event invites and more. Subscribe here →

Get the best African tech newsletters in your inbox

Cryptocurrency

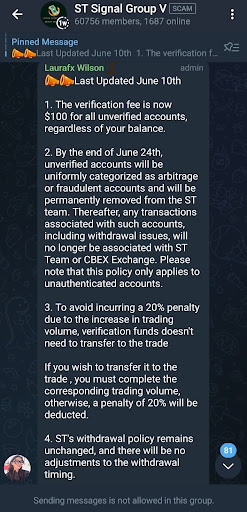

CBEX Ponzi scheme: Nigerians need regulators to save them from themselves

Image Source: Zikoko Memes

It’s sad that despite multiple media reports, warnings, and red flags, many Nigerians are still hooked on CBEX, the Ponzi scheme that took the country by surprise in April.

After freezing withdrawals, CBEX is now asking users to pay a $100 “verification fee” to get their money back.

This makes no sense. A platform that owes you money shouldn’t ask for more. It’s like charging people to unlock the door you already locked from the outside. Classic Ponzi behaviour.

Remember Racksterli? The platform collapsed in 2021, then returned with a dummy site asking users to keep engaging. People kept paying in, but no one got paid out.

Our theory on CBEX is simple: the money is gone. And in its final days, it’s trying to squeeze more out of desperate users to “pay them back.” And sadly, some are still falling for it. According to engagements seen in Telegram groups, users who pay the fee are added to a “private” group to talk to CBEX admins about repayments.

The shuffle of Nigerians toward predatory schemes like CBEX—stemming from greed or desperation at this point—is driven by a deep-rooted lack of financial education. CBEX promised steady monthly returns from crypto futures trading. But if you know anything about trading, you know returns are never guaranteed.

Regulators need to step up. The Securities and Exchange Commission (SEC), for example, could work with telecom operators in the country to block access to known Ponzi websites like CBEX. It might not solve everything, but it could slow the damage.

For now, CBEX says it will pay 50% of debts by June 25. Fingers crossed, but the Ponzi platform remains a ticking time bomb.

Introducing, The Naira Life Conference by Zikoko

This August, the Naira Life Con will bring together wealth builders, entrepreneurs, financial leaders, and everyday Nigerians to share their experiences with earning, managing, and spending money. Think: bold conversations, immersive workshops, and content tracks that hand you a playbook for building real wealth. Get early bird tickets now at 30% off only for a limited time.

P:S If you’re often missing TC Daily in your inbox, check your Promotions folder and move any edition of TC Daily from “Promotions” to your “Main” or “Primary” folder and TC Daily will always come to you.

Nelson Ikan, a Nigerian who once trained as a materials engineer and dreamed of joining the oil and gas elite now works in tech. Ikan is a senior project manager focused on digitising healthcare systems in the UK.

Recently, conversations have reignited online over the career pivots Nigerian migrants make in an attempt to attain success in their new countries of residence.

From students juggling multiple jobs to professionals who’ve swapped offices in their home country for factory jobs, the costs are often emotional, physical, and financial.

“I had to survive.”

Nelson Ikan arrived in the UK in November 2021, setting his sights on building his career in a new country.

“I didn’t work immediately when I came in. I was okay for a couple of months, trying to get settled,” he recalled. “But soon, I needed to raise money to stay afloat.”

He began applying for jobs that he qualified and sometimes was overqualified for. Offers came in, including one from an energy company. Ikan turned the offers down.

“I didn’t take those jobs because I didn’t want to get stuck doing something that didn’t align with what I had planned,” he said. “It wasn’t just about getting a job; for me, it was about getting the right kind of job.”

In the early months that followed, Ikan took up other roles he could find in the UK as he tried to adjust in his new environment. Soon after, he was exploring ways to integrate himself in the UK’s tech scene.

Get the best African tech newsletters in your inbox

Back in Nigeria, Ikan had studied materials engineering, interned at energy company, had a brief stint in banking, before spending seven years in construction. This, he shared, gave him his first real experience managing big projects.

In the UK, when it was time to transition into project management, he leaned into his construction experience. “I had plans of making a life for myself here,” he said. “But I knew I needed something to validate my experience.”